The PANEL Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSpecifying the Input DataSpecifying the Regression ModelUnbalanced DataMissing ValuesComputational ResourcesRestricted EstimatesNotationOne-Way Fixed-Effects ModelTwo-Way Fixed-Effects ModelBalanced PanelsUnbalanced PanelsFirst-Differenced Methods for One-Way and Two-Way ModelsBetween EstimatorsPooled EstimatorOne-Way Random-Effects ModelTwo-Way Random-Effects ModelHausman-Taylor EstimationAmemiya-MaCurdy EstimationParks Method (Autoregressive Model)Da Silva Method (Variance-Component Moving Average Model)Dynamic Panel EstimatorsLinear Hypothesis TestingHeteroscedasticity-Corrected Covariance MatricesHeteroscedasticity- and Autocorrelation-Consistent Covariance MatricesR-SquareSpecification TestsPanel Data Poolability TestPanel Data Cross-Sectional Dependence TestPanel Data Unit Root TestsLagrange Multiplier (LM) Tests for Cross-Sectional and Time EffectsTests for Serial Correlation and Cross-Sectional EffectsTroubleshootingCreating ODS GraphicsOUTPUT OUT= Data SetOUTEST= Data SetOUTTRANS= Data SetPrinted OutputODS Table Names

-

Examples

- References

Heteroscedasticity- and Autocorrelation-Consistent Covariance Matrices

The HAC option in the MODEL statement selects the type of heteroscedasticity- and autocorrelation-consistent covariance matrix.

As with the HCCME option, an estimator of the middle expression  in sandwich form is needed. With the HAC option, it is estimated as

in sandwich form is needed. With the HAC option, it is estimated as

![\[ \Lambda _{\mr{HAC}}=a\sum _{i = 1} ^{N} \sum _{t=1}^{T_ i} \hat{\epsilon }_{it} ^{2}\mb{x} _{it} \mb{x} _{it} ^{'} +a\sum _{i = 1} ^{N} \sum _{t=1}^{T_ i} \sum _{s=1}^{t-1} k(\frac{s-t}{b})\hat{\epsilon }_{it}\hat{\epsilon }_{is}\left(\mb{x} _{it} \mb{x} _{is} ^{'}+\mb{x} _{is} \mb{x} _{it} ^{'}\right) \]](images/etsug_panel0666.png)

, where  is the real-valued kernel function[6], b is the bandwidth parameter, and a is the adjustment factor of small sample degrees of freedom (that is,

is the real-valued kernel function[6], b is the bandwidth parameter, and a is the adjustment factor of small sample degrees of freedom (that is,  if the ADJUSTDF option is not specified and otherwise

if the ADJUSTDF option is not specified and otherwise  , where k is the number of parameters including dummy variables). The types of kernel functions are listed in Table 27.2.

, where k is the number of parameters including dummy variables). The types of kernel functions are listed in Table 27.2.

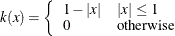

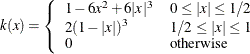

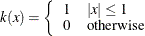

Table 27.2: Kernel Functions

|

Kernel Name |

Equation |

|---|---|

|

Bartlett |

|

|

Parzen |

|

|

Quadratic spectral |

|

|

Truncated |

|

|

Tukey-Hanning |

|

When the BANDWIDTH=ANDREWS option is specified, the bandwidth parameter is estimated as shown in Table 27.3.

Table 27.3: Bandwidth Parameter Estimation

|

Kernel Name |

Bandwidth Parameter |

|---|---|

|

Bartlett |

|

|

Parzen |

|

|

Quadratic spectral |

|

|

Truncated |

|

|

Tukey-Hanning |

|

Let  denote each series in

denote each series in  , and let

, and let  denote the corresponding estimates of the autoregressive and innovation variance parameters of the AR(1) model on ,

denote the corresponding estimates of the autoregressive and innovation variance parameters of the AR(1) model on ,  , where the AR(1) model is parameterized as

, where the AR(1) model is parameterized as  with

with  . The

. The  and

and  are estimated with the following formulas:

are estimated with the following formulas:

![\[ \alpha (1) = \frac{\sum _{a=1}^ k{\frac{4\rho _ a^{2}\sigma _ a^4}{(1-\rho _ a)^6(1+\rho _ a)^2}}}{\sum _{a=1}^ k{\frac{\sigma _ a^4}{(1-\rho _ a)^4}}} \\ \alpha (2) = \frac{\sum _{a=1}^ k{\frac{4\rho _ a^{2}\sigma _ a^4}{(1-\rho _ a)^8}}}{\sum _{a=1}^ k{\frac{\sigma _ a^4}{(1-\rho _ a)^4}}} \]](images/etsug_panel0689.png)

When you specify BANDWIDTH=NEWEYWEST94, according to Newey and West (1994) the bandwidth parameter is estimated as shown in Table 27.4.

Table 27.4: Bandwidth Parameter Estimation

|

Kernel Name |

Bandwidth Parameter |

|---|---|

|

Bartlett |

|

|

Parzen |

|

|

Quadratic spectral |

|

|

Truncated |

|

|

Tukey-Hanning |

|

The  and

and  are estimated with the following formulas:

are estimated with the following formulas:

![\[ s_1 = 2\sum _{j=1}^ n{j\sigma _ j} \\ s_0 = \sigma _0+2\sum _{j=1}^ n{\sigma _ j} \]](images/etsug_panel0697.png)

where n is the lag selection parameter and is determined by kernels, as listed in Table 27.5.

Table 27.5: Lag Selection Parameter Estimation

|

Kernel Name |

Lag Selection Parameter |

|---|---|

|

Bartlett |

|

|

Parzen |

|

|

Quadratic Spectral |

|

|

Truncated |

|

|

Tukey-Hanning |

|

The c in Table 27.5 is specified by the C= option; by default, C=12.

The  is estimated with the equation

is estimated with the equation

![\[ \sigma _ j = T^{-1}\sum _{t=j+1}^{T}{\left(\sum _{a=i}^ k{g_{at}}\sum _{a=i}^ k{g_{at-j}}\right)}, j=0, ..., n \]](images/etsug_panel0703.png)

where  is the same as in the Andrews method and i is 1 if the NOINT option in the MODEL statement is specified, and 2 otherwise.

is the same as in the Andrews method and i is 1 if the NOINT option in the MODEL statement is specified, and 2 otherwise.

When you specify BANDWIDTH=SAMPLESIZE, the bandwidth parameter is estimated with the equation

![\[ b = \left\{ \begin{array}{ l l } \left\lfloor {\gamma T^{r} + c} \right\rfloor & \text {if BANDWIDTH=SAMPLESIZE(INT) option is specified} \\ \gamma T^{r} + c & \text {otherwise} \end{array} \right. \]](images/etsug_panel0705.png)

where T is the sample size,  is the largest integer less than or equal to x, and

is the largest integer less than or equal to x, and  , r, and c are values specified by BANDWIDTH=SAMPLESIZE(GAMMA=, RATE=, CONSTANT=) options, respectively.

, r, and c are values specified by BANDWIDTH=SAMPLESIZE(GAMMA=, RATE=, CONSTANT=) options, respectively.

If the PREWHITENING option is specified in the MODEL statement,  is prewhitened by the VAR(1) model,

is prewhitened by the VAR(1) model,

![\[ g_{it} = A_{i} g_{i,t-1} + w_{it} \]](images/etsug_panel0708.png)

Then  is calculated by

is calculated by

![\[ \Lambda _{\mr{HAC}}=a\sum _{i = 1} ^{N}\left\{ \left(\sum _{t=1}^{T_{i}}{w_{it} w_{it}’}+\sum _{t=1}^{T_{i}}{\sum _{s=1}^{t-1}{k(\frac{s-t}{b})\left(w_{it} w_{is}’ + w_{is} w_{it}’\right)}}\right)(I-A_{i})^{-1}((I-A_{i})^{-1})’\right\} \]](images/etsug_panel0710.png)