The PANEL Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSpecifying the Input DataSpecifying the Regression ModelUnbalanced DataMissing ValuesComputational ResourcesRestricted EstimatesNotationOne-Way Fixed-Effects ModelTwo-Way Fixed-Effects ModelBalanced PanelsUnbalanced PanelsFirst-Differenced Methods for One-Way and Two-Way ModelsBetween EstimatorsPooled EstimatorOne-Way Random-Effects ModelTwo-Way Random-Effects ModelHausman-Taylor EstimationAmemiya-MaCurdy EstimationParks Method (Autoregressive Model)Da Silva Method (Variance-Component Moving Average Model)Dynamic Panel EstimatorsLinear Hypothesis TestingHeteroscedasticity-Corrected Covariance MatricesHeteroscedasticity- and Autocorrelation-Consistent Covariance MatricesR-SquareSpecification TestsPanel Data Poolability TestPanel Data Cross-Sectional Dependence TestPanel Data Unit Root TestsLagrange Multiplier (LM) Tests for Cross-Sectional and Time EffectsTests for Serial Correlation and Cross-Sectional EffectsTroubleshootingCreating ODS GraphicsOUTPUT OUT= Data SetOUTEST= Data SetOUTTRANS= Data SetPrinted OutputODS Table Names

-

Examples

- References

Restricted Estimates

A consequence of estimating a linear model with a restriction is that the error degrees of freedom increase by the number of restrictions. PROC PANEL produces the LaGrange multiplier associated with each restriction.

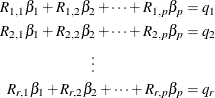

Say that you are interested in linear regression in which there are r restrictions. A linear restriction implies the following set of equations that relate the regression coefficients:

To economize on notation, you can represent the restriction structure in the following matrix notation  . Let

. Let  be the unrestricted estimator of

be the unrestricted estimator of  , and

, and  be the corresponding set of regressors. The restricted

be the corresponding set of regressors. The restricted  estimator is given by:

estimator is given by:

![\[ {\bbeta }^{*} = {\hat\bbeta }- (\mb{X} ^{'}\mb{X} )^{-1}\mb{R} ^{'} \left[\mb{R} (\mb{X} ^{'}\mb{X} )^{-1}\mb{R} ^{'}\right]^{-1}(\mb{R}\hat\bbeta - \mb{q} ) \]](images/etsug_panel0034.png)

The LaGrange multipliers are given as:

![\[ {\blambda }_{*} = \left[\mb{R} (\mb{X} ^{'}\mb{X} )^{-1}\mb{R} ^{'}\right]^{-1}(\mb{R}\hat\bbeta - \mb{q} ) \]](images/etsug_panel0035.png)

The standard errors of the LaGrange multipliers are calculated as:

![\[ \mr{Var}({\blambda }_{*}) = \left[\mb{R} (\mb{X} ^{'}\mb{X} )^{-1}\mb{R} ^{'}\right]^{-1} \mb{R} \mr{Var}({\hat\bbeta })\mb{R} ^{'} \left[\mb{R} (\mb{X} ^{'}\mb{X} )^{-1}\mb{R} ^{'}\right]^{-1} \]](images/etsug_panel0036.png)

A significant LaGrange multiplier implies that you can reject the null hypothesis that the restriction is not binding.

Note that in the special case of the fixed-effects models, the NOINT option and RESTRICT INTERCEPT=0 option give different estimates. This is not an error; it reflects two perspectives on the same issue. In the FIXONE case, the intercept is the last cross section’s fixed effect (or the last time affecting the case of FIXONETIME). Specifying the NOINT option removes the intercept, but allows the last effect in. The NOINT command simply reclassifies the effects. The dummy variables become true cross section effects. If you specify the NOINT option with the FIXTWO option, the restriction is imposed that the last time effect is zero. A RESTRICT INTERCEPT=0 statement suppresses the estimation of the last effect in the FIXONE and FIXONETIME case. A RESTRICT INTERCEPT=0 has similar effects on the FIXTWO estimator. In general, restricting the intercept to zero is not recommended because OLS loses its unbiased nature.