The REG Procedure

- Overview

-

Getting Started

-

Syntax

-

Details

Missing Values Input Data Sets Output Data Sets Interactive Analysis Model-Selection Methods Criteria Used in Model-Selection Methods Limitations in Model-Selection Methods Parameter Estimates and Associated Statistics Predicted and Residual Values Models of Less Than Full Rank Collinearity Diagnostics Model Fit and Diagnostic Statistics Influence Statistics Reweighting Observations in an Analysis Testing for Heteroscedasticity Testing for Lack of Fit Multivariate Tests Autocorrelation in Time Series Data Computations for Ridge Regression and IPC Analysis Construction of Q-Q and P-P Plots Computational Methods Computer Resources in Regression Analysis Displayed Output ODS Table Names ODS Graphics

-

Examples

- References

| Autocorrelation in Time Series Data |

When regression is performed on time series data, the errors might not be independent. Often errors are autocorrelated; that is, each error is correlated with the error immediately before it. Autocorrelation is also a symptom of systematic lack of fit. The DW option provides the Durbin-Watson  statistic to test that the autocorrelation is zero:

statistic to test that the autocorrelation is zero:

|

The value of is close to 2 if the errors are uncorrelated. The distribution of is reported by Durbin and Watson (1951). Tables of the distribution are found in most econometrics textbooks, such as Johnston (1972) and Pindyck and Rubinfeld (1981).

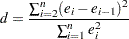

The sample autocorrelation estimate is displayed after the Durbin-Watson statistic. The sample is computed as

|

This autocorrelation of the residuals might not be a very good estimate of the autocorrelation of the true errors, especially if there are few observations and the independent variables have certain patterns. If there are missing observations in the regression, these measures are computed as though the missing observations did not exist.

Positive autocorrelation of the errors generally tends to make the estimate of the error variance too small, so confidence intervals are too narrow and true null hypotheses are rejected with a higher probability than the stated significance level. Negative autocorrelation of the errors generally tends to make the estimate of the error variance too large, so confidence intervals are too wide and the power of significance tests is reduced. With either positive or negative autocorrelation, least squares parameter estimates are usually not as efficient as generalized least squares parameter estimates. For more details, refer to Judge et al. (1985, Chapter 8) and the SAS/ETS User’s Guide.

The following SAS statements request the DWPROB option for the U.S. population data (see Figure 76.50). If you use the DW option instead of the DWPROB option, then  -values are not produced.

-values are not produced.

proc reg data=USPopulation; model Population=Year YearSq / dwProb; run;

| Durbin-Watson D | 1.191 |

|---|---|

| Pr < DW | 0.0050 |

| Pr > DW | 0.9950 |

| Number of Observations | 22 |

| 1st Order Autocorrelation | 0.323 |