The PANEL Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSpecifying the Input DataSpecifying the Regression ModelUnbalanced DataMissing ValuesComputational ResourcesRestricted EstimatesNotationOne-Way Fixed-Effects ModelTwo-Way Fixed-Effects ModelBalanced PanelsUnbalanced PanelsFirst-Differenced Methods for One-Way and Two-Way ModelsBetween EstimatorsPooled EstimatorOne-Way Random-Effects ModelTwo-Way Random-Effects ModelParks Method (Autoregressive Model)Da Silva Method (Variance-Component Moving Average Model)Dynamic Panel EstimatorLinear Hypothesis TestingHeteroscedasticity-Corrected Covariance MatricesHeteroscedasticity- and Autocorrelation-Consistent Covariance MatricesR-SquareSpecification TestsPanel Data Poolability TestPanel Data Cross-Sectional Dependence TestPanel Data Unit Root TestsLagrange Multiplier (LM) Tests for Cross-Sectional and Time EffectsTests for Serial Correlation and Cross-Sectional EffectsTroubleshootingCreating ODS GraphicsOUTPUT OUT= Data SetOUTEST= Data SetOUTTRANS= Data SetPrinted OutputODS Table Names

-

Example

- References

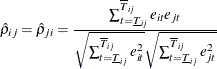

Breusch and Pagan (1980) propose a Lagrange multiplier (LM) statistic to test the null hypothesis of zero cross-sectional error correlations. Let

![]() be the OLS estimate of the error term

be the OLS estimate of the error term ![]() under the null hypothesis. Then the pairwise cross-sectional correlations can be estimated by the sample counterparts

under the null hypothesis. Then the pairwise cross-sectional correlations can be estimated by the sample counterparts ![]() ,

,

where ![]() and

and ![]() are the lower bound and upper bound, respectively, which mark the overlap time periods for the cross sections i and j. If the panel is balanced,

are the lower bound and upper bound, respectively, which mark the overlap time periods for the cross sections i and j. If the panel is balanced, ![]() and

and ![]() . Let

. Let ![]() denote the number of overlapped time periods (

denote the number of overlapped time periods (![]() ). Then the Breusch-Pagan LM test statistic can be constructed as

). Then the Breusch-Pagan LM test statistic can be constructed as

When N is fixed and ![]() ,

, ![]() . So the test is not applicable as

. So the test is not applicable as ![]() .

.

Because ![]() , are asymptotically independent under the null hypothesis of zero cross-sectional correlation,

, are asymptotically independent under the null hypothesis of zero cross-sectional correlation, ![]() . Then the following modified Breusch-Pagan LM statistic can be considered to test for cross-sectional dependence:

. Then the following modified Breusch-Pagan LM statistic can be considered to test for cross-sectional dependence:

Under the null hypothesis, ![]() as

as ![]() , and then

, and then ![]() . But because

. But because ![]() is not correctly centered at zero for finite

is not correctly centered at zero for finite ![]() , the test is likely to exhibit substantial size distortion for large N and small

, the test is likely to exhibit substantial size distortion for large N and small ![]() .

.

Pesaran (2004) proposes a cross-sectional dependence test that is also based on the pairwise correlation coefficients ![]() ,

,

The test statistic has a zero mean for fixed N and ![]() under a wide class of panel data models, including stationary or unit root heterogeneous dynamic models that are subject

to multiple breaks. For each

under a wide class of panel data models, including stationary or unit root heterogeneous dynamic models that are subject

to multiple breaks. For each ![]() , as

, as ![]() ,

, ![]() . Therefore, for N and

. Therefore, for N and ![]() tending to infinity in any order,

tending to infinity in any order, ![]() .

.

To enhance the power against the alternative hypothesis of local dependence, Pesaran (2004) proposes the CDp test. Local dependence is defined with respect to a weight matrix, ![]() . Therefore, the test can be applied only if the cross-sectional units can be given an ordering that remains immutable over

time. Under the alternative hypothesis of a pth-order local dependence, the CD statistic can be generalized to a local CD test, CDp,

. Therefore, the test can be applied only if the cross-sectional units can be given an ordering that remains immutable over

time. Under the alternative hypothesis of a pth-order local dependence, the CD statistic can be generalized to a local CD test, CDp,

where ![]() . When

. When ![]() , CDp reduces to the original CD test. Under the null hypothesis of zero cross-sectional dependence, the CDp statistic is centered at zero for fixed N and

, CDp reduces to the original CD test. Under the null hypothesis of zero cross-sectional dependence, the CDp statistic is centered at zero for fixed N and ![]() , and CD

, and CD![]() as

as ![]() and

and ![]() .

.