The SEVERITY Procedure

- Overview

-

Getting Started

-

Syntax

-

DetailsPredefined DistributionsCensoring and TruncationParameter Estimation MethodParameter InitializationEstimating Regression EffectsLevelization of Classification VariablesSpecification and Parameterization of Model EffectsEmpirical Distribution Function Estimation MethodsStatistics of FitDefining a Severity Distribution Model with the FCMP ProcedurePredefined Utility FunctionsScoring FunctionsCustom Objective FunctionsMultithreaded ComputationInput Data SetsOutput Data SetsDisplayed OutputODS Graphics

-

ExamplesDefining a Model for Gaussian DistributionDefining a Model for the Gaussian Distribution with a Scale ParameterDefining a Model for Mixed-Tail DistributionsEstimating Parameters Using Cramér-von Mises EstimatorFitting a Scaled Tweedie Model with RegressorsFitting Distributions to Interval-Censored DataDefining a Finite Mixture Model That Has a Scale ParameterPredicting Mean and Value-at-Risk by Using Scoring FunctionsScale Regression with Rich Regression Effects

- References

The Tweedie distribution is often used in the insurance industry to explain the influence of regression effects on the distribution of losses. PROC SEVERITY provides a predefined scaled Tweedie distribution (STWEEDIE) that enables you to model the influence of regression effects on the scale parameter. The scale regression model has its own advantages such as the ability to easily account for inflation effects. This example illustrates how that model can be used to evaluate the influence of regression effects on the mean of the Tweedie distribution, which is useful in problems such rate-making and pure premium modeling.

Assume a Tweedie process, whose mean ![]() is affected by k regression effects

is affected by k regression effects ![]() ,

, ![]() as follows:

as follows:

where ![]() represents the base value of the mean (you can think of

represents the base value of the mean (you can think of ![]() as

as ![]() , where

, where ![]() is the intercept). This model for the mean is identical to the popular generalized linear model for the mean with a logarithmic

link function.

is the intercept). This model for the mean is identical to the popular generalized linear model for the mean with a logarithmic

link function.

More interestingly, it parallels the model used by PROC SEVERITY for the scale parameter ![]() ,

,

where ![]() represents the base value of the scale parameter. As described in the section Tweedie Distributions, for the parameter range

represents the base value of the scale parameter. As described in the section Tweedie Distributions, for the parameter range ![]() , the mean of the Tweedie distribution is given by

, the mean of the Tweedie distribution is given by

where ![]() is the Poisson mean parameter of the scaled Tweedie distribution. This relationship enables you to use the scale regression

model to infer the influence of regression effects on the mean of the distribution.

is the Poisson mean parameter of the scaled Tweedie distribution. This relationship enables you to use the scale regression

model to infer the influence of regression effects on the mean of the distribution.

Let the data set Work.Test_Sevtw contain a sample generated from a Tweedie distribution with dispersion parameter ![]() , index parameter

, index parameter ![]() , and the mean parameter that is affected by three regression variables

, and the mean parameter that is affected by three regression variables x1, x2, and x3 as follows:

Thus, the population values of regression parameters are ![]() ,

, ![]() ,

, ![]() , and

, and ![]() . You can find the code used to generate the sample in the PROC SEVERITY sample program

. You can find the code used to generate the sample in the PROC SEVERITY sample program sevex05.sas.

The following PROC SEVERITY step uses the sample in Work.Test_Sevtw data set to estimate the parameters of the scale regression model for the predefined scaled Tweedie distribution (STWEEDIE)

with the dual quasi-Newton (QUANEW) optimization technique:

/*--- Fit the scale parameter version of the Tweedie distribution ---*/ proc severity data=test_sevtw outest=estw covout print=all plots=none; loss y; scalemodel x1-x3; dist stweedie; nloptions tech=quanew; run;

The dual quasi-Newton technique is used because it requires only the first-order derivatives of the objective function, and it is harder to compute reasonably accurate estimates of the second-order derivatives of Tweedie distribution’s PDF with respect to the parameters.

Some of the key results prepared by PROC SEVERITY are shown in Output 23.5.1 and Output 23.5.2. The distribution information and the convergence results are shown in Output 23.5.1.

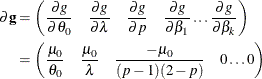

The final parameter estimates of the STWEEDIE regression model are shown in Output 23.5.2. The estimate that is reported for the parameter Theta is the estimate of the base value ![]() . The estimates of regression coefficients

. The estimates of regression coefficients ![]() ,

, ![]() , and

, and ![]() are indicated by the rows of

are indicated by the rows of x1, x2, and x3, respectively.

If your goal is to explain the influence of regression effects on the scale parameter, then the output displayed in Output 23.5.2 is sufficient. But, if you want to compute the influence of regression effects on the mean of the distribution, then you

need to do some postprocessing. Using the relationship between ![]() and

and ![]() ,

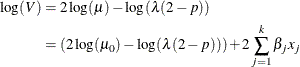

, ![]() can be written in terms of the parameters of the STWEEDIE model as

can be written in terms of the parameters of the STWEEDIE model as

This shows that the parameters ![]() are identical for the mean and the scale model, and the base value

are identical for the mean and the scale model, and the base value ![]() of the mean model is

of the mean model is

The estimate of ![]() and the standard error associated with it can be computed by using the property of the functions of maximum likelihood estimators

(MLE). If

and the standard error associated with it can be computed by using the property of the functions of maximum likelihood estimators

(MLE). If ![]() represents a totally differentiable function of parameters

represents a totally differentiable function of parameters ![]() , then the MLE of g has an asymptotic normal distribution with mean

, then the MLE of g has an asymptotic normal distribution with mean ![]() and covariance

and covariance ![]() , where

, where ![]() is the MLE of

is the MLE of ![]() ,

, ![]() is the estimate of covariance matrix of

is the estimate of covariance matrix of ![]() , and

, and ![]() is the gradient vector of g with respect to

is the gradient vector of g with respect to ![]() evaluated at

evaluated at ![]() . For

. For ![]() , the function is

, the function is ![]() . The gradient vector is

. The gradient vector is

You can write a DATA step that implements these computations by using the parameter and covariance estimates prepared by PROC

SEVERITY step. The DATA step program is available in the sample program sevex05.sas. The estimates of ![]() prepared by that program are shown in Output 23.5.3. These estimates and the estimates of

prepared by that program are shown in Output 23.5.3. These estimates and the estimates of ![]() as shown in Output 23.5.2 are reasonably close (that is, within one or two standard errors) to the parameters of the population from which the sample

in

as shown in Output 23.5.2 are reasonably close (that is, within one or two standard errors) to the parameters of the population from which the sample

in Work.Test_Sevtw data set was drawn.

Another outcome of using the scaled Tweedie distribution to model the influence of regression effects is that the regression

effects also influence the variance V of the Tweedie distribution. The variance is related to the mean as ![]() , where

, where ![]() is the dispersion parameter. Using the relationship between the parameters TWEEDIE and STWEEDIE distributions as described

in the section Tweedie Distributions, the regression model for the dispersion parameter is

is the dispersion parameter. Using the relationship between the parameters TWEEDIE and STWEEDIE distributions as described

in the section Tweedie Distributions, the regression model for the dispersion parameter is

Subsequently, the regression model for the variance is

In summary, PROC SEVERITY enables you to estimate regression effects on various parameters and statistics of the Tweedie model.