The SEVERITY Procedure

- Overview

-

Getting Started

-

Syntax

-

DetailsPredefined DistributionsCensoring and TruncationParameter Estimation MethodParameter InitializationEstimating Regression EffectsLevelization of Classification VariablesSpecification and Parameterization of Model EffectsEmpirical Distribution Function Estimation MethodsStatistics of FitDefining a Severity Distribution Model with the FCMP ProcedurePredefined Utility FunctionsScoring FunctionsCustom Objective FunctionsMultithreaded ComputationInput Data SetsOutput Data SetsDisplayed OutputODS Graphics

-

ExamplesDefining a Model for Gaussian DistributionDefining a Model for the Gaussian Distribution with a Scale ParameterDefining a Model for Mixed-Tail DistributionsEstimating Parameters Using Cramér-von Mises EstimatorFitting a Scaled Tweedie Model with RegressorsFitting Distributions to Interval-Censored DataDefining a Finite Mixture Model That Has a Scale ParameterPredicting Mean and Value-at-Risk by Using Scoring FunctionsScale Regression with Rich Regression Effects

- References

PROC SEVERITY assumes the following model for the response variable Y

where ![]() is a continuous probability distribution with parameters

is a continuous probability distribution with parameters ![]() . The model hypothesizes that the observed response is generated from a stochastic process that is governed by the distribution

. The model hypothesizes that the observed response is generated from a stochastic process that is governed by the distribution

![]() . This model is usually referred to as the error model. Given a representative input sample of response variable values, PROC

SEVERITY estimates the model parameters for any distribution

. This model is usually referred to as the error model. Given a representative input sample of response variable values, PROC

SEVERITY estimates the model parameters for any distribution ![]() and computes the statistics of fit for each model. This enables you to find the distribution that is most likely to generate

the observed sample.

and computes the statistics of fit for each model. This enables you to find the distribution that is most likely to generate

the observed sample.

A set of predefined distributions is provided with the SEVERITY procedure. A summary of the distributions is provided in Table 23.2. For each distribution, the table lists the name of the distribution that should be used in the DIST statement, the parameters of the distribution along with their bounds, and the mathematical expressions for the probability density function (PDF) and cumulative distribution function (CDF) of the distribution.

All the predefined distributions, except LOGN and TWEEDIE, are parameterized such that their first parameter is the scale

parameter. For LOGN, the first parameter ![]() is a log-transformed scale parameter. TWEEDIE does not have a scale parameter. The presence of scale parameter or a log-transformed

scale parameter enables you to use all of the predefined distributions, except TWEEDIE, as a candidate for estimating regression

effects.

is a log-transformed scale parameter. TWEEDIE does not have a scale parameter. The presence of scale parameter or a log-transformed

scale parameter enables you to use all of the predefined distributions, except TWEEDIE, as a candidate for estimating regression

effects.

A distribution model is associated with each predefined distribution. You can also define your own distribution model, which is a set of functions and subroutines that you define by using the FCMP procedure. For more information, see the section Defining a Severity Distribution Model with the FCMP Procedure.

Table 23.2: Predefined SEVERITY Distributions

|

Name |

Distribution |

Parameters |

PDF (f) and CDF (F) |

|

|---|---|---|---|---|

|

BURR |

Burr |

|

|

|

|

|

|

|

||

|

EXP |

Exponential |

|

|

|

|

|

|

|||

|

GAMMA |

Gamma |

|

|

|

|

|

|

|||

|

GPD |

Generalized |

|

|

|

|

Pareto |

|

|

||

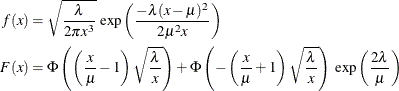

|

IGAUSS |

Inverse Gaussian |

|

|

|

|

(Wald) |

|

|

||

|

|

||||

|

LOGN |

Lognormal |

|

|

|

|

|

|

|

||

|

PARETO |

Pareto |

|

|

|

|

|

|

|||

|

TWEEDIE |

Tweedie |

|

|

|

|

|

|

|

||

|

STWEEDIE |

Scaled Tweedie |

|

|

|

|

|

|

|

||

|

WEIBULL |

Weibull |

|

|

|

|

|

|

|||

|

Notes: |

||||

|

1. |

||||

|

2. |

||||

|

3. Parameters are listed in the order in which they are defined in the distribution model. |

||||

|

4. |

||||

|

5. |

||||

|

6. For more information, see the section Tweedie Distributions. |

||||

Tweedie distributions are a special case of the exponential dispersion family (Jørgensen, 1987) with a property that the variance of the distribution is equal to ![]() , where

, where ![]() is the mean of the distribution,

is the mean of the distribution, ![]() is a dispersion parameter, and p is an index parameter as discovered by Tweedie (1984). The distribution is defined for all values of p except for values of p in the open interval

is a dispersion parameter, and p is an index parameter as discovered by Tweedie (1984). The distribution is defined for all values of p except for values of p in the open interval ![]() . Many important known distributions are a special case of Tweedie distributions including normal (p=0), Poisson (p=1), gamma (p=2), and the inverse Gaussian (p=3). Apart from these special cases, the probability density function (PDF) of the Tweedie distribution does not have an analytic

expression. For

. Many important known distributions are a special case of Tweedie distributions including normal (p=0), Poisson (p=1), gamma (p=2), and the inverse Gaussian (p=3). Apart from these special cases, the probability density function (PDF) of the Tweedie distribution does not have an analytic

expression. For ![]() , it has the form (Dunn and Smyth, 2005),

, it has the form (Dunn and Smyth, 2005),

where ![]() for

for ![]() and

and ![]() for p = 2. The function

for p = 2. The function ![]() does not have an analytical expression. It is typically evaluated using series expansion methods described in Dunn and Smyth

(2005).

does not have an analytical expression. It is typically evaluated using series expansion methods described in Dunn and Smyth

(2005).

For ![]() , the Tweedie distribution is a compound Poisson-gamma mixture distribution, which is the distribution of S defined as

, the Tweedie distribution is a compound Poisson-gamma mixture distribution, which is the distribution of S defined as

where ![]() and

and ![]() are independent and identically distributed gamma random variables with shape parameter

are independent and identically distributed gamma random variables with shape parameter ![]() and scale parameter

and scale parameter ![]() . At X = 0, the density is a probability mass that is governed by the Poisson distribution, and for values of

. At X = 0, the density is a probability mass that is governed by the Poisson distribution, and for values of ![]() , it is a mixture of gamma variates with Poisson mixing probability. The parameters

, it is a mixture of gamma variates with Poisson mixing probability. The parameters ![]() ,

, ![]() , and

, and ![]() are related to the natural parameters

are related to the natural parameters ![]() ,

, ![]() , and p of the Tweedie distribution as

, and p of the Tweedie distribution as

The mean of a Tweedie distribution is positive for ![]() .

.

Two predefined versions of the Tweedie distribution are provided with the SEVERITY procedure. The first version, named TWEEDIE

and defined for ![]() , has the natural parameterization with parameters

, has the natural parameterization with parameters ![]() ,

, ![]() , and p. The second version, named STWEEDIE and defined for

, and p. The second version, named STWEEDIE and defined for ![]() , is the version with a scale parameter. It corresponds to the compound Poisson-gamma distribution with gamma scale parameter

, is the version with a scale parameter. It corresponds to the compound Poisson-gamma distribution with gamma scale parameter

![]() , Poisson mean parameter

, Poisson mean parameter ![]() , and the index parameter p. The index parameter decides the shape parameter

, and the index parameter p. The index parameter decides the shape parameter ![]() of the gamma distribution as

of the gamma distribution as

The parameters ![]() and

and ![]() of the STWEEDIE distribution are related to the parameters

of the STWEEDIE distribution are related to the parameters ![]() and

and ![]() of the TWEEDIE distribution as

of the TWEEDIE distribution as

You can fit either version when there are no regression variables. Each version has its own merits. If you fit the TWEEDIE

version, you have the direct estimate of the overall mean of the distribution. If you are interested in the most practical

range of the index parameter ![]() , then you can fit the STWEEDIE version, which provides you direct estimates of the Poisson and gamma components that comprise

the distribution (an estimate of the gamma shape parameter

, then you can fit the STWEEDIE version, which provides you direct estimates of the Poisson and gamma components that comprise

the distribution (an estimate of the gamma shape parameter ![]() is easily obtained from the estimate of p).

is easily obtained from the estimate of p).

If you want to estimate the effect of exogenous (regression) variables on the distribution, then you must use the STWEEDIE

version, because PROC SEVERITY requires a distribution to have a scale parameter in order to estimate regression effects.

For more information, see the section Estimating Regression Effects. The gamma scale parameter ![]() is the scale parameter of the STWEEDIE distribution. If you are interested in determining the effect of regression variables

on the mean of the distribution, you can do so by first fitting the STWEEDIE distribution to determine the effect of the regression

variables on the scale parameter

is the scale parameter of the STWEEDIE distribution. If you are interested in determining the effect of regression variables

on the mean of the distribution, you can do so by first fitting the STWEEDIE distribution to determine the effect of the regression

variables on the scale parameter ![]() . Then, you can easily estimate how the mean of the distribution

. Then, you can easily estimate how the mean of the distribution ![]() is affected by the regression variables using the relationship

is affected by the regression variables using the relationship ![]() , where

, where ![]() . The estimates of the regression parameters remain the same, whereas the estimate of the intercept parameter is adjusted

by the estimates of the

. The estimates of the regression parameters remain the same, whereas the estimate of the intercept parameter is adjusted

by the estimates of the ![]() and p parameters.

and p parameters.

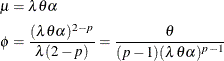

The parameters are initialized by using the method of moments for all the distributions, except for the gamma and the Weibull distributions. For the gamma distribution, approximate maximum likelihood estimates are used. For the Weibull distribution, the method of percentile matching is used.

Given n observations of the severity value ![]() (

(![]() ), the estimate of kth raw moment is denoted by

), the estimate of kth raw moment is denoted by ![]() and computed as

and computed as

The 100pth percentile is denoted by ![]() (

(![]() ). By definition,

). By definition, ![]() satisfies

satisfies

where ![]() . PROC SEVERITY uses the following practical method of computing

. PROC SEVERITY uses the following practical method of computing ![]() . Let

. Let ![]() denote the empirical distribution function (EDF) estimate at a severity value y. Let

denote the empirical distribution function (EDF) estimate at a severity value y. Let ![]() and

and ![]() denote two consecutive values in the ascending sequence of y values such that

denote two consecutive values in the ascending sequence of y values such that ![]() and

and ![]() . Then, the estimate

. Then, the estimate ![]() is computed as

is computed as

Let ![]() denote the smallest double-precision floating-point number such that

denote the smallest double-precision floating-point number such that ![]() . This machine precision constant can be obtained by using the CONSTANT function in Base SAS software.

. This machine precision constant can be obtained by using the CONSTANT function in Base SAS software.

The details of how parameters are initialized for each predefined distribution are as follows:

- BURR

-

The parameters are initialized by using the method of moments. The kth raw moment of the Burr distribution is:

![\[ E[X^ k] = \frac{\theta ^ k \Gamma (1 + k/\gamma ) \Gamma (\alpha - k/\gamma )}{\Gamma (\alpha )}, \quad -\gamma < k < \alpha \gamma \]](images/etsug_severity0112.png)

Three moment equations

![$E[X^ k] = m_ k$](images/etsug_severity0113.png) (

( ) need to be solved for initializing the three parameters of the distribution. In order to get an approximate closed form

solution, the second shape parameter

) need to be solved for initializing the three parameters of the distribution. In order to get an approximate closed form

solution, the second shape parameter  is initialized to a value of 2. If

is initialized to a value of 2. If  , then simplifying and solving the moment equations yields the following feasible set of initial values:

, then simplifying and solving the moment equations yields the following feasible set of initial values:

![\[ \hat{\theta } = \sqrt {\frac{m_2 m_3}{2 m_3 - 3 m_1 m_2}}, \quad \hat{\alpha } = 1 + \frac{m_3}{2 m_3 - 3 m_1 m_2}, \quad \hat{\gamma } = 2 \]](images/etsug_severity0117.png)

If

, then the parameters are initialized as follows:

, then the parameters are initialized as follows:

![\[ \hat{\theta } = \sqrt {m_2}, \quad \hat{\alpha } = 2, \quad \hat{\gamma } = 2 \]](images/etsug_severity0119.png)

- EXP

-

The parameters are initialized by using the method of moments. The kth raw moment of the exponential distribution is:

![\[ E[X^ k] = \theta ^ k \Gamma (k+1), \quad k > -1 \]](images/etsug_severity0120.png)

Solving

![$E[X] = m_1$](images/etsug_severity0121.png) yields the initial value of

yields the initial value of  .

.

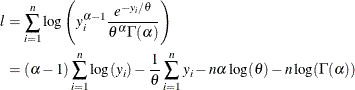

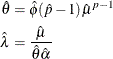

- GAMMA

-

The parameter

is initialized by using its approximate maximum likelihood (ML) estimate. For a set of n independent and identically distributed observations

is initialized by using its approximate maximum likelihood (ML) estimate. For a set of n independent and identically distributed observations  (

( ) drawn from a gamma distribution, the log likelihood l is defined as follows:

) drawn from a gamma distribution, the log likelihood l is defined as follows:

Using a shorter notation of

to denote

to denote  and solving the equation

and solving the equation  yields the following ML estimate of

yields the following ML estimate of  :

:

![\[ \hat{\theta } = \frac{\sum y_ i}{n \alpha } = \frac{m_1}{\alpha } \]](images/etsug_severity0127.png)

Substituting this estimate in the expression of l and simplifying gives

![\[ l = (\alpha - 1) \sum \log (y_ i) - n \alpha - n \alpha \log (m_1) + n \alpha \log (\alpha ) - n \log (\Gamma (\alpha )) \]](images/etsug_severity0128.png)

Let d be defined as follows:

![\[ d = \log (m_1) - \frac{1}{n} \sum \log (y_ i) \]](images/etsug_severity0129.png)

Solving the equation

yields the following expression in terms of the digamma function,

yields the following expression in terms of the digamma function,  :

:

![\[ \log (\alpha ) - \psi (\alpha ) = d \]](images/etsug_severity0132.png)

The digamma function can be approximated as follows:

![\[ \hat{\psi }(\alpha ) \approx \log (\alpha ) - \frac{1}{\alpha } \left(0.5 + \frac{1}{12 \alpha + 2}\right) \]](images/etsug_severity0133.png)

This approximation is within 1.4% of the true value for all the values of

except when is arbitrarily close to the positive root of the digamma function (which is approximately 1.461632). Even for the values

of that are close to the positive root, the absolute error between true and approximate values is still acceptable (

except when is arbitrarily close to the positive root of the digamma function (which is approximately 1.461632). Even for the values

of that are close to the positive root, the absolute error between true and approximate values is still acceptable ( for

for  ). Solving the equation that arises from this approximation yields the following estimate of :

). Solving the equation that arises from this approximation yields the following estimate of :

![\[ \hat{\alpha } = \frac{3 - d + \sqrt {(d-3)^2 + 24 d}}{12 d} \]](images/etsug_severity0136.png)

If this approximate ML estimate is infeasible, then the method of moments is used. The kth raw moment of the gamma distribution is:

![\[ E[X^ k] = \theta ^ k \frac{\Gamma (\alpha + k)}{\Gamma (\alpha )}, \quad k > -\alpha \]](images/etsug_severity0137.png)

Solving

and ![$E[X^2] = m_2$](images/etsug_severity0138.png) yields the following initial value for :

yields the following initial value for :

![\[ \hat{\alpha } = \frac{m_1^2}{m_2 - m_1^2} \]](images/etsug_severity0139.png)

If

(almost zero sample variance), then is initialized as follows:

(almost zero sample variance), then is initialized as follows:

![\[ \hat{\alpha } = 1 \]](images/etsug_severity0141.png)

After computing the estimate of

, the estimate of is computed as follows:

![\[ \hat{\theta } = \frac{m_1}{\hat{\alpha }} \]](images/etsug_severity0142.png)

Both the maximum likelihood method and the method of moments arrive at the same relationship between

and

and  .

.

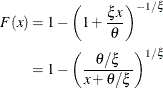

- GPD

-

The parameters are initialized by using the method of moments. Notice that for

, the CDF of the generalized Pareto distribution (GPD) is:

, the CDF of the generalized Pareto distribution (GPD) is:

This is equivalent to a Pareto distribution with scale parameter

and shape parameter

and shape parameter  . Using this relationship, the parameter initialization method used for the PARETO distribution is used to get the following

initial values for the parameters of the GPD distribution:

. Using this relationship, the parameter initialization method used for the PARETO distribution is used to get the following

initial values for the parameters of the GPD distribution:

![\[ \hat{\theta } = \frac{m_1 m_2}{2 (m_2 - m_1^2)}, \quad \hat{\xi } = \frac{m_2 - 2 m_1^2}{2 (m_2 - m_1^2)} \]](images/etsug_severity0148.png)

If

(almost zero sample variance) or  , then the parameters are initialized as follows:

, then the parameters are initialized as follows:

![\[ \hat{\theta } = \frac{m_1}{2}, \quad \hat{\xi } = \frac{1}{2} \]](images/etsug_severity0150.png)

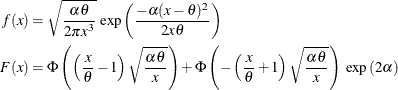

- IGAUSS

-

The parameters are initialized by using the method of moments. The standard parameterization of the inverse Gaussian distribution (also known as the Wald distribution), in terms of the location parameter

and shape parameter

and shape parameter  , is as follows (Klugman, Panjer, and Willmot, 1998, p. 583):

, is as follows (Klugman, Panjer, and Willmot, 1998, p. 583):

For this parameterization, it is known that the mean is

![$E[X] = \mu $](images/etsug_severity0152.png) and the variance is

and the variance is ![$Var[X] = \mu ^3/\lambda $](images/etsug_severity0153.png) , which yields the second raw moment as

, which yields the second raw moment as ![$E[X^2] = \mu ^2 (1 + \mu /\lambda )$](images/etsug_severity0154.png) (computed by using

(computed by using ![$E[X^2] = Var[X] + (E[X])^2$](images/etsug_severity0155.png) ).

).

The predefined IGAUSS distribution in PROC SEVERITY uses the following alternate parameterization to allow the distribution to have a scale parameter,

:

The parameters

(scale) and (shape) of this alternate form are related to the parameters and of the preceding form such that  and

and  . Using this relationship, the first and second raw moments of the IGAUSS distribution are:

. Using this relationship, the first and second raw moments of the IGAUSS distribution are:

![\begin{align*} E[X] & = \theta \\ E[X^2] & = \theta ^2 \left(1 + \frac{1}{\alpha }\right) \end{align*}](images/etsug_severity0159.png)

Solving

and yields the following initial values:

![\[ \hat{\theta } = m_1, \quad \hat{\alpha } = \frac{m_1^2}{m_2 - m_1^2} \]](images/etsug_severity0160.png)

If

(almost zero sample variance), then the parameters are initialized as follows:

![\[ \hat{\theta } = m_1, \quad \hat{\alpha } = 1 \]](images/etsug_severity0161.png)

- LOGN

-

The parameters are initialized by using the method of moments. The kth raw moment of the lognormal distribution is:

![\[ E[X^ k] = \exp \left(k \mu + \frac{k^2 \sigma ^2}{2}\right) \]](images/etsug_severity0162.png)

Solving

and yields the following initial values:

![\[ \hat{\mu } = 2 \log (m1) - \frac{\log (m2)}{2}, \quad \hat{\sigma } = \sqrt {\log (m2) - 2 \log (m1)} \]](images/etsug_severity0163.png)

- PARETO

-

The parameters are initialized by using the method of moments. The kth raw moment of the Pareto distribution is:

![\[ E[X^ k] = \frac{\theta ^ k \Gamma (k + 1) \Gamma (\alpha - k)}{\Gamma (\alpha )}, -1 < k < \alpha \]](images/etsug_severity0164.png)

Solving

and yields the following initial values:

![\[ \hat{\theta } = \frac{m_1 m_2}{m_2 - 2 m_1^2}, \quad \hat{\alpha } = \frac{2(m_2 - m_1^2)}{m_2 - 2 m_1^2} \]](images/etsug_severity0165.png)

If

(almost zero sample variance) or , then the parameters are initialized as follows:

![\[ \hat{\theta } = m_1, \quad \hat{\alpha } = 2 \]](images/etsug_severity0166.png)

- TWEEDIE

-

The parameter p is initialized by assuming that the sample is generated from a gamma distribution with shape parameter

and by computing  . The initial value is obtained from using the method previously described for the GAMMA distribution. The parameter is the mean of the distribution. Hence, it is initialized to the sample mean as

. The initial value is obtained from using the method previously described for the GAMMA distribution. The parameter is the mean of the distribution. Hence, it is initialized to the sample mean as

![\[ \hat{\mu } = m_1 \]](images/etsug_severity0168.png)

Variance of a Tweedie distribution is equal to

. Thus, the sample variance is used to initialize the value of

. Thus, the sample variance is used to initialize the value of  as

as

![\[ \hat{\phi } = \frac{m_2 - m_1^2}{\hat{\mu }^{\hat{p}}} \]](images/etsug_severity0169.png)

- STWEEDIE

-

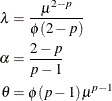

STWEEDIE is a compound Poisson-gamma mixture distribution with mean

, where is the shape parameter of the gamma random variables in the mixture and the parameter p is determined solely by . First, the parameter p is initialized by assuming that the sample is generated from a gamma distribution with shape parameter and by computing . The initial value is obtained from using the method previously described for the GAMMA distribution. As done for initializing the parameters

of the TWEEDIE distribution, the sample mean and variance are used to compute the values

, where is the shape parameter of the gamma random variables in the mixture and the parameter p is determined solely by . First, the parameter p is initialized by assuming that the sample is generated from a gamma distribution with shape parameter and by computing . The initial value is obtained from using the method previously described for the GAMMA distribution. As done for initializing the parameters

of the TWEEDIE distribution, the sample mean and variance are used to compute the values  and

and  as

as

Based on the relationship between the parameters of TWEEDIE and STWEEDIE distributions described in the section Tweedie Distributions, values of

and are initialized as

- WEIBULL

-

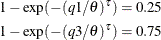

The parameters are initialized by using the percentile matching method. Let

and

and  denote the estimates of the 25th and 75th percentiles, respectively. Using the formula for the CDF of Weibull distribution,

they can be written as

denote the estimates of the 25th and 75th percentiles, respectively. Using the formula for the CDF of Weibull distribution,

they can be written as

Simplifying and solving these two equations yields the following initial values:

![\[ \hat{\theta } = \exp \left(\frac{r \log (q1) - \log (q3)}{r - 1}\right), \quad \hat{\tau } = \frac{\log (\log (4))}{\log (q3) - \log (\hat{\theta })} \]](images/etsug_severity0178.png)

where

. These initial values agree with those suggested in Klugman, Panjer, and Willmot (1998).

. These initial values agree with those suggested in Klugman, Panjer, and Willmot (1998).

A summary of the initial values of all the parameters for all the predefined distributions is given in Table 23.3. The table also provides the names of the parameters to use in the INIT= option in the DIST statement if you want to provide a different initial value.

Table 23.3: Parameter Initialization for Predefined Distributions

|

Distribution |

Parameter |

Name for INIT option |

Default Initial Value |

|---|---|---|---|

|

BURR |

|

theta |

|

|

|

alpha |

|

|

|

|

gamma |

2 |

|

|

EXP |

|

theta |

|

|

GAMMA |

|

theta |

|

|

|

alpha |

|

|

|

GPD |

|

theta |

|

|

|

xi |

|

|

|

IGAUSS |

|

theta |

|

|

|

alpha |

|

|

|

LOGN |

|

mu |

|

|

|

sigma |

|

|

|

PARETO |

|

theta |

|

|

|

alpha |

|

|

|

TWEEDIE |

|

mu |

|

|

|

phi |

|

|

|

p |

p |

|

|

|

where |

|||

|

STWEEDIE |

|

theta |

|

|

|

lambda |

|

|

|

p |

p |

|

|

|

where |

|||

|

WEIBULL |

|

theta |

|

|

|

tau |

|

|

|

Notes: |

|||

|

|

|||

|

|

|||

|

|

|||

|

|

|||