The SEVERITY Procedure

- Overview

-

Getting Started

-

Syntax

-

DetailsPredefined DistributionsCensoring and TruncationParameter Estimation MethodParameter InitializationEstimating Regression EffectsLevelization of Classification VariablesSpecification and Parameterization of Model EffectsEmpirical Distribution Function Estimation MethodsStatistics of FitDefining a Severity Distribution Model with the FCMP ProcedurePredefined Utility FunctionsScoring FunctionsCustom Objective FunctionsMultithreaded ComputationInput Data SetsOutput Data SetsDisplayed OutputODS Graphics

-

ExamplesDefining a Model for Gaussian DistributionDefining a Model for the Gaussian Distribution with a Scale ParameterDefining a Model for Mixed-Tail DistributionsEstimating Parameters Using Cramér-von Mises EstimatorFitting a Scaled Tweedie Model with RegressorsFitting Distributions to Interval-Censored DataDefining a Finite Mixture Model That Has a Scale ParameterPredicting Mean and Value-at-Risk by Using Scoring FunctionsScale Regression with Rich Regression Effects

- References

PROC SEVERITY computes and reports various statistics of fit to indicate how well the estimated model fits the data. The statistics belong to two categories: likelihood-based statistics and EDF-based statistics. Neg2LogLike, AIC, AICC, and BIC are likelihood-based statistics, and KS, AD, and CvM are EDF-based statistics. The following subsections provide definitions of each.

Let ![]() , denote the response variable values. Let L be the likelihood as defined in the section Likelihood Function. Let p denote the number of model parameters that are estimated. Note that

, denote the response variable values. Let L be the likelihood as defined in the section Likelihood Function. Let p denote the number of model parameters that are estimated. Note that ![]() , where

, where ![]() is the number of distribution parameters, k is the number of all regression parameters, and

is the number of distribution parameters, k is the number of all regression parameters, and ![]() is the number of regression parameters that are found to be linearly dependent (redundant) on other regression parameters.

Given this notation, the likelihood-based statistics are defined as follows:

is the number of regression parameters that are found to be linearly dependent (redundant) on other regression parameters.

Given this notation, the likelihood-based statistics are defined as follows:

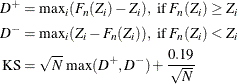

- Neg2LogLike

-

The log likelihood is reported as

![\[ \text {Neg2LogLike} = -2 \log (L) \]](images/etsug_severity0452.png)

The multiplying factor

makes it easy to compare it to the other likelihood-based statistics. A model that has a smaller value of Neg2LogLike is

deemed better.

makes it easy to compare it to the other likelihood-based statistics. A model that has a smaller value of Neg2LogLike is

deemed better.

- AIC

-

Akaike’s information criterion (AIC) is defined as

![\[ \text {AIC} = -2 \log (L) + 2 p \]](images/etsug_severity0454.png)

A model that has a smaller AIC value is deemed better.

- AICC

-

The corrected Akaike’s information criterion (AICC) is defined as

![\[ \text {AICC} = -2 \log (L) + \frac{2 N p}{N - p - 1} \]](images/etsug_severity0455.png)

A model that has a smaller AICC value is deemed better. It corrects the finite-sample bias that AIC has when N is small compared to p. AICC is related to AIC as

![\[ \text {AICC} = \text {AIC} + \frac{2p(p+1)}{N-p-1} \]](images/etsug_severity0456.png)

As N becomes large compared to p, AICC converges to AIC. AICC is usually recommended over AIC as a model selection criterion.

- BIC

-

The Schwarz Bayesian information criterion (BIC) is defined as

![\[ \text {BIC} = -2 \log (L) + p \log (N) \]](images/etsug_severity0457.png)

A model that has a smaller BIC value is deemed better.

This class of statistics is based on the difference between the estimate of the cumulative distribution function (CDF) and the estimate of the empirical distribution function (EDF). A model that has a smaller value of the chosen EDF-based statistic is deemed better.

Let ![]() denote the sample of N values of the response variable. Let

denote the sample of N values of the response variable. Let ![]() denote the number of observations with a value less than or equal to

denote the number of observations with a value less than or equal to ![]() , where I is an indicator function. Let

, where I is an indicator function. Let ![]() denote the EDF estimate that is computed by using the method that you specify in the EMPIRICALCDF=

option. Let

denote the EDF estimate that is computed by using the method that you specify in the EMPIRICALCDF=

option. Let ![]() denote the estimate of the CDF. Let

denote the estimate of the CDF. Let ![]() denote the EDF estimate of

denote the EDF estimate of ![]() values that are computed using the same method that is used to compute the EDF of

values that are computed using the same method that is used to compute the EDF of ![]() values. Using the probability integral transformation, if

values. Using the probability integral transformation, if ![]() is the true distribution of the random variable Y, then the random variable

is the true distribution of the random variable Y, then the random variable ![]() is uniformly distributed between 0 and 1 (D’Agostino and Stephens, 1986, Ch. 4). Thus, comparing

is uniformly distributed between 0 and 1 (D’Agostino and Stephens, 1986, Ch. 4). Thus, comparing ![]() with

with ![]() is equivalent to comparing

is equivalent to comparing ![]() with

with ![]() (uniform distribution).

(uniform distribution).

Note the following two points regarding which CDF estimates are used for computing the test statistics:

-

If you specify regression effects, then the CDF estimates

that are used for computing the EDF test statistics are from a mixture distribution. See the section CDF and PDF Estimates with Regression Effects for more information.

that are used for computing the EDF test statistics are from a mixture distribution. See the section CDF and PDF Estimates with Regression Effects for more information.

-

If the EDF estimates are conditional because of the truncation information, then each unconditional estimate

is converted to a conditional estimate using the method described in the section Truncation and Conditional CDF Estimates.

In the following, it is assumed that ![]() denotes an appropriate estimate of the CDF if you specify any truncation or regression effects. Given this, the EDF-based

statistics of fit are defined as follows:

denotes an appropriate estimate of the CDF if you specify any truncation or regression effects. Given this, the EDF-based

statistics of fit are defined as follows:

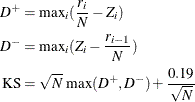

- KS

-

The Kolmogorov-Smirnov (KS) statistic computes the largest vertical distance between the CDF and the EDF. It is formally defined as follows:

![\[ \text {KS} = \sup _ y | F_ n(y) - F(y) | \]](images/etsug_severity0467.png)

If the STANDARD method is used to compute the EDF, then the following formula is used:

Note that

is assumed to be 0.

is assumed to be 0.

If the method used to compute the EDF is any method other than the STANDARD method, then the following formula is used:

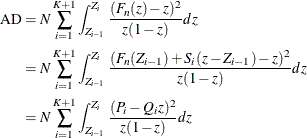

- AD

-

The Anderson-Darling (AD) statistic is a quadratic EDF statistic that is proportional to the expected value of the weighted squared difference between the EDF and CDF. It is formally defined as follows:

![\[ \text {AD} = N \int _{-\infty }^{\infty } \frac{(F_ n(y) - F(y))^2}{F(y) (1-F(y))} dF(y) \]](images/etsug_severity0471.png)

If the STANDARD method is used to compute the EDF, then the following formula is used:

![\[ \text {AD} = -N - \frac{1}{N} \sum _{i=1}^{N} \left[ (2 r_ i - 1) \log (Z_ i) + (2 N + 1 - 2 r_ i) \log (1-Z_ i) \right] \]](images/etsug_severity0472.png)

If the method used to compute the EDF is any method other than the STANDARD method, then the statistic can be computed by using the following two pieces of information:

-

If the EDF estimates are computed using the KAPLANMEIER or MODIFIEDKM methods, then EDF is a step function such that the estimate

is a constant equal to

is a constant equal to  in interval

in interval ![$[Z_{i-1}, Z_ i]$](images/etsug_severity0475.png) . If the EDF estimates are computed using the TURNBULL method, then there are two types of intervals: one in which the EDF

curve is constant and the other in which the EDF curve is theoretically undefined. For computational purposes, it is assumed

that the EDF curve is linear for the latter type of the interval. For each method, the EDF estimate

. If the EDF estimates are computed using the TURNBULL method, then there are two types of intervals: one in which the EDF

curve is constant and the other in which the EDF curve is theoretically undefined. For computational purposes, it is assumed

that the EDF curve is linear for the latter type of the interval. For each method, the EDF estimate  at y can be written as

at y can be written as

![\[ F_ n(z) = F_ n(Z_{i-1}) + S_ i (z - Z_{i-1}), \text { for } z \in [Z_{i-1},Z_ i] \]](images/etsug_severity0476.png)

where

is the slope of the line defined as

is the slope of the line defined as

![\[ S_ i = \frac{F_ n(Z_{i})-F_ n(Z_{i-1})}{Z_{i}-Z_{i-1}} \]](images/etsug_severity0478.png)

For the KAPLANMEIER or MODIFIEDKM method,

in each interval.

in each interval.

-

Using the probability integral transform

, the formula simplifies to

, the formula simplifies to

![\[ \text {AD} = N \int _{-\infty }^{\infty } \frac{(F_ n(z) - z)^2}{z (1-z)} dz \]](images/etsug_severity0481.png)

The computation formula can then be derived from the following approximation:

where

,

,  , and K is the number of points at which the EDF estimate are computed. For the TURNBULL method,

, and K is the number of points at which the EDF estimate are computed. For the TURNBULL method,  for some k.

for some k.

Assuming

,

,  ,

,  , and

, and  yields the following computation formula:

yields the following computation formula:

![\begin{equation*} \begin{split} \text {AD} = & - N (Z_1 + \log (1-Z_1) + \log (Z_ K) + (1-Z_ K)) \\ & + N \sum _{i=2}^{K} \left[ P_ i^2 A_ i - (Q_ i-P_ i)^2 B_ i - Q_ i^2 C_ i \right] \end{split}\end{equation*}](images/etsug_severity0490.png)

where

,

,  , and

, and  .

.

If EDF estimates are computed using the KAPLANMEIER or MODIFIEDKM method, then

and

and  , which simplifies the formula as

, which simplifies the formula as

![\begin{equation*} \begin{split} \text {AD} = & - N (1 + \log (1-Z_1) + \log (Z_ K)) \\ & + N \sum _{i=2}^{K} \left[ F_ n(Z_{i-1})^2 A_ i - (1-F_ n(Z_{i-1}))^2 B_ i \right] \end{split}\end{equation*}](images/etsug_severity0496.png)

-

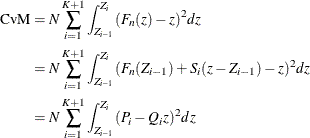

- CvM

-

The Cramér-von Mises (CvM) statistic is a quadratic EDF statistic that is proportional to the expected value of the squared difference between the EDF and CDF. It is formally defined as follows:

![\[ \text {CvM} = N \int _{-\infty }^{\infty } (F_ n(y) - F(y))^2 dF(y) \]](images/etsug_severity0497.png)

If the STANDARD method is used to compute the EDF, then the following formula is used:

![\[ \text {CvM} = \frac{1}{12 N} + \sum _{i=1}^{N} \left( Z_ i - \frac{(2 r_ i - 1)}{2N}\right)^2 \]](images/etsug_severity0498.png)

If the method used to compute the EDF is any method other than the STANDARD method, then the statistic can be computed by using the following two pieces of information:

-

As described previously for the AD statistic, the EDF estimates are assumed to be piecewise linear such that the estimate

at y is

where

is the slope of the line defined as

For the KAPLANMEIER or MODIFIEDKM method,

in each interval.

-

Using the probability integral transform

, the formula simplifies to:

![\[ \text {CvM} = N \int _{-\infty }^{\infty } (F_ n(z) - z)^2 dz \]](images/etsug_severity0499.png)

The computation formula can then be derived from the following approximation:

where

, , and K is the number of points at which the EDF estimate are computed. For the TURNBULL method, for some k.

Assuming

, , and yields the following computation formula:

![\[ \text {CvM} = N \frac{Z_1^3}{3} + N \sum _{i=2}^{K+1} \left[ P_ i^2 A_ i - P_ i Q_ i B_ i - \frac{Q_ i^2}{3} C_ i \right] \]](images/etsug_severity0501.png)

where

,

,  , and

, and  .

.

If EDF estimates are computed using the KAPLANMEIER or MODIFIEDKM method, then

and , which simplifies the formula as

![\[ \text {CvM} = \frac{N}{3} + N \sum _{i=2}^{K+1} \left[ F_ n(Z_{i-1})^2 (Z_ i-Z_{i-1}) - F_ n(Z_{i-1}) (Z_ i^2-Z_{i-1}^2) \right] \]](images/etsug_severity0505.png)

which is similar to the formula proposed by Koziol and Green (1976).

-