The VARMAX Procedure

- Overview

-

Getting Started

-

Syntax

-

Details

Missing Values VARMAX Model Dynamic Simultaneous Equations Modeling Impulse Response Function Forecasting Tentative Order Selection VAR and VARX Modeling Bayesian VAR and VARX Modeling VARMA and VARMAX Modeling Model Diagnostic Checks Cointegration Vector Error Correction Modeling I(2) Model Multivariate GARCH Modeling Output Data Sets OUT= Data Set OUTEST= Data Set OUTHT= Data Set OUTSTAT= Data Set Printed Output ODS Table Names ODS Graphics Computational Issues

-

Examples

- References

| VARMA and VARMAX Modeling |

A VARMA( ) process is written as

) process is written as

|

or

|

where  and

and  .

.

Stationarity and Invertibility

For stationarity and invertibility of the VARMA process, the roots of  and

and  are outside the unit circle.

are outside the unit circle.

Parameter Estimation

Under the assumption of normality of the  with mean vector zero and nonsingular covariance matrix

with mean vector zero and nonsingular covariance matrix  , consider the conditional (approximate) log-likelihood function of a VARMA(

, consider the conditional (approximate) log-likelihood function of a VARMA( ,

, ) model with mean zero.

) model with mean zero.

Define  and

and  with

with  and

and  ; define

; define  and

and  . Then

. Then

|

where  and

and  .

.

Then, the conditional (approximate) log-likelihood function can be written as follows (Reinsel 1997):

|

|

|

|||

|

|

|

where  , and

, and  is such that

is such that  .

.

For the exact log-likelihood function of a VARMA(,) model, the Kalman filtering method is used transforming the VARMA process into the state-space form (Reinsel 1997).

The state-space form of the VARMA(,) model consists of a state equation

|

and an observation equation

|

where for

|

|

and

|

The Kalman filtering approach is used for evaluation of the likelihood function. The updating equation is

|

with

|

and the prediction equation is

|

with  for

for  .

.

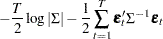

The log-likelihood function can be expressed as

|

where  and

and  are determined recursively from the Kalman filter procedure. To construct the likelihood function from Kalman filtering, you obtain

are determined recursively from the Kalman filter procedure. To construct the likelihood function from Kalman filtering, you obtain  ,

,  , and

, and  .

.

Define the vector

|

where  and

and  .

.

The log-likelihood equations are solved by iterative numerical procedures such as the quasi-Newton optimization. The starting values for the AR and MA parameters are obtained from the least squares estimates.

Asymptotic Distribution of the Parameter Estimates

Under the assumptions of stationarity and invertibility for the VARMA model and the assumption that is a white noise process,  is a consistent estimator for

is a consistent estimator for  and

and  converges in distribution to the multivariate normal

converges in distribution to the multivariate normal  as

as  , where

, where  is the asymptotic information matrix of .

is the asymptotic information matrix of .

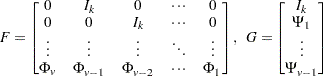

Asymptotic Distributions of Impulse Response Functions

Defining the vector

|

the asymptotic distribution of the impulse response function for a VARMA() model is

|

where  is the covariance matrix of the parameter estimates and

is the covariance matrix of the parameter estimates and

|

where  is a

is a  matrix with the second

matrix with the second  following after block matrices;

following after block matrices;  is a

is a  matrix;

matrix;  is a

is a  matrix,

matrix,

|

where

|

is a

is a  zero matrix, and

zero matrix, and

|

An Example of a VARMA(1,1) Model

Consider a VARMA(1,1) model with mean zero

|

where  is the white noise process with a mean zero vector and the positive-definite covariance matrix .

is the white noise process with a mean zero vector and the positive-definite covariance matrix .

The following IML procedure statements simulate a bivariate vector time series from this model to provide test data for the VARMAX procedure:

proc iml;

sig = {1.0 0.5, 0.5 1.25};

phi = {1.2 -0.5, 0.6 0.3};

theta = {0.5 -0.2, 0.1 0.3};

/* to simulate the vector time series */

call varmasim(y,phi,theta) sigma=sig n=100 seed=34657;

cn = {'y1' 'y2'};

create simul3 from y[colname=cn];

append from y;

run;

The following statements fit a VARMA(1,1) model to the simulated data. You specify the order of the autoregressive model with the P= option and the order of moving-average model with the Q= option. You specify the quasi-Newton optimization in the NLOPTIONS statement as an optimization method.

proc varmax data=simul3; nloptions tech=qn; model y1 y2 / p=1 q=1 noint print=(estimates); run;

Figure 35.46 shows the initial values of parameters. The initial values were estimated using the least squares method.

| Optimization Start | |||

|---|---|---|---|

| Parameter Estimates | |||

| N | Parameter | Estimate | Gradient Objective Function |

| 1 | AR1_1_1 | 1.013118 | -0.987110 |

| 2 | AR1_2_1 | 0.510233 | 0.163904 |

| 3 | AR1_1_2 | -0.399051 | 0.826824 |

| 4 | AR1_2_2 | 0.441344 | -9.605845 |

| 5 | MA1_1_1 | 0.295872 | -1.929771 |

| 6 | MA1_2_1 | -0.002809 | 2.408518 |

| 7 | MA1_1_2 | -0.044216 | -0.632995 |

| 8 | MA1_2_2 | 0.425334 | 0.888222 |

Figure 35.47 shows the default option settings for the quasi-Newton optimization technique.

| Minimum Iterations | 0 |

|---|---|

| Maximum Iterations | 200 |

| Maximum Function Calls | 2000 |

| ABSGCONV Gradient Criterion | 0.00001 |

| GCONV Gradient Criterion | 1E-8 |

| ABSFCONV Function Criterion | 0 |

| FCONV Function Criterion | 2.220446E-16 |

| FCONV2 Function Criterion | 0 |

| FSIZE Parameter | 0 |

| ABSXCONV Parameter Change Criterion | 0 |

| XCONV Parameter Change Criterion | 0 |

| XSIZE Parameter | 0 |

| ABSCONV Function Criterion | -1.34078E154 |

| Line Search Method | 2 |

| Starting Alpha for Line Search | 1 |

| Line Search Precision LSPRECISION | 0.4 |

| DAMPSTEP Parameter for Line Search | . |

| Singularity Tolerance (SINGULAR) | 1E-8 |

Figure 35.48 shows the iteration history of parameter estimates.

| Iteration | Restarts | Function Calls |

Active Constraints |

Objective Function |

Objective Function Change |

Max Abs Gradient Element |

Step Size |

Slope of Search Direction |

||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0 | 38 | 0 | 121.86537 | 0.1020 | 6.3068 | 0.00376 | -54.483 | ||

| 2 | 0 | 57 | 0 | 121.76369 | 0.1017 | 6.9381 | 0.0100 | -33.359 | ||

| 3 | 0 | 76 | 0 | 121.55605 | 0.2076 | 5.1526 | 0.0100 | -31.265 | ||

| 4 | 0 | 95 | 0 | 121.36386 | 0.1922 | 5.7292 | 0.0100 | -37.419 | ||

| 5 | 0 | 114 | 0 | 121.25741 | 0.1064 | 5.5107 | 0.0100 | -17.708 | ||

| 6 | 0 | 133 | 0 | 121.22578 | 0.0316 | 4.9213 | 0.0240 | -2.905 | ||

| 7 | 0 | 152 | 0 | 121.20582 | 0.0200 | 6.0114 | 0.0316 | -1.268 | ||

| 8 | 0 | 171 | 0 | 121.18747 | 0.0183 | 5.5324 | 0.0457 | -0.805 | ||

| 9 | 0 | 207 | 0 | 121.13613 | 0.0513 | 0.5829 | 0.628 | -0.164 | ||

| 10 | 0 | 226 | 0 | 121.13536 | 0.000766 | 0.2054 | 1.000 | -0.0021 | ||

| 11 | 0 | 245 | 0 | 121.13528 | 0.000082 | 0.0534 | 1.000 | -0.0002 | ||

| 12 | 0 | 264 | 0 | 121.13528 | 2.537E-6 | 0.0101 | 1.000 | -637E-8 | ||

| 13 | 0 | 283 | 0 | 121.13528 | 1.475E-7 | 0.000270 | 1.000 | -3E-7 |

Figure 35.49 shows the final parameter estimates.

| Optimization Results | ||

|---|---|---|

| Parameter Estimates | ||

| N | Parameter | Estimate |

| 1 | AR1_1_1 | 1.018085 |

| 2 | AR1_2_1 | 0.391465 |

| 3 | AR1_1_2 | -0.386513 |

| 4 | AR1_2_2 | 0.552904 |

| 5 | MA1_1_1 | 0.322906 |

| 6 | MA1_2_1 | -0.165661 |

| 7 | MA1_1_2 | -0.021533 |

| 8 | MA1_2_2 | 0.586132 |

Figure 35.50 shows the AR coefficient matrix in terms of lag 1, the MA coefficient matrix in terms of lag 1, the parameter estimates, and their significance, which is one indication of how well the model fits the data.

| Type of Model | VARMA(1,1) |

|---|---|

| Estimation Method | Maximum Likelihood Estimation |

| AR | |||

|---|---|---|---|

| Lag | Variable | y1 | y2 |

| 1 | y1 | 1.01809 | -0.38651 |

| y2 | 0.39147 | 0.55290 | |

| MA | |||

|---|---|---|---|

| Lag | Variable | e1 | e2 |

| 1 | y1 | 0.32291 | -0.02153 |

| y2 | -0.16566 | 0.58613 | |

| Schematic Representation | ||

|---|---|---|

| Variable/Lag | AR1 | MA1 |

| y1 | +- | +. |

| y2 | ++ | .+ |

| + is > 2*std error, - is < -2*std error, . is between, * is N/A | ||

| Model Parameter Estimates | ||||||

|---|---|---|---|---|---|---|

| Equation | Parameter | Estimate | Standard Error |

t Value | Pr > |t| | Variable |

| y1 | AR1_1_1 | 1.01809 | 0.10257 | 9.93 | 0.0001 | y1(t-1) |

| AR1_1_2 | -0.38651 | 0.09644 | -4.01 | 0.0001 | y2(t-1) | |

| MA1_1_1 | 0.32291 | 0.14530 | 2.22 | 0.0285 | e1(t-1) | |

| MA1_1_2 | -0.02153 | 0.14200 | -0.15 | 0.8798 | e2(t-1) | |

| y2 | AR1_2_1 | 0.39147 | 0.10062 | 3.89 | 0.0002 | y1(t-1) |

| AR1_2_2 | 0.55290 | 0.08421 | 6.57 | 0.0001 | y2(t-1) | |

| MA1_2_1 | -0.16566 | 0.15700 | -1.06 | 0.2939 | e1(t-1) | |

| MA1_2_2 | 0.58612 | 0.14115 | 4.15 | 0.0001 | e2(t-1) | |

The fitted VARMA(1,1) model with estimated standard errors in parentheses is given as

|

VARMAX Modeling

A VARMAX( ) process is written as

) process is written as

|

or

|

where ,  , and .

, and .

The dimension of the state-space vector of the Kalman filtering method for the parameter estimation of the VARMAX(,, ) model is large, which takes time and memory for computing. For convenience, the parameter estimation of the VARMAX(,,) model uses the two-stage estimation method, which first estimates the deterministic terms and exogenous parameters, and then maximizes the log-likelihood function of a VARMA(,) model.

) model is large, which takes time and memory for computing. For convenience, the parameter estimation of the VARMAX(,,) model uses the two-stage estimation method, which first estimates the deterministic terms and exogenous parameters, and then maximizes the log-likelihood function of a VARMA(,) model.

Some examples of VARMAX modeling are as follows:

model y1 y2 = x1 / q=1; nloptions tech=qn;

model y1 y2 = x1 / p=1 q=1 xlag=1 nocurrentx; nloptions tech=qn;