The SSM Procedure

-

Overview

- Getting Started

-

Syntax

-

DetailsState Space Model and NotationTypes of Sequence DataOverview of Model Specification SyntaxFiltering, Smoothing, Likelihood, and Structural Break DetectionEstimation of User-Specified Linear Combination of State ElementsContrasting PROC SSM with Other SAS Procedures Predefined Trend ModelsPredefined Structural ModelsModels with Dependent LagsCovariance ParameterizationMissing ValuesComputational IssuesDisplayed OutputODS Table NamesODS Graph NamesOUT= Data Set

-

ExamplesBivariate Basic Structural Model Panel Data: Random-Effects and Autoregressive ModelsBackcasting, Forecasting, and InterpolationLongitudinal Data: Smoothing of Repeated MeasuresA User-Defined Trend ModelModel with Multiple ARIMA ComponentsDynamic Factor ModelingDiagnostic Plots and Structural Break AnalysisLongitudinal Data: Variable Bandwidth SmoothingA Transfer Function Model for the Gas Furnace DataPanel Data: Dynamic Panel Model for the Cigar DataMultivariate Modeling: Long-Term Temperature TrendsBivariate Model: Sales of Mink and Muskrat FursFactor Model: Now-Casting the US EconomyLongitudinal Data: Lung Function Analysis

- References

Models with Dependent Lags

Many useful time series models relate the present value of a response variable to its own lagged values and, in the multivariate

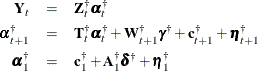

case, the lagged values of other response variables in the model. In the SSM procedure, you can use the DEPLAG

statement to specify the terms in the model that involve lagged response variables. These models apply only to the regular

data type. This section describes the state space form of such models; for more information, see Harvey (1989, sec. 7.1.1). As an illustration, consider the following model, where the q-dimensional coefficient matrices  and

and  are either fully or partially known:

are either fully or partially known:

Except for the presence of the terms that involve lagged response vectors ( and

and  ) in the observation equation, the form of this model is the same as the standard state space form that is described in the

section State Space Model and Notation. It turns out that this model can be expressed in the standard state space form by suitably enlarging the latent vectors

in the state equation and by appropriately reorganizing the system matrices. The enlarged latent vectors and the corresponding

system matrices are distinguished by the presence of dagger (

) in the observation equation, the form of this model is the same as the standard state space form that is described in the

section State Space Model and Notation. It turns out that this model can be expressed in the standard state space form by suitably enlarging the latent vectors

in the state equation and by appropriately reorganizing the system matrices. The enlarged latent vectors and the corresponding

system matrices are distinguished by the presence of dagger ( ) as a superscript in the following reformulated model,

) as a superscript in the following reformulated model,

where the following conditions are true (column vectors are displayed horizontally to save space):

-

The enlarged state vector (

) is formed by vertically stacking the old state vector (

) is formed by vertically stacking the old state vector ( ), the observation disturbance vector (

), the observation disturbance vector ( ), and the present and lagged response vectors (

), and the present and lagged response vectors ( and

and  , respectively). That is,

, respectively). That is, ![$\pmb {\alpha }_{t}^{\dagger } = [\pmb {\alpha }_{t} \; \; \pmb {\epsilon }_{t} \; \; \mb{Y}_{t} \; \; \mb{Y}_{t-1}]$](images/etsug_ssm0469.png) . Because is m-dimensional and , , and are q-dimensional, the dimension of is

. Because is m-dimensional and , , and are q-dimensional, the dimension of is  .

.

-

The new state regression vector (

) is formed by vertically stacking the old state regression vector (

) is formed by vertically stacking the old state regression vector ( ) and the observation equation regression vector (

) and the observation equation regression vector ( ). That is,

). That is, ![$\pmb {\gamma }^{\dagger } = [\pmb {\gamma } \; \; \pmb {\beta }]$](images/etsug_ssm0472.png) .

.

-

The enlarged disturbance vector (

) is formed by vertically stacking the old state disturbance vector (

) is formed by vertically stacking the old state disturbance vector ( ), the observation disturbance vector (), the vector sum

), the observation disturbance vector (), the vector sum  , and filling the rest of the vector with zeros. That is,

, and filling the rest of the vector with zeros. That is, ![$\pmb {\eta }_{t}^{\dagger } = [\pmb {\eta }_{t} \; \; \pmb {\epsilon }_{t} \; \; (\mb{Z}_{t} \pmb {\eta }_{t} + \pmb {\epsilon }_{t}) \; \; \mb{0}]$](images/etsug_ssm0475.png) .

.

-

The deterministic vector

![$\mb{c}_{t+1}^{\dagger } = [ \mb{c}_{t+1} \; \; \mb{0} \; \; \mb{Z}_{t+1}\mb{c}_{t+1} \; \; \mb{0} ]$](images/etsug_ssm0476.png) .

.

-

The last 2q elements of the initial state vector (

), which correspond to

), which correspond to  , and

, and  , are taken to be diffuse (which means that the diffuse vector

, are taken to be diffuse (which means that the diffuse vector  has 2q additional elements compared to

has 2q additional elements compared to  ).

).

The new system matrices can be described in blockwise form in terms of the old system matrices as follows:

-

The

-dimensional

-dimensional ![$\mb{Z}_{t}^{\dagger } = [ \mb{0} \; \mb{0} \; \mb{I} \; \mb{0} ]$](images/etsug_ssm0482.png) , where

, where  is either a

is either a  -dimensional or

-dimensional or  -dimensional matrix of zeros and

-dimensional matrix of zeros and  is a q-dimensional identity matrix.

is a q-dimensional identity matrix.

-

The

matrices

matrices  (transition matrix) and

(transition matrix) and  (covariance of

(covariance of  ) are

) are

![\[ \mb{T}_{t}^{\dagger } = \left[ \begin{matrix} \mb{T}_{t} & \mb{0} & \mb{0} & \mb{0} \\ \mb{0} & \mb{0} & \mb{0} & \mb{0} \\ \mb{Z}_{t+1} \mb{T}_{t} & \mb{0} & \pmb {\Phi }_{1} & \pmb {\Phi }_{2} \\ \mb{0} & \mb{0} & \mb{I} & \mb{0} \\ \end{matrix} \right] \; \; \text {and} \; \; \mb{Q}_{t}^{\dagger } = \left[ \begin{matrix} \mb{Q}_{t} & \mb{0} & \mb{Q}_{t} \mb{Z}_{t+1}^{'} & \mb{0} \\ \mb{0} & \pmb {\Sigma }_{t+1} & \pmb {\Sigma }_{t+1} & \mb{0} \\ \mb{Z}_{t+1} \mb{Q}_{t} & \pmb {\Sigma }_{t+1} & (\mb{Z}_{t+1} \mb{Q}_{t} \mb{Z}_{t+1}^{'} + \pmb {\Sigma }_{t+1}) & \mb{0} \\ \mb{0} & \mb{0} & \mb{0} & \mb{0} \\ \end{matrix} \right] \]](images/etsug_ssm0491.png)

where

denotes the covariance matrix (which is diagonal by design) of the observation error vector . Recall that the system matrices in the transition equation can depend on both t and

denotes the covariance matrix (which is diagonal by design) of the observation error vector . Recall that the system matrices in the transition equation can depend on both t and  even if the subscripts of

even if the subscripts of  and

and  show dependence on t alone.

show dependence on t alone.

-

The

matrix

matrix  is

is

![\[ \mb{W}_{t+1}^{\dagger } = \left[ \begin{matrix} \mb{W}_{t+1} & \mb{0} \\ \mb{0} & \mb{0} \\ \mb{Z}_{t+1} \mb{W}_{t+1} & \mb{X}_{t+1} \\ \mb{0} & \mb{0} \\ \end{matrix} \right] \]](images/etsug_ssm0495.png)

This state space form can be easily extended to account for higher-order lags.

Models that contain dependent lag terms must be used with care. Because the SSM procedure does not impose any special constraints

on the lag coefficients (the elements of coefficient matrices  ), the resulting models can often be explosive. For an example of a model with lagged response variables, see Example 34.13.

), the resulting models can often be explosive. For an example of a model with lagged response variables, see Example 34.13.

PROC SSM and PROC UCM (see Chapter 41: The UCM Procedure) handle models that contain dependent lags in essentially the same way. However, there is one difference: if the model parameter vector contains unknown lag parameters, PROC UCM parameters are estimated by optimizing the nondiffuse part of the likelihood whereas PROC SSM continues to use the full diffuse likelihood for parameter estimation.