The ARIMA Procedure

- Overview

-

Getting Started

The Three Stages of ARIMA ModelingIdentification StageEstimation and Diagnostic Checking StageForecasting StageUsing ARIMA Procedure StatementsGeneral Notation for ARIMA ModelsStationarityDifferencingSubset, Seasonal, and Factored ARMA ModelsInput Variables and Regression with ARMA ErrorsIntervention Models and Interrupted Time SeriesRational Transfer Functions and Distributed Lag ModelsForecasting with Input VariablesData Requirements

The Three Stages of ARIMA ModelingIdentification StageEstimation and Diagnostic Checking StageForecasting StageUsing ARIMA Procedure StatementsGeneral Notation for ARIMA ModelsStationarityDifferencingSubset, Seasonal, and Factored ARMA ModelsInput Variables and Regression with ARMA ErrorsIntervention Models and Interrupted Time SeriesRational Transfer Functions and Distributed Lag ModelsForecasting with Input VariablesData Requirements -

Syntax

-

DetailsThe Inverse Autocorrelation FunctionThe Partial Autocorrelation FunctionThe Cross-Correlation FunctionThe ESACF MethodThe MINIC MethodThe SCAN MethodStationarity TestsPrewhiteningIdentifying Transfer Function ModelsMissing Values and AutocorrelationsEstimation DetailsSpecifying Inputs and Transfer FunctionsInitial ValuesStationarity and InvertibilityNaming of Model ParametersMissing Values and Estimation and ForecastingForecasting DetailsForecasting Log Transformed DataSpecifying Series PeriodicityDetecting OutliersOUT= Data SetOUTCOV= Data SetOUTEST= Data SetOUTMODEL= SAS Data SetOUTSTAT= Data SetPrinted OutputODS Table NamesStatistical Graphics

-

Examples

- References

Initial Values

The syntax for giving initial values to transfer function parameters in the INITVAL= option parallels the syntax of the INPUT= option. For each transfer function in the INPUT= option, the INITVAL= option should give an initialization specification followed by the input series name. The initialization specification for each transfer function has the form

![\[ C ~ \$ ~ (V_{1,1},V_{1,2}, {\ldots }) (V_{2,1}, {\ldots }) {\ldots } / (V_{\mi{i},1}, {\ldots }) {\ldots } \]](images/etsug_arima0260.png)

where C is the lag 0 term in the first numerator factor of the transfer function (or the overall scale factor if the ALTPARM option

is specified) and  is the coefficient of the

is the coefficient of the  element in the transfer function.

element in the transfer function.

To illustrate, suppose you want to fit the model

![\[ Y_{t}={\mu }+\frac{({\omega }_{0}- {\omega }_{1}{B}-{\omega }_{2}{B}^{2})}{(1-{\delta }_{1}{B}-{\delta }_{2}{B}^{2}-{\delta }_{3}{B}^{3})}X_{t-3} +\frac{1}{(1-{\phi }_{1}{B}-{\phi }_{2}{B}^{3})}a_{t} \]](images/etsug_arima0262.png)

and start the estimation process with the initial values  =10,

=10,  =1,

=1,  =0.5,

=0.5,  =0.03,

=0.03,  =0.8,

=0.8,  =–0.1,

=–0.1,  =0.002,

=0.002,  =0.1,

=0.1,  =0.01. (These are arbitrary values for illustration only.) You would use the following statements:

=0.01. (These are arbitrary values for illustration only.) You would use the following statements:

identify var=y crosscorr=x;

estimate p=(1,3) input=(3$(1,2)/(1,2,3)x)

mu=10 ar=.1 .01

initval=(1$(.5,.03)/(.8,-.1,.002)x);

Note that the lags specified for a particular factor are sorted, so initial values should be given in sorted order. For example, if the P= option had been entered as P=(3,1) instead of P=(1,3), the model would be the same and so would the AR= option. Sorting is done within all factors, including transfer function factors, so initial values should always be given in order of increasing lags.

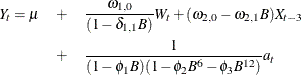

Here is another illustration, showing initialization for a factored model with multiple inputs. The model is

and the initial values are =10,  =5,

=5,  =0.8,

=0.8,  =1,

=1,  =0.5,

=0.5,  =0.1,

=0.1,  =0.05, and

=0.05, and  =0.01. You would use the following statements:

=0.01. You would use the following statements:

identify var=y crosscorr=(w x);

estimate p=(1)(6,12) input=(/(1)w, 3$(1)x)

mu=10 ar=.1 .05 .01

initval=(5$/(.8)w 1$(.5)x);