The HPQUANTSELECT Procedure

More Statistics for Parameter Estimates

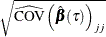

Let  denote the covariance function matrix of a random vector. Then, the sparsity-function estimates of

denote the covariance function matrix of a random vector. Then, the sparsity-function estimates of  is

is

![\[ \widehat{\mbox{COV}}\left(\hat{\bbeta }(\tau )\right)=\left\{ \begin{array}{l l} \omega ^2(\tau , F)\bOmega ^{-1}/n & \mbox{for a linear model with iid errors}\\ \tau (1-\tau )\mb{H}_ n^{-}\bOmega \mb{H}_ n^{-})/n & \mbox{for a linear-in-parameter model with non-iid settings} \end{array} \right. \]](images/stathpug_hpqtr0082.png)

where  is the vector of the parameter estimates.

is the vector of the parameter estimates.

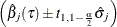

If you specify the CLB option in the MODEL

statement, PROC HPQUANTSELECT outputs the standard error, confidence limits, t value, and Pr >  probability for each

probability for each  in the parameter estimates table. Table 14.5 summarizes these statistics for .

in the parameter estimates table. Table 14.5 summarizes these statistics for .

Table 14.5: More Statistics for

|

Statistic |

Definition |

|

|---|---|---|

|

Standard error: |

|

|

|

|

|

|

|

t value |

|

|

|

Pr > |

p-value of the t value |

Here  is the

is the  element of , and

element of , and  denotes the

denotes the  -level student’s t score with 1 degree of freedom.

-level student’s t score with 1 degree of freedom.