The TCOUNTREG Procedure (Experimental)

- Overview

- Getting Started

-

Syntax

-

Details

Specification of Regressors Missing Values Poisson Regression Negative Binomial Regression Zero-Inflated Count Regression Overview Zero-Inflated Poisson Regression Zero-Inflated Negative Binomial Regression Variable Selection Panel Data Analysis Computational Resources Nonlinear Optimization Options Covariance Matrix Types Displayed Output OUTPUT OUT= Data Set OUTEST= Data Set ODS Table Names

-

Examples

- References

| Panel Data Analysis |

Panel Data Poisson Regression with Fixed Effects

The count regression model for panel data can be derived from the Poisson regression model. Consider the multiplicative one-way panel data model,

|

where

|

Here,  are the individual effects.

are the individual effects.

In the fixed effects model, the are unknown parameters. The fixed effects model can be estimated by eliminating by conditioning on  .

.

In the random effects model, the are independent and identically distributed (iid) random variables, in contrast to the fixed effects model. The random effects model can then be estimated by assuming a distribution for .

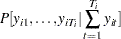

In the Poisson fixed effects model, conditional on  and parameter ,

and parameter ,  is iid Poisson distributed with parameter

is iid Poisson distributed with parameter  , and

, and  does not include an intercept. Then, the conditional joint density for the outcomes within the

does not include an intercept. Then, the conditional joint density for the outcomes within the  th panel is

th panel is

|

|

|

|||

|

|

|

Since is iid Poisson( ),

),  is the product of

is the product of  Poisson densities. Also,

Poisson densities. Also,  is Poisson(

is Poisson( ). Then,

). Then,

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

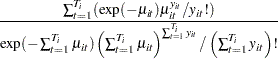

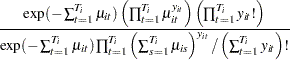

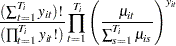

Thus, the conditional log-likelihood function of the fixed effects Poisson model is given by

|

The gradient is

|

|

|

|||

|

|

|

where

|

Panel Data Poisson Regression with Random Effects

In the Poisson random effects model, conditional on and parameter , is iid Poisson distributed with parameter , and the individual effects, , are assumed to be iid random variables. The joint density for observations in all time periods for the th individual,  , can be obtained after the density

, can be obtained after the density  of

of  is specified.

is specified.

Let

|

so that  and

and  :

:

|

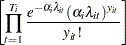

Let  . Since is conditional on and parameter is iid Poisson(

. Since is conditional on and parameter is iid Poisson( ), the conditional joint probability for observations in all time periods for the th individual,

), the conditional joint probability for observations in all time periods for the th individual,  , is the product of Poisson densities:

, is the product of Poisson densities:

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

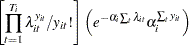

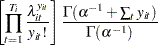

Then, the joint density for the th panel conditional on just the  can be obtained by integrating out :

can be obtained by integrating out :

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

where  is the overdispersion parameter. This is the density of the Poisson random effects model with gamma-distributed random effects. For this distribution,

is the overdispersion parameter. This is the density of the Poisson random effects model with gamma-distributed random effects. For this distribution,  and

and  ; that is, there is overdispersion.

; that is, there is overdispersion.

Then the log-likelihood function is written as

|

|

|

|||

|

|

|

|||

|

|

|

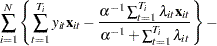

The gradient is

|

|

|

|||

|

|

|

|||

|

|

|

and

|

|

|

|||

|

|

|

where  ,

,  and

and  is the digamma function.

is the digamma function.

Panel Data Negative Binomial Regression with Fixed Effects

This section shows the derivation of a negative binomial model with fixed effects. Keep the assumptions of the Poisson-distributed dependent variable

|

But now let the Poisson parameter be random with gamma distribution and parameters  ,

,

|

where one of the parameters is the exponentially affine function of independent variables  . Use integration by parts to obtain the distribution of ,

. Use integration by parts to obtain the distribution of ,

|

|

|

|||

|

|

|

which is a negative binomial distribution with parameters . Conditional joint distribution is given as

|

|

|

|||

|

|

|

Hence, the conditional fixed-effects negative binomial log-likelihood is

|

|

|

|||

|

|

|

The gradient is

|

|

|

|||

|

|

|

|||

|

|

|

Panel Data Negative Binomial Regression with Random Effects

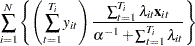

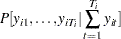

This section describes the derivation of negative binomial model with random effects. Suppose

|

with the Poisson parameter distributed as gamma,

|

where its parameters are also random:

|

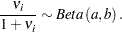

Assume that the distribution of a function of  is beta with parameters

is beta with parameters  :

:

|

Explicitly, the beta density with  domain is

domain is

|

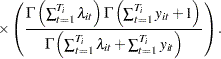

where  is the beta function. Then, conditional joint distribution of dependent variables is

is the beta function. Then, conditional joint distribution of dependent variables is

|

Integrating out the variable yields the following conditional distribution function:

|

|

|

|||

|

|

|

|||

|

|

|

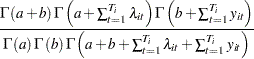

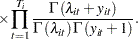

Consequently, the conditional log-likelihood function for a negative binomial model with random effects is

|

|

|

|||

|

|

|

|||

|

|

|

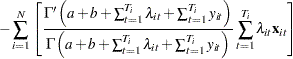

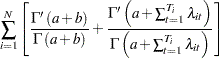

The gradient is

|

|

|

|||

|

|

|

|||

|

|

|

and

|

|

|

|||

|

|

|

and

|

|

|

|||

|

|

|

Note: This procedure is experimental.