The ENTROPY Procedure(Experimental)

- Overview

-

Getting Started

-

Syntax

-

DetailsGeneralized Maximum EntropyGeneralized Cross EntropyMoment Generalized Maximum EntropyMaximum Entropy-Based Seemingly Unrelated RegressionGeneralized Maximum Entropy for Multinomial Discrete Choice ModelsCensored or Truncated Dependent VariablesInformation MeasuresParameter Covariance For GCEParameter Covariance For GCE-MStatistical TestsMissing ValuesInput Data SetsOutput Data SetsODS Table NamesODS Graphics

-

Examples

- References

Generalized Maximum Entropy

Reparameterization of the errors in a regression equation is the process of specifying a support for the errors, observation

by observation. If a two-point support is used, the error for the tth observation is reparameterized by setting  , where

, where  and

and  are the upper and lower bounds for the tth error

are the upper and lower bounds for the tth error  , and

, and  and

and  represent the weight associated with the point and . The error distribution is usually chosen to be symmetric, centered around zero, and the same across observations so that

represent the weight associated with the point and . The error distribution is usually chosen to be symmetric, centered around zero, and the same across observations so that

, where R is the support value chosen for the problem (Golan, Judge, and Miller 1996).

, where R is the support value chosen for the problem (Golan, Judge, and Miller 1996).

The generalized maximum entropy (GME) formulation was proposed for the ill-posed or underdetermined case where there is insufficient

data to estimate the model with traditional methods.  is reparameterized by defining a support for (and a set of weights in the cross entropy case), which defines a prior distribution for .

is reparameterized by defining a support for (and a set of weights in the cross entropy case), which defines a prior distribution for .

In the simplest case, each  is reparameterized as

is reparameterized as  , where

, where  and

and  represent the probabilities ranging from [0,1] for each , and

represent the probabilities ranging from [0,1] for each , and  and

and  represent the lower and upper bounds placed on

represent the lower and upper bounds placed on  . The support points, and , are usually distributed symmetrically around the most likely value for based on some prior knowledge.

. The support points, and , are usually distributed symmetrically around the most likely value for based on some prior knowledge.

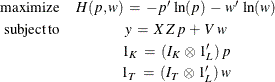

With these reparameterizations, the GME estimation problem is

where y denotes the column vector of length T of the dependent variable;  denotes the

denotes the  matrix of observations of the independent variables; p denotes the LK column vector of weights associated with the points in Z; w denotes the LT column vector of weights associated with the points in V;

matrix of observations of the independent variables; p denotes the LK column vector of weights associated with the points in Z; w denotes the LT column vector of weights associated with the points in V;  ,

,  , and

, and  are K-, L-, and T-dimensional column vectors, respectively, of ones; and

are K-, L-, and T-dimensional column vectors, respectively, of ones; and  and

and  are

are  and

and  dimensional identity matrices.

dimensional identity matrices.

These equations can be rewritten using set notation as follows:

![\[ \mr{maximize} \; \; \; H(p,w) \: = \: - \, \sum _{l=1}^{L} \, \sum _{k=1}^{K} \: p_{kl} \, \ln (p_{kl}) \: - \: \sum _{l=1}^{L} \, \sum _{t=1}^{T} \: w_{tl} \, \ln (w_{tl}) \]](images/etsug_entropy0063.png)

![\[ \mr{subject\, to} \; \; \; y_ t \: = \: \sum _{l=1}^{L} \left[ \, \sum _{k=1}^{K} \: \left( \, X_{kt} \, Z_{kl} \, p_{kl} \right) \: + \: V_{tl} \, w_{tl} \right] \]](images/etsug_entropy0064.png)

![\[ \; \; \; \; \; \; \; \; \; \; \; \; \; \; \; \; \; \; \sum _{l=1}^{L} \: p_{kl}\: = \: 1 \; \; \mr{and} \; \; \sum _{l=1}^{L} \: w_{tl} \: = \: 1 \]](images/etsug_entropy0065.png)

The subscript l denotes the support point (l=1, 2, ..., L), k denotes the parameter (k=1, 2, ..., K), and t denotes the observation (t=1, 2, ..., T).

The GME objective is strictly concave; therefore, a unique solution exists. The optimal estimated probabilities, p and w, and the prior supports, Z and V, can be used to form the point estimates of the unknown parameters, , and the unknown errors, e.