| The ROBUSTREG Procedure |

| M Estimation |

M estimation in the context of regression was first introduced by Huber (1973) as a result of making the least squares approach robust. Although M estimators are not robust with respect to leverage points, they are popular in applications where leverage points are not an issue.

Instead of minimizing a sum of squares of the residuals, a Huber-type M estimator  of

of  minimizes a sum of less rapidly increasing functions of the residuals:

minimizes a sum of less rapidly increasing functions of the residuals:

|

where  . For the ordinary least squares estimation,

. For the ordinary least squares estimation,  is the square function,

is the square function,  .

.

If  is known, then by taking derivatives with respect to , is also a solution of the system of

is known, then by taking derivatives with respect to , is also a solution of the system of  equations:

equations:

|

where  . If is convex, is the unique solution.

. If is convex, is the unique solution.

The ROBUSTREG procedure solves this system by using iteratively reweighted least squares (IRLS). The weight function  is defined as

is defined as

|

The ROBUSTREG procedure provides 10 kinds of weight functions through the WEIGHTFUNCTION= option in the MODEL statement. Each weight function corresponds to a function. See the section Weight Functions for a complete discussion. You can specify the scale parameter with the SCALE= option in the PROC statement.

If is unknown, both and are estimated by minimizing the function

|

The algorithm proceeds by alternately improving  in a location step and

in a location step and  in a scale step.

in a scale step.

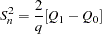

For the scale step, three methods are available to estimate , which you can select with the SCALE= option.

(SCALE=HUBER<(D=d)>) Compute

by the iteration

where

is the Huber function and

is the Huber constant (refer to Huber 1981, p. 179). You can specify

is the Huber constant (refer to Huber 1981, p. 179). You can specify  with the D= option. By default,

with the D= option. By default,  .

. (SCALE=TUKEY<(D=d)>) Compute

by solving the supplementary equation

by solving the supplementary equation

where

Here

is Tukey’s bisquare function, and

is Tukey’s bisquare function, and  is the constant such that the solution is asymptotically consistent when

is the constant such that the solution is asymptotically consistent when  (refer to Hampel et al. 1986, p. 149). You can specify with the D= option. By default, .

(refer to Hampel et al. 1986, p. 149). You can specify with the D= option. By default, . (SCALE=MED) Compute

by the iteration

where

is the constant such that the solution is asymptotically consistent when (refer to Hampel et al. 1986, p. 312).

is the constant such that the solution is asymptotically consistent when (refer to Hampel et al. 1986, p. 312).

Note that SCALE = MED is the default.

Algorithm

The basic algorithm for computing M estimates for regression is iteratively reweighted least squares (IRLS). As the name suggests, a weighted least squares fit is carried out inside an iteration loop. For each iteration, a set of weights for the observations is used in the least squares fit. The weights are constructed by applying a weight function to the current residuals. Initial weights are based on residuals from an initial fit. The ROBUSTREG procedure uses the unweighted least squares fit as a default initial fit. The iteration terminates when a convergence criterion is satisfied. The maximum number of iterations is set to 1000. You can specify the weight function and the convergence criteria.

Weight Functions

You can specify the weight function for M estimation with the WEIGHTFUNCTION= option. The ROBUSTREG procedure provides 10 weight functions. By default, the procedure uses the bisquare weight function. In most cases, M estimates are more sensitive to the parameters of these weight functions than to the type of the weight function. The median weight function is not stable and is seldom recommended in data analysis; it is included in the procedure for completeness. You can specify the parameters for these weight functions. Except for the hampel and median weight functions, default values for these parameters are defined such that the corresponding M estimates have  asymptotic efficiency in the location model with the Gaussian distribution (see Holland and Welsch 1977).

asymptotic efficiency in the location model with the Gaussian distribution (see Holland and Welsch 1977).

The following list shows the weight functions available. See Table 74.5 for the default values of the constants in these weight functions.

andrews |

|

|

bisquare |

|

|

cauchy |

|

|

fair |

|

|

hampel |

|

|

huber |

|

|

logistic |

|

|

median |

|

|

talworth |

|

|

welsch |

|

|

Convergence Criteria

The following convergence criteria are available in PROC ROBUSTREG:

relative change in the coefficients (CONVERGENCE= COEF)

relative change in the scaled residuals (CONVERGENCE= RESID)

relative change in weights (CONVERGENCE= WEIGHT)

You can specify the criteria with the CONVERGENCE= option in the PROC statement. The default is CONVERGENCE= COEF.

You can specify the precision of the convergence criterion with the EPS= suboption. The default is EPS=1.E 8.

8.

In addition to these convergence criteria, a convergence criterion based on scale-independent measure of the gradient is always checked. See Coleman et al. (1980) for more details. A warning is issued if this criterion is not satisfied.

Asymptotic Covariance and Confidence Intervals

The following three estimators of the asymptotic covariance of the robust estimator are available in PROC ROBUSTREG:

|

|

|

where  is a correction factor and

is a correction factor and  . Refer to Huber (1981, p. 173) for more details.

. Refer to Huber (1981, p. 173) for more details.

You can specify the asymptotic covariance estimate with the option ASYMPCOV= option. The ROBUSTREG procedure uses H1 as the default because of its simplicity and stability. Confidence intervals are computed from the diagonal elements of the estimated asymptotic covariance matrix.

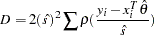

R Square and Deviance

The robust version of  is defined as

is defined as

|

and the robust deviance is defined as the optimal value of the objective function on the  scale:

scale:

|

where  ,

,  is the M estimator of ,

is the M estimator of ,  is the M estimator of location, and

is the M estimator of location, and  is the M estimator of the scale parameter in the full model.

is the M estimator of the scale parameter in the full model.

Linear Tests

Two tests are available in PROC ROBUSTREG for the canonical linear hypothesis

|

where  is the total number of parameters of the tested effects. The first test is a robust version of the

is the total number of parameters of the tested effects. The first test is a robust version of the  test, which is referred to as the test. Denote the M estimators in the full and reduced model as

test, which is referred to as the test. Denote the M estimators in the full and reduced model as  and

and  , respectively. Let

, respectively. Let

|

|

|

|||

|

|

|

with

|

The robust test is based on the test statistic

|

Asymptotically  under

under  , where the standardization factor is

, where the standardization factor is

and

and  is the cumulative distribution function of the standard normal distribution. Large values of

is the cumulative distribution function of the standard normal distribution. Large values of  are significant. This test is a special case of the general

are significant. This test is a special case of the general  test of Hampel et al. (1986, Section 7.2).

test of Hampel et al. (1986, Section 7.2).

The second test is a robust version of the Wald test, which is referred to as  test. The test uses a test statistic

test. The test uses a test statistic

|

where  is the

is the  block (corresponding to

block (corresponding to  ) of the asymptotic covariance matrix of the M estimate

) of the asymptotic covariance matrix of the M estimate  of in a -parameter linear model.

of in a -parameter linear model.

Under , the statistic has an asymptotic  distribution with degrees of freedom. Large values of are significant. Refer to Hampel et al. (1986, Chapter 7) for more details.

distribution with degrees of freedom. Large values of are significant. Refer to Hampel et al. (1986, Chapter 7) for more details.

Model Selection

When M estimation is used, two criteria are available in PROC ROBUSTREG for model selection. The first criterion is a counterpart of the Akaike (1974) AIC criterion for robust regression, and it is defined as

|

where  , is a robust estimate of and is the M estimator with

, is a robust estimate of and is the M estimator with  -dimensional design matrix.

-dimensional design matrix.

As with AIC,  is the weight of the penalty for dimensions. The ROBUSTREG procedure uses

is the weight of the penalty for dimensions. The ROBUSTREG procedure uses  (Ronchetti 1985) and estimates it by using the final robust residuals.

(Ronchetti 1985) and estimates it by using the final robust residuals.

The second criterion is a robust version of the Schwarz information criteria (BIC), and it is defined as

|

Copyright © 2009 by SAS Institute Inc., Cary, NC, USA. All rights reserved.