The COPULA Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSklar’s TheoremDependence MeasuresNormal CopulaStudent’s t copulaArchimedean CopulasHierarchical Archimedean Copula (HAC)Canonical Maximum Likelihood Estimation (CMLE)Exact Maximum Likelihood Estimation (MLE)Calibration EstimationNonlinear Optimization OptionsDisplayed OutputOUTCOPULA= Data SetOUTPSEUDO=, OUT=, and OUTUNIFORM= Data SetsODS Table NamesODS Graph Names

-

Examples

- References

Let ![]() and let

and let ![]() be a univariate t distribution with

be a univariate t distribution with ![]() degrees of freedom.

degrees of freedom.

The Student’s t copula can be written as

where ![]() is the multivariate Student’s t distribution with a correlation matrix

is the multivariate Student’s t distribution with a correlation matrix ![]() with

with ![]() degrees of freedom.

degrees of freedom.

The input parameters for the simulation are ![]() . The t copula can be simulated by the following the two steps:

. The t copula can be simulated by the following the two steps:

-

Generate a multivariate vector

following the centered t distribution with

following the centered t distribution with  degrees of freedom and correlation matrix

degrees of freedom and correlation matrix  .

.

-

Transform the vector

into

into  , where

, where  is the distribution function of univariate t distribution with degrees of freedom.

is the distribution function of univariate t distribution with degrees of freedom.

To simulate centered multivariate t random variables, you can use the property that ![]() if

if ![]() , where

, where ![]() and the univariate random variable

and the univariate random variable ![]() .

.

To fit a t copula is to estimate the covariance matrix ![]() and degrees of freedom

and degrees of freedom ![]() from a given multivariate data set. Given a random sample

from a given multivariate data set. Given a random sample![]() ,

, ![]() that has uniform marginal distributions, the log likelihood is

that has uniform marginal distributions, the log likelihood is

where ![]() denotes the degrees of freedom of the t copula,

denotes the degrees of freedom of the t copula, ![]() denotes the joint density function of the centered multivariate t distribution with parameters

denotes the joint density function of the centered multivariate t distribution with parameters ![]() ,

, ![]() is the distribution function of a univariate t distribution with

is the distribution function of a univariate t distribution with ![]() degrees of freedom,

degrees of freedom, ![]() is a correlation matrix, and

is a correlation matrix, and ![]() is the density function of univariate t distribution with

is the density function of univariate t distribution with ![]() degrees of freedom.

degrees of freedom.

The log likelihood can be maximized with respect to the parameters ![]() using numerical optimization. If you allow the parameters in

using numerical optimization. If you allow the parameters in ![]() to be such that

to be such that ![]() is symmetric and with ones on the diagonal, then the MLE estimate for

is symmetric and with ones on the diagonal, then the MLE estimate for ![]() might not be positive semidefinite. In that case, you need to apply the adjustment to convert the estimated matrix to positive

semidefinite, as shown by McNeil, Frey, and Embrechts (2005), Algorithm 5.55.

might not be positive semidefinite. In that case, you need to apply the adjustment to convert the estimated matrix to positive

semidefinite, as shown by McNeil, Frey, and Embrechts (2005), Algorithm 5.55.

When the dimension of the data m increases, the numerical optimization quickly becomes infeasible. It is common practice to estimate the correlation matrix

![]() by calibration using Kendall’s tau. Then, using this fixed

by calibration using Kendall’s tau. Then, using this fixed ![]() , the single parameter

, the single parameter ![]() can be estimated by MLE. By proposition 5.37 in McNeil, Frey, and Embrechts (2005),

can be estimated by MLE. By proposition 5.37 in McNeil, Frey, and Embrechts (2005),

where ![]() is the Kendall’s tau and

is the Kendall’s tau and ![]() is the off-diagonal elements of the correlation matrix

is the off-diagonal elements of the correlation matrix ![]() of the t copula. Therefore, an estimate for the correlation is

of the t copula. Therefore, an estimate for the correlation is

where ![]() and

and ![]() are the estimates of the sample correlation matrix and Kendall’s tau, respectively. However, it is possible that the estimate

of the correlation matrix

are the estimates of the sample correlation matrix and Kendall’s tau, respectively. However, it is possible that the estimate

of the correlation matrix ![]() is not positive definite. In this case, there is a standard procedure that uses the eigenvalue decomposition to transform

the correlation matrix into one that is positive definite. Let

is not positive definite. In this case, there is a standard procedure that uses the eigenvalue decomposition to transform

the correlation matrix into one that is positive definite. Let ![]() be a symmetric matrix with ones on the diagonal, with off-diagonal entries in

be a symmetric matrix with ones on the diagonal, with off-diagonal entries in ![]() . If

. If ![]() is not positive semidefinite, use Algorithm 5.55 from McNeil, Frey, and Embrechts (2005):

is not positive semidefinite, use Algorithm 5.55 from McNeil, Frey, and Embrechts (2005):

-

Compute the eigenvalue decomposition

, where

, where  is a diagonal matrix that contains all the eigenvalues and

is a diagonal matrix that contains all the eigenvalues and  is an orthogonal matrix that contains the eigenvectors.

is an orthogonal matrix that contains the eigenvectors.

-

Construct a diagonal matrix

by replacing all negative eigenvalues in by a small value

by replacing all negative eigenvalues in by a small value  .

.

-

Compute

, which is positive definite but not necessarily a correlation matrix.

, which is positive definite but not necessarily a correlation matrix.

-

Apply the normalizing operator

on the matrix

on the matrix  to obtain the correlation matrix desired.

to obtain the correlation matrix desired.

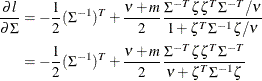

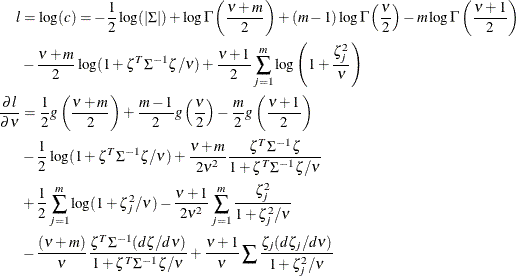

The log likelihood function and its gradient function for a single observation are listed as follows, where ![]() , with

, with ![]() , and g is the derivative of the

, and g is the derivative of the ![]() function:

function:

The derivative of the likelihood with respect to the correlation matrix ![]() follows:

follows: