The X12 Procedure

- Overview

-

Getting Started

-

SyntaxFunctional SummaryPROC X12 StatementADJUST StatementARIMA StatementAUTOMDL StatementBY StatementCHECK StatementESTIMATE StatementEVENT StatementFORECAST StatementID StatementIDENTIFY StatementINPUT StatementOUTLIER StatementOUTPUT StatementPICKMDL StatementREGRESSION StatementSEATSDECOMP StatementTABLES StatementTRANSFORM StatementUSERDEFINED StatementVAR StatementX11 Statement

-

DetailsData RequirementsMissing ValuesSAS Predefined EventsUser-Defined Regression VariablesCombined Test for the Presence of Identifiable SeasonalityComputationsPICKMDL Model SelectionSEATS DecompositionDisplayed Output, ODS Table Names, and OUTPUT Tablename KeywordsUsing Auxiliary Variables to Subset Output Data SetsODS GraphicsOUT= Data SetSEATSDECOMP OUT= Data SetSpecial Data Sets

-

ExamplesARIMA Model IdentificationModel EstimationSeasonal AdjustmentRegARIMA Automatic Model SelectionAutomatic Outlier DetectionUser-Defined RegressorsMDLINFOIN= and MDLINFOOUT= Data SetsSetting Regression ParametersCreating an MDLINFO= Data Set for Use with the PICKMDL StatementIllustration of ODS GraphicsAUXDATA= Data Set

- References

REGRESSION Statement

REGRESSION regression-group-options ;

REGRESSION PREDEFINED= variables < / B=(value <F> …) > ;

REGRESSION USERVAR= variables < / B=(value <F> …) USERTYPE=(values) > ;

The REGRESSION statement includes regression variables in a regARIMA model or specifies regression variables whose effects are to be removed by the IDENTIFY statement to aid in ARIMA model identification. Include the PREDEFINED= option to select predefined regression variables. Include the USERVAR= option to specify user-defined regression variables.

Table 38.3 shows the X-12-ARIMA tables that contain regression factors. Tables A8AO, A8LS, and A8TC are available only when more than one outlier type is present in the model.

Table 38.3: X-12-ARIMA Regression Effects Tables

|

Table |

Regression Effects |

|---|---|

|

A6 |

Trading day effects |

|

A7 |

Holiday effects including Easter, Labor Day, and Thanksgiving-Christmas |

|

A8 |

Combined effects of outliers, level shifts, ramps, and temporary changes |

|

A8AO |

Point outlier effects; available only when more than one outlier type is present in the model |

|

A8LS |

Level shift and ramp effects; available only when more than one outlier type is present in the model |

|

A8TC |

Temporary change effects; available only when more than one outlier type is present in the model |

|

A9 |

User-defined regression effects |

|

A10 |

User-defined seasonal component effects |

Missing values in the span of an input series automatically create missing value regressors. See the NOTRIMMISS option in the PROC X12 statement and the section Missing Values for further details about missing values.

Combining your model with additional predefined regression variables can result in a singularity problem. To successfully perform the regression if a singularity occurs, you might need to alter either the model or the choices of the regressors.

To seasonally adjust a series that uses a regARIMA model, the factors derived from regression are used as multiplicative or additive factors, depending on the mode of seasonal decomposition. Therefore, regressors that are appropriate to the mode of the seasonal decomposition should be defined, so that meaningful combined adjustment factors can be derived and adjustment diagnostics can be generated. For example, if a regARIMA model is applied to a log-transformed series, then the regression factors are expressed as ratios, which match the form of the seasonal factors that are generated by the multiplicative or log-additive adjustment modes. Conversely, if a regARIMA model is fit to the original series, then the regression factors are measured on the same scale as the original series, which matches the scale of the seasonal factors that are generated by the additive adjustment mode. Note that the default transformation (no transformation) and the default seasonal adjustment mode (multiplicative) are in conflict. Thus, when you specify the X11 statement and any of the REGRESSION, INPUT, or EVENT statements, you must also either use the TRANSFORM statement to specify a transformation or use the MODE= option in the X11 statement to specify a different mode to seasonally adjust the data that uses the regARIMA model.

According to Ladiray and Quenneville (2001), “X-12-ARIMA is based on the same principle [as the X-11 method] but proposes, in addition, a complete module, called Reg-ARIMA, that allows for the initial series to be corrected for all sorts of undesirable effects. These effects are estimated using regression models with ARIMA errors (Findley et al. [23]).” The REGRESSION, INPUT, and EVENT statements specify these regression effects. Predefined effects that can be corrected in this manner are listed in the PREDEFINED= option. You can create your own definitions to remove other effects by using the USERVAR= option and the EVENT statement.

You can specify either the PREDEFINED= option or the USERVAR= option, but not both, in a single REGRESSION statement. You can use multiple REGRESSION statements.

You can specify the following regression-group-options in the REGRESSION statement. The regression-group-options apply to all regression variables in a regression group. For predefined regression variables, the regression group is predefined. For user-defined regression variables, you can specify the regression group in the USERTYPE= option.

You can specify the following regression variable specification options in the REGRESSION statement.

-

PREDEFINED=CONSTANT | EASTER(value) | LABOR(value) | LOM | LOMSTOCK | LOQ | LPYEAR

PREDEFINED=SCEASTER(value) | SEASONAL | SINCOS(value …) | TD | TD1COEF

PREDEFINED=TD1NOLPYEAR | TDNOLPYEAR | TDSTOCK(value) | THANK(value) -

lists the predefined regression variables to be included in the model. Data values for these variables are calculated by the program, mostly as functions of the calendar. Table 38.5 gives definitions for the available predefined variables. The values LOM and LOQ are equivalent: the actual regression is controlled by the SEASONS= option in the PROC X12 statement. You can specify multiple predefined regression variables. The syntax for using both a length-of-month and a seasonal regression can be in one of the following forms:

regression predefined=lom seasonal; regression predefined=(lom seasonal); regression predefined=lom predefined=seasonal;

The following restrictions apply when you use more than one predefined regression variable:

-

You can specify only one of TD, TDNOLPYEAR, TD1COEF, or TD1NOLPYEAR.

-

You cannot specify LPYEAR with TD, TD1COEF, LOM, LOMSTOCK, or LOQ.

-

You cannot specify LOM or LOQ with TD or TD1COEF.

-

If you specify the SINCOS predefined regression variable, then you must also specify the INTERVAL= option or the SEASONS= option in the PROC X12 statement because there are restrictions on this regression variable that are based on the frequency of the data.

The predefined regression variables, EASTER, LABOR, SCEASTER, SINCOS, TDSTOCK, and THANK, require extra parameters. Only one TDSTOCK regressor can be implemented in the regression model. If you specify multiple TDSTOCK variables, PROC X12 uses the last TDSTOCK variable specified. For EASTER, LABOR, SCEASTER, SINCOS, and THANK, you can specify the variables with different parameters to implement multiple regressors in the model. For example, the following statement specifies two EASTER regressors with widths 7 and 14:

regression predefined=easter(7) easter(14);

For SINCOS, specifying a parameter includes both the sine and the cosine regressor except for the highest order allowed (2 for quarterly data and 6 for monthly data.) For quarterly data, the following statement is the most common use of the SINCOS variable; it includes three regressors in the model:

regression predefined=sincos(1,2);

For monthly data, the following statement is the most common use of the SINCOS variable; it includes 11 regressors in the model:

regression predefined=sincos(1,2,3,4,5,6);

Table 38.5: Predefined Regression Variables in X-12-ARIMA

Regression Effect

Variable Definitions

Trend constant

CONSTANT

where

and

and

is the number of the

is the number of the  days before Easter that fall in month

days before Easter that fall in month

Easter holiday

(or quarter)

. (Note: This variable is

. (Note: This variable is  except in February, March,

except in February, March,

EASTER(

)

and April (or first and second quarter).

It is nonzero in February only for

.)

.)

Restriction:

.

.

Labor Day

![$L(w,t) = \frac{1}{w} \times [\text {no. of the } w \text { days before Labor Day that fall in month } t]$](images/etsug_x120034.png)

LABOR(

)

(Note: This variable is

except in August and September.)

Restriction:

.

Length-of-month

where

where  = length of month (in days)

= length of month (in days)

(monthly flow)

and

(average length of month)

(average length of month)

LOM

Stock length-of-month

LOMSTOCK

where

and are defined in LOM and

and are defined in LOM and

Length-of-quarter

where

where  = length of quarter (in days)

= length of quarter (in days)

(quarterly flow)

and

(average length of quarter)

(average length of quarter)

LOQ

Leap year

(monthly and quarterly flow)

LPYEAR

Statistics Canada Easter

If Easter falls before April

, let  be the number of the days

be the number of the days

(monthly or quarterly flow)

on or before Easter that fall in March. Then:

SCEASTER(

)

If Easter falls on or after April

, then  .

.

(Note: This variable is

except in March and April (or first and

second quarter).) Restriction:

.

.

Fixed seasonal

SEASONAL

Fixed seasonal

SINCOS(

)

)

, and

, and  is the seasonal period

is the seasonal period

SINCOS(

)

)

for

for  )

)

Restrictions:

,

,  .

.

Trading day

TD, TDNOLPYEAR

One coefficient trading day

TD1COEF, TD1NOLPYEAR

Stock trading day

TDSTOCK(

)

where

is the smaller of and the length of month .

is the smaller of and the length of month .

For end-of-month stock series, set

to 31; that is,

specify TDSTOCK(31). Restriction:

.

.

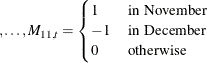

Thanksgiving

proportion of days from days before Thanksgiving

proportion of days from days before Thanksgiving

THANK(

)

through December 24 that fall in month

(negative values of indicate

days after Thanksgiving).

(Note: This variable is

except in November and December.)

Restriction:

.

.

-

- USERVAR=(variables)

-

specifies variables in the DATA= or AUXDATA= data set (which are specified in the PROC X12 statement) that are to be used as regressors. The variables in the data set should contain the values for each observation that define the regressor. Regression variables should also include future values in the data set for the forecast horizon if the time series is to be extended with regARIMA forecasts. Regression variables should include past values if the time series is to be extended with regARIMA backcasts. Missing values are not permitted within the data span, including backcasts and forecasts, of the user-defined regressors. Example 38.6 shows how to create an input data set that contains both the series to be seasonally adjusted and a user-defined input variable. Example 38.11 shows how to create an auxiliary data set that contains a user-defined input variable. For more information about specifying user-defined regression variables see the section User-Defined Regression Variables.

All regression variables in the USERVAR= option apply to all time series to be seasonally adjusted unless the MDLINFOIN= data set specifies different regression information. You cannot specify the PREDEFINED= option and the USERVAR= option in the same REGRESSION statement; however, you can specify multiple REGRESSION statements.

You can specify the following options for individual regression variables. Individual regression variable options are specified in the PREDEFINED= and USERVAR= options after the slash. The B= option can be specified in both the PREDEFINED= and USERVAR= options. Because the regression group is predefined for predefined variables, you can specify the USERTYPE= option only in the USERVAR= option.

- B=(value <F> …)

-

specifies initial or fixed values for the regression parameters in the order in which they appear in a PREDEFINED= or USERVAR= option. Each B= list applies to the PREDEFINED= or USERVAR= variable list that immediately precedes the slash.

For example, the following statements set an initial value of 1 for the user-defined regressor,

x:regression predefined=LOM ; regression uservar=x / b=1 2 ;

In this example, the B= option applies only to the USERVAR= option. The value 2 is discarded because there is only one variable in the USERVAR= list.

To assign an initial value of 1 to the LOM regressor and 2 to the

xregressor, use the following statements:regression predefined=LOM / b=1; regression uservar=x / b=2 ;

An F immediately following the numerical value indicates that this is not an initial value, but a fixed value. See Example 38.8 for an example that uses fixed parameters. In PROC X12, individual parameters can be fixed while other parameters in the same model are estimated.

- USERTYPE=(values)

-

enables a variable that you define to be processed in the same manner as a U.S. Census predefined variable. You can specify the following values: AO, CONSTANT, EASTER, HOLIDAY, LABOR, LOM, LOMSTOCK, LOQ, LPYEAR, LS, RP, SCEASTER, SEASONAL, TC, TD, TDSTOCK, THANKS, or USER. For example, the U.S. Census Bureau EASTER(

) regression effects are included the “RegARIMA Holiday Component” table (A7). Specify USERTYPE=EASTER to define a variable that is processed exactly as the U.S. Census predefined EASTER() variable, including inclusion in the A7 table. Each USERTYPE= list applies to the USERVAR= variable list that immediately

precedes the slash. USERTYPE= does not apply to U.S. Census predefined variables.

The same rules for assigning B= values to regression variables apply for USERTYPE= options. For example, the following statements specify that the user-defined regressor in the variable

MyEasterbe processed exactly as the U.S. Census predefined LOM variable:regression uservar=MyLOM; regression uservar=MyEaster / usertype=LOM EASTER;

In this example, the USERTYPE= option applies only to the

MyEastervariable in the second REGRESSION statement. The USERTYPE value EASTER is discarded because there is only one variable in the USERVAR= list.To assign the USERTYPE value LOM to the

MyLOMvariable and EASTER to theMyEastervariable, use the following statements:regression uservar=MyLOM / usertype=LOM; regression uservar=MyEaster / usertype=EASTER;

The following USERTYPE= options specify that the regression effect be removed from the seasonally adjusted series: EASTER, HOLIDAY, LABOR, LOM, LOMSTOCK, LOQ, LPYEAR, SCEASTER, SEASONAL, TD, TDSTOCK, THANKS, and USER. When a regression effect is removed from the seasonally adjusted series, the level (mean) of the seasonally adjusted series can be altered. It is often desirable to use a zero-mean (mean-adjusted) regressor for effects that are to be removed from the seasonally adjusted series. See Example 38.6 for an example that specifies a zero-mean regressor.