The QUANTSELECT Procedure

Criteria Used in Model Selection Methods

PROC QUANTSELECT supports a variety of fit statistics that you can specify as criteria for the CHOOSE= , SELECT= , and STOP= method-options in the MODEL statement.

Single Quantile Effect Selection

The following fit statistics are available for single quantile effect selection:

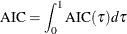

- AIC

-

applies the Akaike’s information criterion (Akaike 1981; Darlington 1968; Judge et al. 1985).

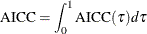

- AICC

-

applies the corrected Akaike’s information criterion (Hurvich and Tsai 1989).

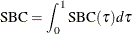

- SBC

-

applies the Schwarz Bayesian information criterion (Schwarz 1978; Judge et al. 1985).

- SL<(LR1 | LR2)>

-

specifies the significance level of a statistic used to assess an effect’s contribution to the fit when it is added to or removed from a model. LR1 specifies likelihood ratio Type I, and LR2 specifies the likelihood ratio Type II. By default, the LR1 statistic is applied.

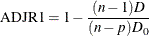

- ADJR1

-

applies the adjusted quantile regression R statistic.

- VALIDATE

-

applies the average check loss for the validation data.

Table 96.11 provides formulas and definitions for these fit statistics.

Table 96.11: Formulas and Definitions for Model Fit Summary Statistics for Single Quantile Effect Selection

|

Statistic |

Definition or Formula |

|---|---|

|

n |

Number of observations |

|

p |

Number of parameters including the intercept |

|

|

Residual for the ith observation; |

|

|

Total sum of check losses; |

|

|

Total sum of check losses for intercept-only model if intercept is a forced-in effect, otherwise for empty-model. |

|

|

Average check loss; |

|

|

Counterpart of linear regression R-square for quantile regression; |

|

|

Adjusted R1; |

|

|

Akaike’s information criterion; |

|

|

Corrected Akaike’s information criterion; |

|

|

Schwarz Bayesian information criterion; |

Quantile Process Effect Selection

The following statistics are available for quantile process effect selection:

- AIC

-

specifies Akaike’s information criterion (Akaike 1981; Darlington 1968; Judge et al. 1985).

- AICC

-

specifies the corrected Akaike’s information criterion (Hurvich and Tsai 1989).

- SBC

-

specifies Schwarz Bayesian information criterion (Schwarz 1978; Judge et al. 1985).

- ADJR1

-

specifies the adjusted quantile regression R statistic.

- VALIDATE

-

specifies average check loss for the validation data.

Table 96.12 provides formulas and definitions for the fit statistics.

Table 96.12: Formulas and Definitions for Model Fit Summary Statistics for Quantile Process Effect Selection

|

Statistic |

Definition or Formula |

|---|---|

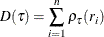

|

D |

Integral of total sum of check losses; |

|

|

Integral of total sum of check losses for intercept-only model or empty-model if the NOINT option is used; |

|

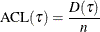

|

Integral of average check loss; |

|

|

Counterpart of linear regression R-square for quantile process regression; |

|

|

Adjusted R1; |

|

|

Akaike’s information criterion; |

|

|

Corrected Akaike’s information criterion; |

|

|

Schwarz Bayesian information criterion; |