| The OPTQP Procedure |

Example 17.3: Portfolio Selection with Transactions

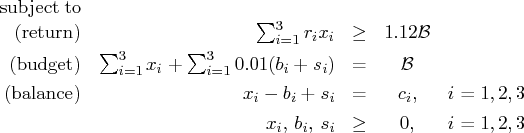

Consider a portfolio selection problem with a slight modification. You are now required to take into account the current position and transaction costs associated with buying and selling assets. The objective is to find the minimum variance portfolio. In order to understand the scenario better, consider the following data.

You are given three assets. The current holding of the three assets is denoted

by the vector ![]() = [200, 300, 500], the amount of asset bought and

sold is denoted by

= [200, 300, 500], the amount of asset bought and

sold is denoted by ![]() and

and ![]() , respectively, and the net

investment in each asset is denoted by

, respectively, and the net

investment in each asset is denoted by ![]() and is defined by the following relation:

and is defined by the following relation:

![\mathcal{c} & = & [ 0.027489 & -0.00874 & -0.00015 \ -0.00874 & 0.109449 & -0.00012 \ -0.00015 & -0.00012 & 0.000766 \ ]\](images/optqp_optqpeq115.gif)

The QPS-format input data set is as follows:

data potrdata;

input field1 $ field2 $ field3$ field4 field5 $ field6 @;

datalines;

NAME . POTRAN . . .

ROWS . . . . .

N OBJ.FUNC . . . .

G RETURN . . . .

E BUDGET . . . .

E BALANC1 . . . .

E BALANC2 . . . .

E BALANC3 . . . .

COLUMNS . . . . .

. X1 RETURN 1.109048 BUDGET 1.0

. X1 BALANC1 1.0 . .

. X2 RETURN 1.169048 BUDGET 1.0

. X2 BALANC2 1.0 . .

. X3 RETURN 1.074286 BUDGET 1.0

. X3 BALANC3 1.0 . .

. B1 BUDGET .01 BALANC1 -1.0

. B2 BUDGET .01 BALANC2 -1.0

. B3 BUDGET .01 BALANC3 -1.0

. S1 BUDGET .01 BALANC1 1.0

. S2 BUDGET .01 BALANC2 1.0

. S3 BUDGET .01 BALANC3 1.0

RHS . . . . .

. RHS RETURN 1120 . .

. RHS BUDGET 1000 . .

. RHS BALANC1 200 . .

. RHS BALANC2 300 . .

. RHS BALANC3 500 . .

RANGES . . . . .

BOUNDS . . . . .

QUADOBJ . . . . .

. X1 X1 0.054978 . .

. X1 X2 -.01748 . .

. X1 X3 -.0003 . .

. X2 X2 0.218898 . .

. X2 X3 -.00024 . .

. X3 X3 0.001532 . .

ENDATA . . . . .

;

Use the following SAS code to solve the problem:

proc optqp data=potrdata

primalout = potrpout

dualout = potrdout;

run;

The optimal solution is displayed in Output 17.3.1.

Output 17.3.1: Portfolio Selection with Transactions

Copyright © 2008 by SAS Institute Inc., Cary, NC, USA. All rights reserved.