| The Linear Programming Solver |

Overview

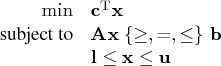

The OPTMODEL procedure provides a framework for specifying and solving linear programs (LPs). A standard linear program has the following formulation:

| is the vector of decision variables | |||

| is the matrix of constraints | |||

| is the vector of objective function coefficients | |||

| is the vector of constraints right-hand sides (RHS) | |||

| is the vector of lower bounds on variables | |||

| is the vector of upper bounds on variables |

The following LP solvers are available in the OPTMODEL procedure:

- primal simplex solver

- dual simplex solver

- interior point solver (experimental)

The simplex solvers implement the two-phase simplex method. In phase I, the solver tries to find a feasible solution. If no feasible solution is found, the LP is infeasible; otherwise, the solver enters phase II to solve the original LP. The interior point solver implements a primal-dual predictor-corrector interior point algorithm. If any of the decision variables are constrained to be integer-valued, then the relaxed version of the problem is solved.

Copyright © 2008 by SAS Institute Inc., Cary, NC, USA. All rights reserved.