The HPPANEL Procedure

- Overview

- Getting Started

-

Syntax

-

DetailsSpecifying the Input DataSpecifying the Regression ModelSpecifying the Number of Nodes and Number of ThreadsUnbalanced DataOne-Way Fixed-Effects ModelTwo-Way Fixed-Effects ModelBalanced PanelsUnbalanced PanelsOne-Way Random-Effects ModelTwo-Way Random-Effects ModelBetween EstimatorsPooled EstimatorLinear Hypothesis TestingSpecification TestsOUTPUT OUT= Data SetOUTEST= Data SetPrinted OutputODS Table Names

-

Example

- References

Unbalanced Panels

Let  and

and  be the independent and dependent variables, respectively, that are arranged by time and by cross section within each time

period. (Note that the input data set that the PANEL procedure uses must be sorted by cross section and then by time within

each cross section.) Let

be the independent and dependent variables, respectively, that are arranged by time and by cross section within each time

period. (Note that the input data set that the PANEL procedure uses must be sorted by cross section and then by time within

each cross section.) Let  be the number of cross sections that are observed in year

be the number of cross sections that are observed in year  , and let

, and let  . Let

. Let  be the

be the  matrix that is obtained from the

matrix that is obtained from the  identity matrix from which rows that correspond to cross sections that are not observed at time have been omitted. Consider

identity matrix from which rows that correspond to cross sections that are not observed at time have been omitted. Consider

![\[ \mb{Z} =(\mb{Z} _{1}, \mb{Z} _{2}) \]](images/etsug_hppanel0069.png)

where  and

and  . The matrix

. The matrix  contains the dummy variable structure for the two-way model.

contains the dummy variable structure for the two-way model.

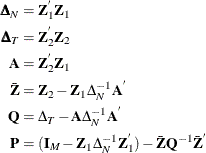

Let

The estimate of the regression slope coefficients is given by

![\[ \tilde{{\beta }}_{s}= ( \mb{X} ^{'}_{{\ast } s}\mb{PX} _{{\ast }s})^{-1} \mb{X} ^{'}_{{\ast } s}\mb{Py} _{{\ast }} \]](images/etsug_hppanel0074.png)

where  is the

is the  matrix without the vector of 1s.

matrix without the vector of 1s.

The estimator of the error variance is

![\[ \hat{{\sigma }}^{2}_{{\epsilon }}= \tilde{\mb{u} }^{'}\mb{P} \tilde{\mb{u} } / (\mi{M}-\mi{T}-\mi{N} +1-(\mi{K} -1)) \]](images/etsug_hppanel0077.png)

where the residuals are given by  if there is an intercept in the model and by

if there is an intercept in the model and by  if there is no intercept.

if there is no intercept.

The actual implementation is quite different from the theory. For more information, see the section Two-Way Fixed-Effects Model.