The TCOUNTREG Procedure (Experimental)

- Overview

- Getting Started

-

Syntax

-

DetailsSpecification of RegressorsMissing ValuesPoisson RegressionNegative Binomial RegressionZero-Inflated Count Regression OverviewZero-Inflated Poisson RegressionZero-Inflated Negative Binomial RegressionVariable SelectionPanel Data AnalysisComputational ResourcesNonlinear Optimization OptionsCovariance Matrix TypesDisplayed OutputOUTPUT OUT= Data SetOUTEST= Data SetODS Table NamesODS Graphics

-

Examples

- References

The count regression model for panel data can be derived from the Poisson regression model. Consider the multiplicative one-way panel data model,

where

Here, ![]() are the individual effects.

are the individual effects.

In the fixed effects model, the ![]() are unknown parameters. The fixed effects model can be estimated by eliminating

are unknown parameters. The fixed effects model can be estimated by eliminating ![]() by conditioning on

by conditioning on ![]() .

.

In the random effects model, the ![]() are independent and identically distributed (iid) random variables, in contrast to the fixed effects model. The random effects

model can then be estimated by assuming a distribution for

are independent and identically distributed (iid) random variables, in contrast to the fixed effects model. The random effects

model can then be estimated by assuming a distribution for ![]() .

.

In the Poisson fixed effects model, conditional on ![]() and parameter

and parameter ![]() ,

, ![]() is iid Poisson distributed with parameter

is iid Poisson distributed with parameter ![]() , and

, and ![]() does not include an intercept. Then, the conditional joint density for the outcomes within the

does not include an intercept. Then, the conditional joint density for the outcomes within the ![]() th panel is

th panel is

|

|

|

|

|

|

|

|

Since ![]() is iid Poisson(

is iid Poisson(![]() ),

), ![]() is the product of

is the product of ![]() Poisson densities. Also,

Poisson densities. Also, ![]() is Poisson(

is Poisson(![]() ). Then,

). Then,

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Thus, the conditional log-likelihood function of the fixed effects Poisson model is given by

The gradient is

|

|

|

|

|

|

|

|

where

In the Poisson random effects model, conditional on ![]() and parameter

and parameter ![]() ,

, ![]() is iid Poisson distributed with parameter

is iid Poisson distributed with parameter ![]() , and the individual effects,

, and the individual effects, ![]() , are assumed to be iid random variables. The joint density for observations in all time periods for the

, are assumed to be iid random variables. The joint density for observations in all time periods for the ![]() th individual,

th individual, ![]() , can be obtained after the density

, can be obtained after the density ![]() of

of ![]() is specified.

is specified.

Let

so that ![]() and

and ![]() :

:

Let ![]() . Since

. Since ![]() is conditional on

is conditional on ![]() and parameter

and parameter ![]() is iid Poisson(

is iid Poisson(![]() ), the conditional joint probability for observations in all time periods for the

), the conditional joint probability for observations in all time periods for the ![]() th individual,

th individual, ![]() , is the product of

, is the product of ![]() Poisson densities:

Poisson densities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Then, the joint density for the ![]() th panel conditional on just the

th panel conditional on just the ![]() can be obtained by integrating out

can be obtained by integrating out ![]() :

:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

where ![]() is the overdispersion parameter. This is the density of the Poisson random effects model with gamma-distributed random effects.

For this distribution,

is the overdispersion parameter. This is the density of the Poisson random effects model with gamma-distributed random effects.

For this distribution, ![]() and

and ![]() ; that is, there is overdispersion.

; that is, there is overdispersion.

Then the log-likelihood function is written as

|

|

|

|

|

|

|

|

|

|

|

|

The gradient is

|

|

|

|

|

|

|

|

|

|

|

|

and

|

|

|

|

|

|

|

|

where ![]() ,

, ![]() and

and ![]() is the digamma function.

is the digamma function.

This section shows the derivation of a negative binomial model with fixed effects. Keep the assumptions of the Poisson-distributed dependent variable

But now let the Poisson parameter be random with gamma distribution and parameters ![]() ,

,

where one of the parameters is the exponentially affine function of independent variables ![]() . Use integration by parts to obtain the distribution of

. Use integration by parts to obtain the distribution of ![]() ,

,

|

|

|

|

|

|

|

|

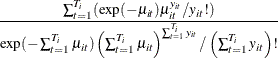

which is a negative binomial distribution with parameters ![]() . Conditional joint distribution is given as

. Conditional joint distribution is given as

|

|

|

|

|

|

|

|

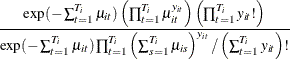

Hence, the conditional fixed-effects negative binomial log-likelihood is

|

|

|

|

|

|

|

|

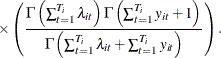

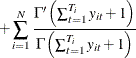

The gradient is

|

|

|

![$\displaystyle \sum _{i=1}^{N}\left[\left(\frac{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}\right)}{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}\right)}-\frac{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right)\sum _{t=1}^{T_{i}}\lambda _{it}\mathbf{x}_{it}\right] $](images/etsug_tcountreg0341.png) |

|

|

|

|

|

|

|

|

This section describes the derivation of negative binomial model with random effects. Suppose

with the Poisson parameter distributed as gamma,

where its parameters are also random:

Assume that the distribution of a function of ![]() is beta with parameters

is beta with parameters ![]() :

:

Explicitly, the beta density with ![]() domain is

domain is

where ![]() is the beta function. Then, conditional joint distribution of dependent variables is

is the beta function. Then, conditional joint distribution of dependent variables is

Integrating out the variable ![]() yields the following conditional distribution function:

yields the following conditional distribution function:

|

|

|

|

|

|

|

|

|

|

|

|

Consequently, the conditional log-likelihood function for a negative binomial model with random effects is

|

|

|

|

|

|

|

|

|

|

|

|

The gradient is

|

|

|

![$\displaystyle \sum _{i=1}^{N}\left[\frac{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}\sum _{t=1}^{T_{i}}\lambda _{it}\mathbf{x}_{it}+\frac{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}\right] $](images/etsug_tcountreg0362.png) |

|

|

|

![$\displaystyle -\sum _{i=1}^{N}\left[\frac{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\sum _{t=1}^{T_{i}}\lambda _{it}\mathbf{x}_{it}\right] $](images/etsug_tcountreg0363.png) |

|

|

|

|

and

|

|

|

![$\displaystyle \sum _{i=1}^{N}\left[\frac{\Gamma \left(a+b\right)}{\Gamma \left(a+b\right)}+\frac{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}{\Gamma \left(a+\sum _{t=1}^{T_{i}}\lambda _{it}\right)}\right] $](images/etsug_tcountreg0367.png) |

|

|

|

![$\displaystyle -\sum _{i=1}^{N}\left[\frac{\Gamma \left(a\right)}{\Gamma \left(a\right)}+\frac{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right], $](images/etsug_tcountreg0368.png) |

and

|

|

|

![$\displaystyle \sum _{i=1}^{N}\left[\frac{\Gamma \left(a+b\right)}{\Gamma \left(a+b\right)}+\frac{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(b+\sum _{t=1}^{T_{i}}y_{it}\right)}\right] $](images/etsug_tcountreg0371.png) |

|

|

|

![$\displaystyle -\sum _{i=1}^{N}\left[\frac{\Gamma \left(b\right)}{\Gamma \left(b\right)}+\frac{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}{\Gamma \left(a+b+\sum _{t=1}^{T_{i}}\lambda _{it}+\sum _{t=1}^{T_{i}}y_{it}\right)}\right]. $](images/etsug_tcountreg0372.png) |