| The AUTOREG Procedure |

| Testing |

Heteroscedasticity and Normality Tests

Portmanteau Q Test

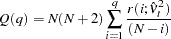

For nonlinear time series models, the portmanteau test statistic based on squared residuals is used to test for independence of the series (McLeod and Li; 1983):

|

where

|

|

This Q statistic is used to test the nonlinear effects (for example, GARCH effects) present in the residuals. The GARCH process can be considered as an ARMA

process can be considered as an ARMA process. See the section Predicting the Conditional Variance later in this chapter. Therefore, the Q statistic calculated from the squared residuals can be used to identify the order of the GARCH process.

process. See the section Predicting the Conditional Variance later in this chapter. Therefore, the Q statistic calculated from the squared residuals can be used to identify the order of the GARCH process.

Lagrange Multiplier Test for ARCH Disturbances

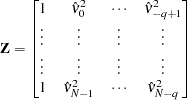

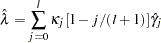

Engle (1982) proposed a Lagrange multiplier test for ARCH disturbances. The test statistic is asymptotically equivalent to the test used by Breusch and Pagan (1979). Engle’s Lagrange multiplier test for the qth order ARCH process is written

|

where

|

and

|

The presample values (  ,

, ,

,  ) have been set to 0. Note that the LM

) have been set to 0. Note that the LM tests may have different finite-sample properties depending on the presample values, though they are asymptotically equivalent regardless of the presample values. The LM and Q statistics are computed from the OLS residuals assuming that disturbances are white noise. The Q and LM statistics have an approximate

tests may have different finite-sample properties depending on the presample values, though they are asymptotically equivalent regardless of the presample values. The LM and Q statistics are computed from the OLS residuals assuming that disturbances are white noise. The Q and LM statistics have an approximate  distribution under the white-noise null hypothesis.

distribution under the white-noise null hypothesis.

Normality Test

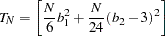

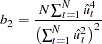

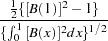

Based on skewness and kurtosis, Jarque and Bera (1980) calculated the test statistic

|

where

|

|

The

(2) distribution gives an approximation to the normality test

(2) distribution gives an approximation to the normality test  .

.

When the GARCH model is estimated, the normality test is obtained using the standardized residuals  . The normality test can be used to detect misspecification of the family of ARCH models.

. The normality test can be used to detect misspecification of the family of ARCH models.

Computation of the Chow Test

Consider the linear regression model

|

where the parameter vector  contains

contains  elements.

elements.

Split the observations for this model into two subsets at the break point specified by the CHOW= option, so that

|

|

|

|||

|

|

|

|||

|

|

|

Now consider the two linear regressions for the two subsets of the data modeled separately,

|

|

where the number of observations from the first set is  and the number of observations from the second set is

and the number of observations from the second set is  .

.

The Chow test statistic is used to test the null hypothesis  conditional on the same error variance

conditional on the same error variance  . The Chow test is computed using three sums of square errors:

. The Chow test is computed using three sums of square errors:

|

where  is the regression residual vector from the full set model,

is the regression residual vector from the full set model,  is the regression residual vector from the first set model, and

is the regression residual vector from the first set model, and  is the regression residual vector from the second set model. Under the null hypothesis, the Chow test statistic has an F distribution with

is the regression residual vector from the second set model. Under the null hypothesis, the Chow test statistic has an F distribution with  and

and  degrees of freedom, where is the number of elements in

degrees of freedom, where is the number of elements in  .

.

Chow (1960) suggested another test statistic that tests the hypothesis that the mean of prediction errors is 0. The predictive Chow test can also be used when  .

.

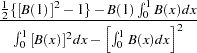

The PCHOW= option computes the predictive Chow test statistic

|

The predictive Chow test has an F distribution with and  degrees of freedom.

degrees of freedom.

Phillips-Perron Unit Root and Cointegration Testing

Consider the random walk process

|

where the disturbances might be serially correlated with possible heteroscedasticity. Phillips and Perron (1988) proposed the unit root test of the OLS regression model,

|

Let  and let

and let  be the variance estimate of the OLS estimator

be the variance estimate of the OLS estimator  , where

, where  is the OLS residual. You can estimate the asymptotic variance of

is the OLS residual. You can estimate the asymptotic variance of  by using the truncation lag l.

by using the truncation lag l.

|

where  ,

,  for

for  , and

, and  .

.

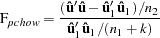

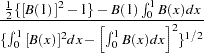

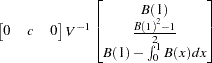

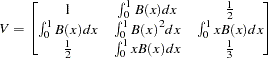

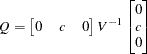

Then the Phillips-Perron  (defined here as

(defined here as  ) test (zero mean case) is written

) test (zero mean case) is written

|

and has the following limiting distribution:

|

where B( ) is a standard Brownian motion. Note that the realization

) is a standard Brownian motion. Note that the realization  from the stochastic process

from the stochastic process  is distributed as

is distributed as  and thus

and thus  .

.

Note that  as

as  , which shows that the limiting distribution is skewed to the left.

, which shows that the limiting distribution is skewed to the left.

Let  be the

be the  statistic for . The Phillips-Perron

statistic for . The Phillips-Perron  (defined here as

(defined here as  ) test is written

) test is written

|

and its limiting distribution is derived as

|

When you test the regression model  for the true random walk process (single mean case), the limiting distribution of the statistic

for the true random walk process (single mean case), the limiting distribution of the statistic  is written

is written

|

while the limiting distribution of the statistic is given by

|

Finally, the limiting distribution of the Phillips-Perron test for the random walk with drift process  (trend case) can be derived as

(trend case) can be derived as

|

where  for

for  and

and  for ,

for ,

|

|

When several variables  are cointegrated, there exists a

are cointegrated, there exists a  cointegrating vector

cointegrating vector  such that

such that  is stationary and is a nonzero vector. The residual based cointegration test assumes the following regression model:

is stationary and is a nonzero vector. The residual based cointegration test assumes the following regression model:

|

where  ,

,  , and = (

, and = ( ,

, ,

, . You can estimate the consistent cointegrating vector by using OLS if all variables are difference stationary — that is, I(1). The Phillips-Ouliaris test is computed using the OLS residuals from the preceding regression model, and it performs the test for the null hypothesis of no cointegration. The estimated cointegrating vector is

. You can estimate the consistent cointegrating vector by using OLS if all variables are difference stationary — that is, I(1). The Phillips-Ouliaris test is computed using the OLS residuals from the preceding regression model, and it performs the test for the null hypothesis of no cointegration. The estimated cointegrating vector is  .

.

You need to refer to the tables by Phillips and Ouliaris (1990) to obtain the  -value of the cointegration test. Before you apply the cointegration test, you may want to perform the unit root test for each variable (see the option STATIONARITY= ( PHILLIPS )).

-value of the cointegration test. Before you apply the cointegration test, you may want to perform the unit root test for each variable (see the option STATIONARITY= ( PHILLIPS )).

Kwiatkowski, Phillips, Schmidt, and Shin (KPSS) Unit Root Test

The KPSS test was introduced in Kwiatkowski et al. (1992) to test the null hypothesis that an observable series is stationary around a deterministic trend. Please note, that for consistency reasons, the notation used here is different from the notation used in the original paper. The setup of the problem is as follows: it is assumed that the series is expressed as the sum of the deterministic trend, random walk  , and stationary error

, and stationary error  ; that is,

; that is,

|

with  ,

,  iid

iid  , and an intercept

, and an intercept  (in the original paper, the authors use

(in the original paper, the authors use  instead of .) Under stronger assumptions of normality and iid of and

instead of .) Under stronger assumptions of normality and iid of and  , a one-sided LM test of the null that there is no random walk (

, a one-sided LM test of the null that there is no random walk ( ) can be constructed as follows:

) can be constructed as follows:

|

|

|||

|

|

|||

|

|

Following the original work of Kwiatkowski, Phillips, Schmidt, and Shin, under the null ( ),

),  statistic converges asymptotically to three different distributions depending on whether the model is trend-stationary, level-stationary (

statistic converges asymptotically to three different distributions depending on whether the model is trend-stationary, level-stationary ( ), or zero-mean stationary (,

), or zero-mean stationary (,  ). The trend-stationary model is denoted by subscript and the level-stationary model is denoted by subscript . The case when there is no trend and zero intercept denoted as 0. The last case is considered in Hobijn, Franses, and Ooms (2004).

). The trend-stationary model is denoted by subscript and the level-stationary model is denoted by subscript . The case when there is no trend and zero intercept denoted as 0. The last case is considered in Hobijn, Franses, and Ooms (2004).

|

|

|||

|

|

|||

|

|

|||

|

|

|||

|

|

where  is a standard Brownian bridge,

is a standard Brownian bridge,  is a Brownian bridge of a second-level,

is a Brownian bridge of a second-level,  is a Brownian motion (Wiener process), and

is a Brownian motion (Wiener process), and  is convergence in distribution.

is convergence in distribution.

Using the notation of Kwiatkowski et al. (1992) the  statistic is named as

statistic is named as  . This test depends on the computational method used to compute the long-run variance

. This test depends on the computational method used to compute the long-run variance  — that is, the window width

— that is, the window width  and the kernel type

and the kernel type  . You can specify the kernel used in the test, using the KERNEL option:

. You can specify the kernel used in the test, using the KERNEL option:

Newey-West/Bartlett (KERNEL=NW

BART), default

BART), default

Quadratic spectral (KERNEL=QS)

You can specify the number of lags, , in three different ways:

Schwert (SCHW = c) (default for NW, c=4)

Manual (LAG =

) Automatic selection (AUTO) (default for QS) Hobijn, Franses, and Ooms (2004)

The last option (AUTO) needs more explanation, summarized in the following table.

NW Kernel |

QS Kernel |

||

|---|---|---|---|

|

|

||

where |

|||

|

|

||

|

|||

|

|

||

– number of observations,

– number of observations,

|

|||

|

Ramsey’s Reset Test

Ramsey’s reset test is a misspecification test associated with the functional form of models to check whether power transforms need to be added to a model. The original linear model, henceforth called the restricted model, is

|

To test for misspecification in the functional form, the unrestricted model is

|

where  is the predicted value from the linear model and is the power of in the unrestricted model equation starting from 2. The number of higher-ordered terms to be chosen depends on the discretion of the analyst. The RESET opti

is the predicted value from the linear model and is the power of in the unrestricted model equation starting from 2. The number of higher-ordered terms to be chosen depends on the discretion of the analyst. The RESET opti

on produces test results for  2, 3, and 4.

2, 3, and 4.

The reset test is an F statistic for testing  , against

, against  for at least one

for at least one  in the unrestricted model and is computed as follows:

in the unrestricted model and is computed as follows:

|

where  is the sum of squared errors due to the restricted model,

is the sum of squared errors due to the restricted model,  is the sum of squared errors due to the unrestricted model,

is the sum of squared errors due to the unrestricted model,  is the total number of observations, and is the number of parameters in the original linear model.

is the total number of observations, and is the number of parameters in the original linear model.

Ramsey’s test can be viewed as a linearity test that checks whether any nonlinear transformation of the specified independent variables has been omitted, but it need not help in identifying a new relevant variable other than those already specified in the current model.

Copyright © 2008 by SAS Institute Inc., Cary, NC, USA. All rights reserved.