| The TCALIS Procedure |

Example 88.10 A Multiple-Group Model for Purchasing Behavior

In this example, data were collected from customers who made purchases from a retail company during years 2002 and 2003. A two-group structural equation model is fitted to the data.

The variables are:

- Spend02:

total purchase amount in 2002

- Spend03:

total purchase amount in 2003

- Courtesy:

rating of the courtesy of the customer service

- Responsive:

rating of the responsiveness of the customer service

- Helpful:

rating of the helpfulness of the customer service

- Delivery:

rating of the timeliness of the delivery

- Pricing:

rating of the product pricing

- Availability:

rating of the product availability

- Quality:

rating of the product quality

For the ratings scales, nine-point scales were used. Customers could respond 1 to 9 on these scales, with 1 representing "extremely unsatisfied" and 9 representing "extremely satisfied." Data were collected from two different regions, which will be labeled as Region 1 ( ) and Region 2 (

) and Region 2 ( ), respectively. The ratings were collected at the end of year 2002 so that they represent customers’ purchasing experience in year 2002.

), respectively. The ratings were collected at the end of year 2002 so that they represent customers’ purchasing experience in year 2002.

The central questions of the study are:

How does the overall customer service affect the current purchases and predict future purchases?

How does the overall product quality affect the current purchases and predict future purchases?

Do current purchases predict future purchases?

Do the two regions have different structural models for predicting the purchases?

In stating these research questions, you use several constructs that might or might not correspond to objective measurements. Current and future purchases are certainly measurable directly by the spending of the customers. That is, because customer service and product satisfaction/qualities were surveyed between 2002 and 2003, Spend02 would represent current purchases and Spend03 would represent future purchases in the study. Both variables Spend02 and Spend03 are objective measurements without measurement errors. All you need to do is to extract the information from the transaction records. But how about hypothetical constructs like customer service quality and product quality? How would you measure them in the model?

In measuring these hypothetical constructs, one might ask customers’ perception about the service or product quality directly in a single question. A simple survey with two questions about the customer service and product qualities could then be what you need. These questions are called indicators (or indicator variables) of the underlying constructs. However, using just one indicator (question) for each of these hypothetical constructs would be quite unreliable—that is, measurement errors might dominate in the data collection process. Therefore, multiple indicators are usually recommended for measuring such hypothetical constructs.

There are two main advantages of using multiple indicators for hypothetical constructs. The first one is conceptual and the other is statistical/mathematical.

First, hypothetical constructs might conceptually be multifaceted themselves. Measuring a hypothetical construct by a single indicator does not capture the full meaning of the construct. For example, the product quality might refer to the durability of the product, the outlook of the product, the pricing of the product, and the availability of product, among others. The customer service quality might refer to the politeness of the customer service, the timeliness of the delivery, and the responsiveness of customer services, among others. Therefore, multiple indicators for a single hypothetical construct might be necessary if you want to cover the multifaceted aspects of a given hypothetical construct.

Second, from a statistical point of view, the reliability would be higher if you combine correlated indicators for a construct than if you use a single indicator only. Therefore, combining correlated indicators would lead to more accurate and reliable results.

One way to combine correlated indicators is to use a simple sum of them to represent the underlying hypothetical construct. However, a better way is to use the structural equation modeling technique that represents each indicator (variable) as a function of the underlying hypothetical construct plus an error term. In structural equation modeling, hypothetical constructs are constructed as latent factors, which are unobserved systematic (that is, non-error) variables. Theoretically, latent factors are free from measurement errors, and so the estimation through the structural equation modeling technique is more accurate than if you just use simple sums of indicators to represent hypothetical constructs. Therefore, structural equation modeling approach is the method of the choice in the current analysis.

In practice, you must also make sure that there are enough indicators for the identification of the underlying latent factor, and hence the identification of the entire model. Necessary and sufficient rules for identification are very complicated to describe and are out of the scope of the current discussion (however, see Bollen 1989b for discussions of identification rules for various classes of structural equation models). Some simple rules of thumb may be useful as a guidance. For example, for unconstrained situations, you should at least have three indicators (variables) measured for a latent factor. Unfortunately, these rules of thumb do not guarantee identification in every case.

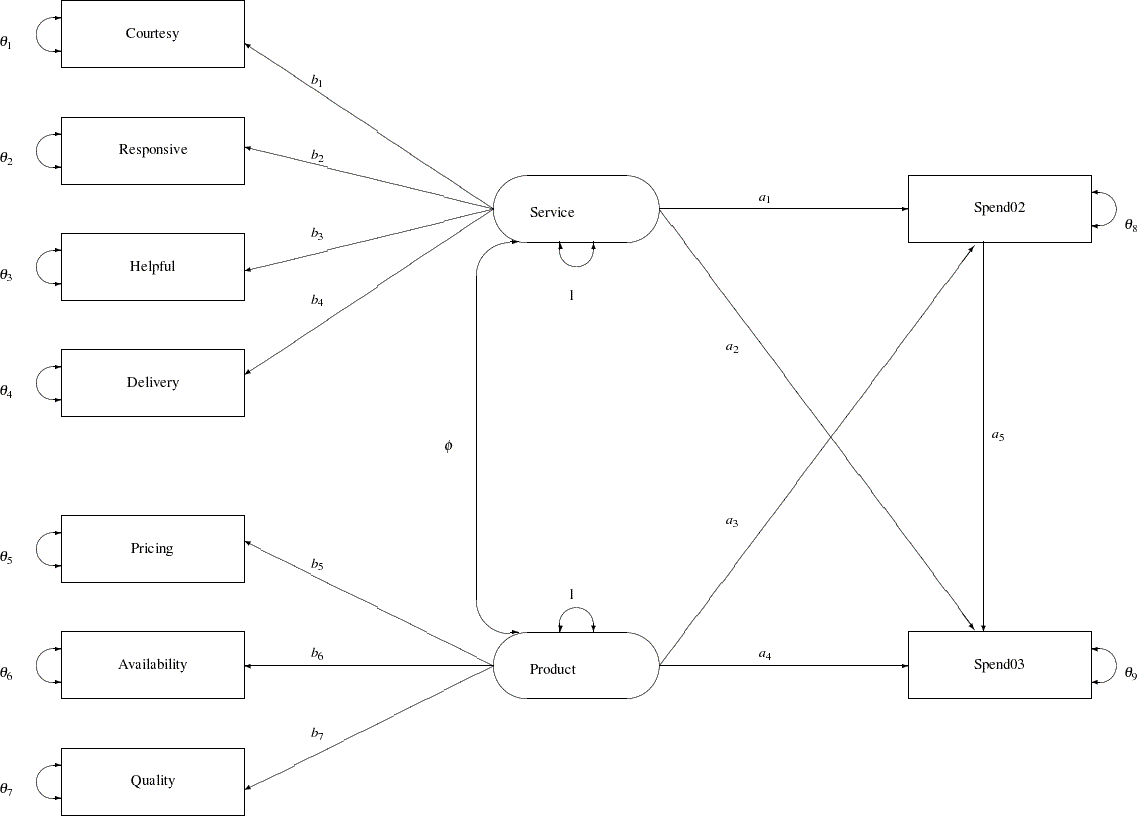

In this example, Service and Product are latent factors in the structural equation model that represents service and product qualities, respectively. In the model, these two latent factors are reflected by the ratings of the customers. Ratings on the Courtesy, Responsive, Helpful, and Delivery scales are indicators of Service. Ratings on the Pricing, Availability, and Quality scales are indicators of Product (that is, product quality).

A Path Diagram

A path diagram is used to represent the structural equation model for the purchase behavior. In Figure 88.5, observed or manifest variables are represented by rectangles, and latent variables are represented by ovals. As mentioned, two latent variables or factors, Service and Product are created as overall measures of customer service and product qualities, respectively.

The left part of the diagram represents the measurement model of the latent variables. The Service factor has four indicators: Courtesy, Responsive, Helpful, and Delivery. The path coefficients to these observed variables from the Service factor are  ,

,  ,

,  , and

, and  , respectively. Similarly, the Product variable has three indicators: Pricing, Availability, and Quality, with path coefficients

, respectively. Similarly, the Product variable has three indicators: Pricing, Availability, and Quality, with path coefficients  ,

,  , and

, and  , respectively.

, respectively.

The two latent factors are predictors of the purchase amounts Spend02 and Spend03. In addition, Spend02 also serves as a predictor of Spend03. Path coefficients or effects for this part of functional relationships are represented by a1–a5 in the diagram.

Each variable in the path diagram has a variance parameter. For endogenous or dependent variables, which serve as outcome variables in the model, the variance parameters are the error variances that are not accounted for by the predictors. For example, in the current model all observed variables are endogenous variables. The double-headed arrows tagged on these variables represent error variances. In the diagram,  to

to  are the names of these error variance parameters. For exogenous or independent variables, which never serve as outcome variables in the model, the variance parameters are the (total) variances of these variables. For example, in the diagram the double-headed arrows tagged on Service and Product represent the variances of these two latent variables. In the current model, both of these variances are fixed at one.

are the names of these error variance parameters. For exogenous or independent variables, which never serve as outcome variables in the model, the variance parameters are the (total) variances of these variables. For example, in the diagram the double-headed arrows tagged on Service and Product represent the variances of these two latent variables. In the current model, both of these variances are fixed at one.

When the double-headed arrows are pointing to two variables, they represent covariances in the path diagram. For example, in Figure 88.5 the covariance between Service and Product is represented by the parameter  .

.

A Macro for the Basic Path Model

For the moment, it is hypothesized that both Region 1 and Region 2 data are fitted by the same model as shown in Figure 88.5. Once the path diagram is drawn, it is readily translated into the PATH modeling language. See the PATH statement for details about how to use the PATH modeling language to specify structural equation models. A macro for the path model in Figure 88.5 using the PATH modeling language is shown in the following:

%macro BasepathModel;

path

Service -> Spend02 a1,

Service -> Spend03 a2,

Product -> Spend02 a3,

Product -> Spend03 a4,

Spend02 -> Spend03 a5,

Service -> Courtesy b1,

Service -> Responsive b2,

Service -> Helpful b3,

Service -> Delivery b4,

Product -> Pricing b5,

Product -> Availability b6,

Product -> Quality b7;

pvar

Courtesy Responsive Helpful

Delivery Pricing

Availability Quality = theta01-theta07,

Spend02 = theta08,

Spend03 = theta09,

Service Product = 2 * 1.;

pcov

Service Product = phi;

mean

Service Product = 2 * 0.,

Spend02 = InterSpend02,

Spend03 = InterSpend03,

Courtesy Responsive Helpful

Delivery Pricing

Availability Quality = intercept01-intercept07;

%mend;

The name of this macro is BasePathModel. Defining a model by a SAS macro is not essential to run PROC TCALIS. You could have inserted the PATH model code directly into a PROC TCALIS run. The reason for using a macro here is to facilitate the presentation of the subsequent code so that the coding structure is made clearer. In the BasePathModel macro, the PATH statement captures all the path coefficient specification as well as the direction of the paths in the model. The first five paths are for defining how Spend02 and Spend03 are predicted from the latent variables Service, Product, and Spend02. The next seven paths are for defining the measurement model.

The PVAR statement captures the specification of the error variances and the variances of exogenous variables. The PCOV statement captures the specification of covariance between the two latent variables in the model.

The MEAN statement captures the specification of means and intercepts. Unlike some other representation schemes proposed by various researchers in the field, the mean parameters are not depicted in Figure 88.5. The reason is that representing the mean and intercept parameters in the path diagram would usually obscure the "causal" paths, which are of primary interest. In addition, it is a simple matter to specify the mean and intercept parameters in the MEAN statement without the help of a path diagram when you follow these principles:

Each variable in the path diagram has a mean parameter that can be specified in the MEAN statement.

For exogenous variables, the specifications in the MEAN statement are for the means of these variables.

For endogenous variables, the specifications in the MEAN statement are for the intercepts of these variables.

For variables that are not specified in the MEAN statement, their means or intercepts are fixed zeros by default.

The total number of mean parameters should not exceed the number of observed variables.

Because all nine observed variables are endogenous in the model, their specification in the MEAN statement are for nine intercepts: intercept01–intercept07, InterSpend02, and InterSpend03. The means of the latent variables Service and Product are also specified in the MEAN statement as fixed zeros.

A Restrictive Model with Invariant Mean and Covariance Structures

The following shows the SAS data set being analyzed and the PROC TCALIS specification of a restrictive mean and covariance structure model:

data region1(type=cov);

input _type_ $6. _name_ $12. Spend02 Spend03 Courtesy Responsive

Helpful Delivery Pricing Availability Quality;

datalines;

COV Spend02 14.428 2.206 0.439 0.520 0.459 0.498 0.635 0.642 0.769

COV Spend03 2.206 14.178 0.540 0.665 0.560 0.622 0.535 0.588 0.715

COV Courtesy 0.439 0.540 1.642 0.541 0.473 0.506 0.109 0.120 0.126

COV Responsive 0.520 0.665 0.541 2.977 0.582 0.629 0.119 0.253 0.184

COV Helpful 0.459 0.560 0.473 0.582 2.801 0.546 0.113 0.121 0.139

COV Delivery 0.498 0.622 0.506 0.629 0.546 3.830 0.120 0.132 0.145

COV Pricing 0.635 0.535 0.109 0.119 0.113 0.120 2.152 0.491 0.538

COV Availability 0.642 0.588 0.120 0.253 0.121 0.132 0.491 2.372 0.589

COV Quality 0.769 0.715 0.126 0.184 0.139 0.145 0.538 0.589 2.753

MEAN . 183.500 301.921 4.312 4.724 3.921 4.357 6.144 4.994 5.971

;

data region2(type=cov);

input _type_ $6. _name_ $12. Spend02 Spend03 Courtesy Responsive

Helpful Delivery Pricing Availability Quality;

datalines;

COV Spend02 14.489 2.193 0.442 0.541 0.469 0.508 0.637 0.675 0.769

COV Spend03 2.193 14.168 0.542 0.663 0.574 0.623 0.607 0.642 0.732

COV Courtesy 0.442 0.542 3.282 0.883 0.477 0.120 0.248 0.283 0.387

COV Responsive 0.541 0.663 0.883 2.717 0.477 0.601 0.421 0.104 0.105

COV Helpful 0.469 0.574 0.477 0.477 2.018 0.507 0.187 0.162 0.205

COV Delivery 0.508 0.623 0.120 0.601 0.507 2.999 0.179 0.334 0.099

COV Pricing 0.637 0.607 0.248 0.421 0.187 0.179 2.512 0.477 0.423

COV Availability 0.675 0.642 0.283 0.104 0.162 0.334 0.477 2.085 0.675

COV Quality 0.769 0.732 0.387 0.105 0.205 0.099 0.423 0.675 2.698

MEAN . 156.250 313.670 2.412 2.727 5.224 6.376 7.147 3.233 5.119

;

proc tcalis maxiter=1000 omethod=nrr;

group 1 / data=region1 label="Region 1" nobs=378;

group 2 / data=region2 label="Region 2" nobs=423;

model 1 / group=1,2;

%BasepathModel

run;

In the PROC TCALIS specification, you use the GROUP statements to specify the data for the two regions. Using the DATA= options in the GROUP statements, you assign the Region 1 data to group 1 and the Region 2 data to group 2. You label the two groups by the LABEL= options. Because the number of observations are not defined in the data sets, you use the NOBS= options in the GROUP statements to provide this information.

In the MODEL statement, you specify in the GROUP= option that both Groups 1 and 2 are fitted by the same model—model 1. Next, the BasePathModel macro is included for defining the model for the two groups. Equivalently, you can use two MODEL statements to define two models for the two groups. This way you must also constrain each parameter in the two models. But using a single MODEL statement for the two groups is a short cut for defining such a restrictive model with total parameter invariance among groups.

The OMETHOD=NRR (Newton-Raphson ridge optimization) is used because the default Levenberg-Marquardt optimization did not converge in 1000 iterations.

In Output 88.10.1, a summary of modeling information is presented. Each group is listed with its associated data set, number of observations, and its corresponding model and the model type. In the current analysis, the same model is fitted to both groups. Next, a table for the types of variables is presented. As intended, all nine observed (manifest) variables are endogenous and all latent variables are exogenous in the model.

The optimization converges in 201 iterations. The fit summary table is presented in Output 88.10.2.

| Fit Summary | ||

|---|---|---|

| Modeling Info | N Observations | 801 |

| N Variables | 9 | |

| N Moments | 108 | |

| N Parameters | 31 | |

| N Active Constraints | 0 | |

| Independence Model Chi-Square | 399.7468 | |

| Independence Model Chi-Square DF | 72 | |

| Absolute Index | Fit Function | 3.5310 |

| Chi-Square | 2821.2798 | |

| Chi-Square DF | 77 | |

| Pr > Chi-Square | 0.0000 | |

| Z-Test of Wilson & Hilferty | 43.2651 | |

| Hoelter Critical N | 29 | |

| Root Mean Square Residual (RMSR) | 28.2211 | |

| Standardized RMSR (SRMSR) | 2.1370 | |

| Goodness of Fit Index (GFI) | 0.9996 | |

| Parsimony Index | Adjusted GFI (AGFI) | 0.9995 |

| Parsimonious GFI | 1.0690 | |

| RMSEA Estimate | 0.2987 | |

| RMSEA Lower 90% Confidence Limit | 0.2893 | |

| RMSEA Upper 90% Confidence Limit | 0.3082 | |

| Probability of Close Fit | . | |

| Akaike Information Criterion | 2667.2798 | |

| Bozdogan CAIC | 2229.4685 | |

| Schwarz Bayesian Criterion | 2306.4685 | |

| McDonald Centrality | 0.1803 | |

| Incremental Index | Bentler Comparative Fit Index | -7.3732 |

| Bentler-Bonett NFI | -6.0577 | |

| Bentler-Bonett Non-normed Index | -6.8295 | |

| Bollen Normed Index Rho1 | -5.5994 | |

| Bollen Non-normed Index Delta2 | -7.5029 | |

| James et al. Parsimonious NFI | -6.4783 | |

The model chi-square statistic is  . With

. With  =77 and

=77 and  , the null hypothesis for the mean and covariance structures is rejected. All incremental fit indices are negative. These negative indices indicate a bad model fit, as compared with the independence model. The same fact can be deduced by comparing the chi-square values of the independence model and the structural model defined. The independence model has five degrees of freedom less (five parameters more) than the structural model but the chi-square value is only

, the null hypothesis for the mean and covariance structures is rejected. All incremental fit indices are negative. These negative indices indicate a bad model fit, as compared with the independence model. The same fact can be deduced by comparing the chi-square values of the independence model and the structural model defined. The independence model has five degrees of freedom less (five parameters more) than the structural model but the chi-square value is only  , much less than the model fit chi-square value of

, much less than the model fit chi-square value of  . Because variables in social and behavioral sciences are almost always expected to correlate with each other, a structural model that explains relationships even worse than the independence model is deemed inappropriate for the data. The RMSEA for the structural model is

. Because variables in social and behavioral sciences are almost always expected to correlate with each other, a structural model that explains relationships even worse than the independence model is deemed inappropriate for the data. The RMSEA for the structural model is  , which also indicates a bad model fit. However, GFI, AGFI, and Parsimonious GFI indicate good model fit, which is a little surprising given the fact that all other indices indicate the opposite and the overall model is pretty restrictive in the first place.

, which also indicates a bad model fit. However, GFI, AGFI, and Parsimonious GFI indicate good model fit, which is a little surprising given the fact that all other indices indicate the opposite and the overall model is pretty restrictive in the first place.

There is a warning in the output:

WARNING: Model 1. Although all predicted variances for the

latent variables are positive, the corresponding

predicted covariance matrix is not positive definite.

It has one negative eigenvalue.

PROC TCALIS routinely checks the properties of the predicted covariance matrix. It will issue warnings when there are problems. In this case, the predicted covariance matrix for the latent variables is not positive definite and has one negative eigenvalue. The same fact can also be deduced from the output:

In Output 88.10.3, the covariance between Service and Product is estimated at  . Recall that the variances of these two variables are fixed at ones. Therefore, the predicted covariance matrix for the latent variables is:

. Recall that the variances of these two variables are fixed at ones. Therefore, the predicted covariance matrix for the latent variables is:

|

This matrix is certainly not a proper covariance matrix, as the covariance is larger in magnitude than the variances. The eigenvalues for this matrix are  and

and  , indicating a negative definite covariance matrix for the latent variables.

, indicating a negative definite covariance matrix for the latent variables.

A Model with Unconstrained Parameters for the Two Regions

With all the bad model fit indications and the problematic predicted covariance matrix for the latent variables, you might conclude that an overly restricted model has been fit. Region 1 and Region 2 might not share exactly the same set of parameters. How about fitting a model at the other extreme with all parameters unconstrained for the two groups (regions)? Such a model can be easily specified, as shown in the following statements.

proc tcalis omethod=nrr;

group 1 / data=region1 label="Region 1" nobs=378;

group 2 / data=region2 label="Region 2" nobs=423;

model 1 / groups=1;

%BasepathModel

model 2 / groups=2;

refmodel 1/ AllNewParms;

run;

Unlike the previous specification, in the current specification group 2 is now fitted by a new model labeled as model 2. This model is based on model 1, as specified in REFMODEL statement. The ALLNEWPARMS option in the REFMODEL statement request that all parameters specified in model 1 be renamed so that they become new parameters. As a result, this specification gives different sets of estimates for model 1 and model 2, although both models have the same path structures and a comparable set of parameters.

The optimization converges in 10 iterations without problems. The fit summary table is displayed in Output 88.10.4. The chi-square statistic is  (df

(df ,

,  ). The theoretical model is not rejected. Many other measures of fit also indicate very good model fit. For example, GFI, AGFI, Bentler CFI, Bentler-Bonett NFI, Bollen non-normed index delta2 are all close to one, and RMSEA is close to zero.

). The theoretical model is not rejected. Many other measures of fit also indicate very good model fit. For example, GFI, AGFI, Bentler CFI, Bentler-Bonett NFI, Bollen non-normed index delta2 are all close to one, and RMSEA is close to zero.

| Fit Summary | ||

|---|---|---|

| Modeling Info | N Observations | 801 |

| N Variables | 9 | |

| N Moments | 108 | |

| N Parameters | 62 | |

| N Active Constraints | 0 | |

| Independence Model Chi-Square | 399.7468 | |

| Independence Model Chi-Square DF | 72 | |

| Absolute Index | Fit Function | 0.0371 |

| Chi-Square | 29.6131 | |

| Chi-Square DF | 46 | |

| Pr > Chi-Square | 0.9710 | |

| Z-Test of Wilson & Hilferty | -1.8950 | |

| Hoelter Critical N | 1697 | |

| Root Mean Square Residual (RMSR) | 0.0670 | |

| Standardized RMSR (SRMSR) | 0.0220 | |

| Goodness of Fit Index (GFI) | 1.0000 | |

| Parsimony Index | Adjusted GFI (AGFI) | 1.0000 |

| Parsimonious GFI | 0.6389 | |

| RMSEA Estimate | 0.0000 | |

| RMSEA Lower 90% Confidence Limit | . | |

| RMSEA Upper 90% Confidence Limit | . | |

| Probability of Close Fit | 1.0000 | |

| Akaike Information Criterion | -62.3869 | |

| Bozdogan CAIC | -323.9365 | |

| Schwarz Bayesian Criterion | -277.9365 | |

| McDonald Centrality | 1.0103 | |

| Incremental Index | Bentler Comparative Fit Index | 1.0000 |

| Bentler-Bonett NFI | 0.9259 | |

| Bentler-Bonett Non-normed Index | 1.0783 | |

| Bollen Normed Index Rho1 | 0.8840 | |

| Bollen Non-normed Index Delta2 | 1.0463 | |

| James et al. Parsimonious NFI | 0.5916 | |

Notice that because there are no constraints between the two models for the groups, you might have fit the two sets of data by the respective models separately and gotten exactly the same results as in the current analysis. For example, you get two model fit chi-square values from separate analyses. Adding up these two chi-squares will give you the same overall chi-square as in Output 88.10.4.

PROC TCALIS also provides a table for comparing relative model fit of the groups. In Output 88.10.5, basic modeling information and some measures of fit for the two groups are shown along with the corresponding overall measures.

| Fit Comparison Among Groups | ||||

|---|---|---|---|---|

| Overall | Region 1 | Region 2 | ||

| Modeling Info | N Observations | 801 | 378 | 423 |

| N Variables | 9 | 9 | 9 | |

| N Moments | 108 | 54 | 54 | |

| N Parameters | 62 | 31 | 31 | |

| N Active Constraints | 0 | 0 | 0 | |

| Independence Model Chi-Square | 399.7468 | 173.4482 | 226.2986 | |

| Independence Model Chi-Square DF | 72 | 36 | 36 | |

| Fit Index | Fit Function | 0.0371 | 0.0023 | 0.0681 |

| Percent Contribution to Chi-Square | 100 | 3 | 97 | |

| Root Mean Square Residual (RMSR) | 0.0670 | 0.0172 | 0.0907 | |

| Standardized RMSR (SRMSR) | 0.0220 | 0.0057 | 0.0298 | |

| Goodness of Fit Index (GFI) | 1.0000 | 1.0000 | 1.0000 | |

| Bentler-Bonett NFI | 0.9259 | 0.9950 | 0.8730 | |

When you examine the results of this table, the first thing you have to realize is that in general the group statistics are not independent. For example, although the overall chi-square statistic can be written as the weighted sum of fit functions of the groups, in general it does not imply that the individual terms are statistically independent. In the current two-group analysis, the overall chi-square is written as:

|

where  and

and  are sample sizes for the groups,

are sample sizes for the groups,  and

and  are the discrepancy functions for the groups. Even though

are the discrepancy functions for the groups. Even though  is chi-square distributed under the null hypothesis, in general the individual terms

is chi-square distributed under the null hypothesis, in general the individual terms  and

and  are not chi-square distributed under the same null hypothesis. So when you compare the group fits by using the statistics in Output 88.10.5, you should treat those as descriptive measures only.

are not chi-square distributed under the same null hypothesis. So when you compare the group fits by using the statistics in Output 88.10.5, you should treat those as descriptive measures only.

The current model is a special case where and are actually independent of each other. The reason is that there are no constrained parameters for the models fitted to the two groups. This would imply that the individual terms and are chi-squared distributed under the null hypothesis. Nonetheless, this fact is not important to our group comparison by using the descriptive statistics in Output 88.10.5. The values of and are shown in the row labeled "Fit Function." Group 1 (Region 1) is fitted better by its model ( ) than is group 2 (Region 2) by its model (

) than is group 2 (Region 2) by its model ( ). Next, the percentage contributions to the overall chi-square statistic for the two groups are shown. Group 1 contributes only 3% (

). Next, the percentage contributions to the overall chi-square statistic for the two groups are shown. Group 1 contributes only 3% ( ) while Group 2 contributes 97%. Other measures like RMSR, SRMSR, and Bentler-Bonett NFI show that group 1 data are fitted better. The GFI’s show equal fits for the two groups, however.

) while Group 2 contributes 97%. Other measures like RMSR, SRMSR, and Bentler-Bonett NFI show that group 1 data are fitted better. The GFI’s show equal fits for the two groups, however.

Despite a very good fit, the current model is not intended to be the final model. It was fitted mainly for illustration purposes. For multiple-group analysis, cross-group constraints are of primary interest and should be explored whenever appropriate. The first fitting with all model parameters constrained for the groups has been shown to be too restrictive, while the current model with no cross-group constraints fits very well–so well that it might have overfit unnecessarily. A multiple-group model between these extremes is now explored. The following specification is for such an intermediate model with cross-group constraints.

proc tcalis omethod=nrr modification;

group 1 / data=region1 label="Region 1" nobs=378;

group 2 / data=region2 label="Region 2" nobs=423;

model 1 / groups=1;

%BasepathModel

model 2 / groups=2;

refmodel 1;

mean

Spend02 Spend03 = G2_InterSpend02 G2_InterSpend03,

Courtesy Responsive Helpful

Delivery Pricing Availability

Quality = G2_intercept01-G2_intercept07;

simtest

SpendDiff = (Spend02Diff Spend03Diff)

MeasurementDiff = (CourtesyDiff ResponsiveDiff

HelpfulDiff DeliveryDiff

PricingDiff AvailabilityDiff

QualityDiff);

Spend02Diff = G2_InterSpend02 - InterSpend02;

Spend03Diff = G2_InterSpend03 - InterSpend03;

CourtesyDiff = G2_intercept01 - intercept01;

ResponsiveDiff = G2_intercept02 - intercept02;

HelpfulDiff = G2_intercept03 - intercept03;

DeliveryDiff = G2_intercept04 - intercept04;

PricingDiff = G2_intercept05 - intercept05;

AvailabilityDiff = G2_intercept06 - intercept06;

QualityDiff = G2_intercept07 - intercept07;

run;

In this specification, Region 1 is fitted by model 1, which is essentially unchanged from the previous analyses. Region 2 is fitted by model 2, which, again, is modified from model 1, as specified in the REFMODEL statement. The modification being made is the addition of unique mean parameters. In the MEAN statement, nine new parameters are specified. All these parameters are prefixed with G2_ to be distinguished from the parameters in model 1. Parameters G2_InterSpend02 and G2_InterSpend03 are intercepts for variables Spend02 and Spend03, respectively. Parameters G2_intercept01–G2_intercept07 are intercepts for the indicator measures of the latent variables. Because the latent variables in the model have means at fixed zeros, the intercept parameters G2_intercept01–G2_intercept07 and G2_InterSpend02 are also the means for the corresponding variables. To summarize, in this multiple-group model the covariance structures for the two regions are constrained to be the same, while the means structures are allowed to be unconstrained.

Additional statistics or tests are requested in the current PROC TCALIS run. The MODIFICATION option in the PROC TCALIS statement requests the Lagrange Multiplier tests and Wald tests be conducted. The Lagrange Multiplier tests provide information about which constrained or fixed parameters could be freed or added so as to improve the overall model fit. The Wald tests provide information about which existing parameters could be fixed at zeros (or eliminated) without significantly affecting the overall model fit. These tests will be discussed with more details when the results are presented.

In the SIMTEST statement, two simultaneous tests are requested. The first simultaneous test is named SpendDiff, which includes two parametric functions Spend02Diff and Spend03Diff. The second simultaneous test is named MeasurementDiff, which includes seven parametric functions: CourtesyDiff, ResponsiveDiff, HelpfulDiff, DeliveryDiff, PricingDiff, AvailabilityDiff, and QualityDiff. The null hypothesis of these simultaneous tests is of the form:

|

where  is the number of parametric functions within the simultaneous test. In the current analysis, the component parametric functions are defined in the SAS programming statements, which are shown in the last block of the specification. Essentially, all these parametric functions represent the differences of the mean or intercept parameters between the two models for groups. The first simultaneous test is intended to test whether the mean or intercept parameters in the structural models are the same, while the second simultaneous test is intended to test whether the mean parameters in the measurement models are the same.

is the number of parametric functions within the simultaneous test. In the current analysis, the component parametric functions are defined in the SAS programming statements, which are shown in the last block of the specification. Essentially, all these parametric functions represent the differences of the mean or intercept parameters between the two models for groups. The first simultaneous test is intended to test whether the mean or intercept parameters in the structural models are the same, while the second simultaneous test is intended to test whether the mean parameters in the measurement models are the same.

The fit summary table is shown in Output 88.10.6.

| Fit Summary | ||

|---|---|---|

| Modeling Info | N Observations | 801 |

| N Variables | 9 | |

| N Moments | 108 | |

| N Parameters | 40 | |

| N Active Constraints | 0 | |

| Independence Model Chi-Square | 399.7468 | |

| Independence Model Chi-Square DF | 72 | |

| Absolute Index | Fit Function | 0.1346 |

| Chi-Square | 107.5461 | |

| Chi-Square DF | 68 | |

| Pr > Chi-Square | 0.0016 | |

| Z-Test of Wilson & Hilferty | 2.9452 | |

| Hoelter Critical N | 657 | |

| Root Mean Square Residual (RMSR) | 0.1577 | |

| Standardized RMSR (SRMSR) | 0.0678 | |

| Goodness of Fit Index (GFI) | 1.0000 | |

| Parsimony Index | Adjusted GFI (AGFI) | 0.9999 |

| Parsimonious GFI | 0.9444 | |

| RMSEA Estimate | 0.0382 | |

| RMSEA Lower 90% Confidence Limit | 0.0237 | |

| RMSEA Upper 90% Confidence Limit | 0.0514 | |

| Probability of Close Fit | 0.9275 | |

| Akaike Information Criterion | -28.4539 | |

| Bozdogan CAIC | -415.0924 | |

| Schwarz Bayesian Criterion | -347.0924 | |

| McDonald Centrality | 0.9756 | |

| Incremental Index | Bentler Comparative Fit Index | 0.8793 |

| Bentler-Bonett NFI | 0.7310 | |

| Bentler-Bonett Non-normed Index | 0.8722 | |

| Bollen Normed Index Rho1 | 0.7151 | |

| Bollen Non-normed Index Delta2 | 0.8808 | |

| James et al. Parsimonious NFI | 0.6904 | |

The chi-square value is 107.55 (=68,  =0.0016), which is statistically significant. The null hypothesis of the mean and covariance structures is rejected if

=0.0016), which is statistically significant. The null hypothesis of the mean and covariance structures is rejected if  -level at

-level at  or larger is chosen. However, in practical structural equation modeling, the chi-square test is not the only criterion, or even an important criterion, for evaluating model fit. The RMSEA estimate for the current model is

or larger is chosen. However, in practical structural equation modeling, the chi-square test is not the only criterion, or even an important criterion, for evaluating model fit. The RMSEA estimate for the current model is  , which indicates a good fit. The probability level of close fit is

, which indicates a good fit. The probability level of close fit is  , indicating that a good population fit (RMSEA

, indicating that a good population fit (RMSEA  ) hypothesis cannot be rejected. GFI, AGFI, and parsimonious GFI all indicate good fit. However, the incremental indices show only respectable model fit.

) hypothesis cannot be rejected. GFI, AGFI, and parsimonious GFI all indicate good fit. However, the incremental indices show only respectable model fit.

Comparison of the model fit to the groups is shown in Output 88.10.7.

| Fit Comparison Among Groups | ||||

|---|---|---|---|---|

| Overall | Region 1 | Region 2 | ||

| Modeling Info | N Observations | 801 | 378 | 423 |

| N Variables | 9 | 9 | 9 | |

| N Moments | 108 | 54 | 54 | |

| N Parameters | 40 | 31 | 31 | |

| N Active Constraints | 0 | 0 | 0 | |

| Independence Model Chi-Square | 399.7468 | 173.4482 | 226.2986 | |

| Independence Model Chi-Square DF | 72 | 36 | 36 | |

| Fit Index | Fit Function | 0.1346 | 0.1261 | 0.1422 |

| Percent Contribution to Chi-Square | 100 | 44 | 56 | |

| Root Mean Square Residual (RMSR) | 0.1577 | 0.1552 | 0.1599 | |

| Standardized RMSR (SRMSR) | 0.0678 | 0.0792 | 0.0557 | |

| Goodness of Fit Index (GFI) | 1.0000 | 1.0000 | 1.0000 | |

| Bentler-Bonett NFI | 0.7310 | 0.7260 | 0.7348 | |

Looking at the percentage contribution to the chi-square, the Region 2 fitting shows a worse fit. However, this might be due to the larger sample size in Region 2. When comparing the fit of the two regions by using RMSR, which does not take the sample size into account, the fitting of two groups are about the same. The standardized RMSR even shows that Region 2 is fitted better. So, it seems to be safe to conclude that the models fit almost equally well (or badly) for the two regions.

Constrained parameter estimates for the two regions are shown in Output 88.10.8.

| Model 1. PATH List | ||||||

|---|---|---|---|---|---|---|

| Path | Parameter | Estimate | Standard Error |

t Value | ||

| Service | -> | Spend02 | a1 | 0.37475 | 0.21318 | 1.75795 |

| Service | -> | Spend03 | a2 | 0.53851 | 0.20840 | 2.58401 |

| Product | -> | Spend02 | a3 | 0.80372 | 0.21939 | 3.66347 |

| Product | -> | Spend03 | a4 | 0.59879 | 0.22144 | 2.70409 |

| Spend02 | -> | Spend03 | a5 | 0.08952 | 0.03694 | 2.42326 |

| Service | -> | Courtesy | b1 | 0.72418 | 0.07989 | 9.06482 |

| Service | -> | Responsive | b2 | 0.90452 | 0.08886 | 10.17972 |

| Service | -> | Helpful | b3 | 0.64969 | 0.07683 | 8.45574 |

| Service | -> | Delivery | b4 | 0.64473 | 0.09021 | 7.14677 |

| Product | -> | Pricing | b5 | 0.63452 | 0.07916 | 8.01600 |

| Product | -> | Availability | b6 | 0.76737 | 0.08265 | 9.28516 |

| Product | -> | Quality | b7 | 0.79716 | 0.08922 | 8.93470 |

| Model 1. Variance Parameters | |||||

|---|---|---|---|---|---|

| Variance Type |

Variable | Parameter | Estimate | Standard Error |

t Value |

| Error | Courtesy | theta01 | 1.98374 | 0.13169 | 15.06379 |

| Responsive | theta02 | 2.02152 | 0.16159 | 12.51005 | |

| Helpful | theta03 | 1.96535 | 0.12263 | 16.02727 | |

| Delivery | theta04 | 2.97542 | 0.17049 | 17.45184 | |

| Pricing | theta05 | 1.93952 | 0.12326 | 15.73583 | |

| Availability | theta06 | 1.63156 | 0.13067 | 12.48646 | |

| Quality | theta07 | 2.08849 | 0.15329 | 13.62464 | |

| Spend02 | theta08 | 13.47066 | 0.71842 | 18.75051 | |

| Spend03 | theta09 | 13.02883 | 0.68682 | 18.96966 | |

| Exogenous | Service | 1.00000 | |||

| Product | 1.00000 | ||||

All parameter estimates but one are statistically significant at  . The parameter a1, which represents the path coefficient from Service to Spend02, has a

. The parameter a1, which represents the path coefficient from Service to Spend02, has a  -value of

-value of  . This is only marginally significant. Although all these results bear the title of model 1, these estimates are the same for model 2, of which the corresponding results are not shown here.

. This is only marginally significant. Although all these results bear the title of model 1, these estimates are the same for model 2, of which the corresponding results are not shown here.

The mean and intercept parameters for the two models (regions) are shown in Output 88.10.9.

| Model 1. Means and Intercepts | |||||

|---|---|---|---|---|---|

| Type | Variable | Parameter | Estimate | Standard Error |

t Value |

| Mean | Service | 0 | |||

| Product | 0 | ||||

| Intercept | Spend02 | InterSpend02 | 183.50000 | 0.19585 | 936.95628 |

| Spend03 | InterSpend03 | 285.49480 | 6.78127 | 42.10048 | |

| Courtesy | intercept01 | 4.31200 | 0.08157 | 52.86519 | |

| Responsive | intercept02 | 4.72400 | 0.08679 | 54.43096 | |

| Helpful | intercept03 | 3.92100 | 0.07958 | 49.27201 | |

| Delivery | intercept04 | 4.35700 | 0.09484 | 45.93968 | |

| Pricing | intercept05 | 6.14400 | 0.07882 | 77.94992 | |

| Availability | intercept06 | 4.99400 | 0.07674 | 65.07315 | |

| Quality | intercept07 | 5.97100 | 0.08500 | 70.24543 | |

| Model 2. Means and Intercepts | |||||

|---|---|---|---|---|---|

| Type | Variable | Parameter | Estimate | Standard Error |

t Value |

| Mean | Service | 0 | |||

| Product | 0 | ||||

| Intercept | Spend02 | G2_InterSpend02 | 156.25000 | 0.18511 | 844.09015 |

| Spend03 | G2_InterSpend03 | 299.68311 | 5.77478 | 51.89515 | |

| Courtesy | G2_intercept01 | 2.41200 | 0.07709 | 31.28628 | |

| Responsive | G2_intercept02 | 2.72700 | 0.08203 | 33.24350 | |

| Helpful | G2_intercept03 | 5.22400 | 0.07522 | 69.45319 | |

| Delivery | G2_intercept04 | 6.37600 | 0.08964 | 71.12697 | |

| Pricing | G2_intercept05 | 7.14700 | 0.07450 | 95.93427 | |

| Availability | G2_intercept06 | 3.23300 | 0.07254 | 44.57020 | |

| Quality | G2_intercept07 | 5.11900 | 0.08034 | 63.71500 | |

All the mean and intercept estimates are statistically significant at  . Except for the fixed zero means for Service and Product, a quick glimpse of these mean and intercepts estimates shows a quite different pattern for the two models. Do these estimates truly differ beyond chance? The simultaneous tests of these parameter estimates shown in Output 88.10.10 can confirm this.

. Except for the fixed zero means for Service and Product, a quick glimpse of these mean and intercepts estimates shows a quite different pattern for the two models. Do these estimates truly differ beyond chance? The simultaneous tests of these parameter estimates shown in Output 88.10.10 can confirm this.

In Output 88.10.10, there are two simultaneous tests, as requested in the original statements.

| Simultaneous Tests | |||||

|---|---|---|---|---|---|

| Simultaneous Test |

Parametric Function |

Function Value |

DF | Chi-Square | p Value |

| SpendDiff | 2 | 10458 | <.0001 | ||

| Spend02Diff | -27.25000 | 1 | 10225 | <.0001 | |

| Spend03Diff | 14.18831 | 1 | 185.86725 | <.0001 | |

| MeasurementDiff | 7 | 1610 | <.0001 | ||

| CourtesyDiff | -1.90000 | 1 | 286.58605 | <.0001 | |

| ResponsiveDiff | -1.99700 | 1 | 279.63659 | <.0001 | |

| HelpfulDiff | 1.30300 | 1 | 141.59942 | <.0001 | |

| DeliveryDiff | 2.01900 | 1 | 239.35318 | <.0001 | |

| PricingDiff | 1.00300 | 1 | 85.52567 | <.0001 | |

| AvailabilityDiff | -1.76100 | 1 | 278.09360 | <.0001 | |

| QualityDiff | -0.85200 | 1 | 53.06240 | <.0001 | |

The first one is SpendDiff, which tests simultaneously the hypotheses that:

|

|

|

|||

|

|

|

The exceedingly large chi-square value  suggests the composite null hypothesis is false. Individual tests for these hypotheses suggest each of these hypotheses should be rejected. The chi-square values for individual tests are

suggests the composite null hypothesis is false. Individual tests for these hypotheses suggest each of these hypotheses should be rejected. The chi-square values for individual tests are  and

and  , respectively.

, respectively.

Similarly, the simultaneous and individual tests of the intercepts in the measurement model suggest that the two models (groups) differ significantly in the means of the measured variables. Region 2 has significantly higher means in variables Helpful, Delivery, and Pricing, but significantly lower means in variables Courtesy, Responsive, Availability, and Quality.

Now you are ready to answer the main research questions asked. The overall customer service (Service) does affect the future purchase (Spend03), but not the current purchase (Spend02), as the path coefficient a1 is only marginally significant. This perhaps is an artifact because the rating was done after the purchases in 2002. That is, purchases in 2002 had been done before the impression about customer service was fully formed. However, this argument cannot explain why overall customer service (Service) also shows a strong and significant relationship with purchases in 2002 (Spend02). Nonetheless, customer service and product quality do affect the future purchases (Spend03) in an expected way, even after partialling out the effect of the previous purchase amount (Spend02). Apart from the mean differences of the variables, the common measurement and prediction (or structural) models fit the two regions very well.

Because the current model fits well and most parts of fitting meet your expectations, you might accept this model without looking for further improvement. Nonetheless, for illustration purposes, it would be useful to consider the LM test results. In Output 88.10.11, ranked LM statistics for the path coefficients in model 1 and model 2 are shown.

| Model 1. Rank Order of the 10 Largest LM Stat for Path Relations | ||||

|---|---|---|---|---|

| To | From | LM Stat | Pr > ChiSq | Parm Change |

| Service | Courtesy | 11.15249 | 0.0008 | -0.17145 |

| Service | Helpful | 3.09038 | 0.0788 | 0.09431 |

| Service | Delivery | 2.59511 | 0.1072 | 0.07504 |

| Courtesy | Responsive | 1.75943 | 0.1847 | -0.07730 |

| Delivery | Courtesy | 1.66721 | 0.1966 | 0.08669 |

| Helpful | Courtesy | 1.62005 | 0.2031 | 0.07277 |

| Courtesy | Product | 1.48928 | 0.2223 | -0.14815 |

| Service | Product | 0.83498 | 0.3608 | -0.12327 |

| Responsive | Helpful | 0.76664 | 0.3813 | -0.05625 |

| Product | Helpful | 0.53020 | 0.4665 | -0.03831 |

| Model 2. Rank Order of the 10 Largest LM Stat for Path Relations | ||||

|---|---|---|---|---|

| To | From | LM Stat | Pr > ChiSq | Parm Change |

| Delivery | Courtesy | 16.91167 | <.0001 | -0.26641 |

| Service | Courtesy | 9.11235 | 0.0025 | 0.15430 |

| Courtesy | Delivery | 8.12091 | 0.0044 | -0.12989 |

| Courtesy | Responsive | 8.03954 | 0.0046 | 0.16215 |

| Pricing | Responsive | 5.48406 | 0.0192 | 0.10424 |

| Courtesy | Product | 4.39347 | 0.0361 | 0.24412 |

| Courtesy | Quality | 3.52147 | 0.0606 | 0.08672 |

| Service | Delivery | 3.20160 | 0.0736 | -0.08281 |

| Service | Helpful | 2.97015 | 0.0848 | -0.09198 |

| Responsive | Pricing | 2.91498 | 0.0878 | 0.08943 |

Path coefficients that lead to better improvement (larger chi-square drop) are shown first in the tables. For example, the first path coefficient suggested to be freed in model 1 is the Service <– Courtesy path. The associated -value is  and the estimated change of parameter value is

and the estimated change of parameter value is  . The second path coefficient is for the Service <– Helpful path, but it is not significant at the

. The second path coefficient is for the Service <– Helpful path, but it is not significant at the  level. So, is it good to add the Service <– Courtesy path to model 1, based on the LM test results? The answer is that it depends on your applications and the theoretical and practical implications. For instance, the Service –> Courtesy path, which is a part of the measurement model, is already specified in model 1. Even though the LM test statistic shows a significant drop of model fit chi-square, adding the Service <– Courtesy path might destroy the measurement model and lead to problematic interpretations. In this case, it is wise not to add the Service <– Courtesy path, which is suggested by the LM test results.

level. So, is it good to add the Service <– Courtesy path to model 1, based on the LM test results? The answer is that it depends on your applications and the theoretical and practical implications. For instance, the Service –> Courtesy path, which is a part of the measurement model, is already specified in model 1. Even though the LM test statistic shows a significant drop of model fit chi-square, adding the Service <– Courtesy path might destroy the measurement model and lead to problematic interpretations. In this case, it is wise not to add the Service <– Courtesy path, which is suggested by the LM test results.

LM tests for the path coefficients in model 2 are shown in the bottom of Output 88.10.11. Quite a few of these tests suggest significant improvements in model fit. Again, you are cautioned against adding these paths blindly.

LM tests for the error variances and covariances are shown in Output 88.10.12.

| Model 1. Rank Order of the 10 Largest LM Stat for Error Variances and Covariances | ||||

|---|---|---|---|---|

| Error of |

Error of |

LM Stat | Pr > ChiSq | Parm Change |

| Responsive | Helpful | 1.26589 | 0.2605 | -0.15774 |

| Delivery | Courtesy | 0.70230 | 0.4020 | 0.12577 |

| Helpful | Courtesy | 0.50167 | 0.4788 | 0.09103 |

| Quality | Availability | 0.47993 | 0.4885 | -0.09739 |

| Quality | Pricing | 0.45925 | 0.4980 | 0.09449 |

| Responsive | Availability | 0.25734 | 0.6120 | 0.05965 |

| Helpful | Availability | 0.24811 | 0.6184 | -0.05413 |

| Responsive | Pricing | 0.23748 | 0.6260 | -0.05911 |

| Spend02 | Availability | 0.19634 | 0.6577 | -0.13200 |

| Responsive | Courtesy | 0.18212 | 0.6696 | 0.06201 |

| Model 2. Rank Order of the 10 Largest LM Stat for Error Variances and Covariances | ||||

|---|---|---|---|---|

| Error of |

Error of |

LM Stat | Pr > ChiSq | Parm Change |

| Delivery | Courtesy | 16.00996 | <.0001 | -0.57408 |

| Responsive | Pricing | 4.89190 | 0.0270 | 0.25403 |

| Helpful | Delivery | 3.33480 | 0.0678 | 0.25299 |

| Delivery | Availability | 2.79513 | 0.0946 | 0.20656 |

| Responsive | Availability | 2.16944 | 0.1408 | -0.16421 |

| Quality | Courtesy | 2.14952 | 0.1426 | 0.17094 |

| Responsive | Courtesy | 2.12832 | 0.1446 | 0.20604 |

| Quality | Pricing | 2.00978 | 0.1563 | -0.19154 |

| Quality | Availability | 1.99477 | 0.1578 | 0.19459 |

| Responsive | Quality | 1.88736 | 0.1695 | -0.16963 |

Using , you might consider adding two pairs of correlated errors in model 2. The first pair is for Delivery and Courtesy, which has a -value less than  . The second pair is Pricing and Responsive, which has a -value of

. The second pair is Pricing and Responsive, which has a -value of  . Again, adding correlated errors (in the PCOV statement) should not be a pure statistical consideration. You should also consider theoretical and practical implications.

. Again, adding correlated errors (in the PCOV statement) should not be a pure statistical consideration. You should also consider theoretical and practical implications.

LM tests for other subsets of parameters are also conducted. Some subsets do not have parameters that can be freed and so they are not shown here. Other subsets are simply not shown here for conserving space.

PROC TCALIS ranks and outputs the LM test results for some default subsets of parameters. You have seen the subsets for path coefficients and correlated errors in the two previous outputs. Some other LM test results are not shown. With this kind of default LM output, there could be a huge amount of modification indices to look at. Fortunately, you can limit the LM test results to any subsets of potential parameters that you might be interested in. With your substantive knowledge, you can define such meaningful subsets of potential parameters by using the LMTESTS statement. The LM test indices and rankings will then be done for each predefined subset of potential parameters. With these customized LM results, you can limit your attention to consider only those meaningful parameters to be added. See the LMTESTS statement for details.

The next group of LM tests is for releasing implicit equality constraints in your model, as shown in Output 88.10.13.

| Lagrange Multiplier Statistics for Releasing Equality Constraints | ||||||||

|---|---|---|---|---|---|---|---|---|

| Parm | Released Parameter | LM Stat | Pr > ChiSq | Changes | ||||

Model |

Type |

Var1 |

Var2 |

Original Parm |

Released Parm |

|||

| a1 | 1 | DV_IV | Spend02 | Service | 0.01554 | 0.9008 | -0.0213 | 0.0238 |

| 2 | DV_IV | Spend02 | Service | 0.01554 | 0.9008 | 0.0238 | -0.0213 | |

| a2 | 1 | DV_IV | Spend03 | Service | 0.01763 | 0.8944 | -0.0222 | 0.0248 |

| 2 | DV_IV | Spend03 | Service | 0.01763 | 0.8944 | 0.0248 | -0.0222 | |

| a3 | 1 | DV_IV | Spend02 | Product | 0.0003403 | 0.9853 | -0.00321 | 0.00355 |

| 2 | DV_IV | Spend02 | Product | 0.0003403 | 0.9853 | 0.00355 | -0.00321 | |

| a4 | 1 | DV_IV | Spend03 | Product | 0.00176 | 0.9665 | 0.00714 | -0.00802 |

| 2 | DV_IV | Spend03 | Product | 0.00176 | 0.9665 | -0.00802 | 0.00714 | |

| a5 | 1 | DV_DV | Spend03 | Spend02 | 0.0009698 | 0.9752 | -0.00100 | 0.00112 |

| 2 | DV_DV | Spend03 | Spend02 | 0.0009698 | 0.9752 | 0.00112 | -0.00100 | |

| b1 | 1 | DV_IV | Courtesy | Service | 19.17225 | <.0001 | 0.2851 | -0.3191 |

| 2 | DV_IV | Courtesy | Service | 19.17225 | <.0001 | -0.3191 | 0.2851 | |

| b2 | 1 | DV_IV | Responsive | Service | 0.21266 | 0.6447 | -0.0304 | 0.0341 |

| 2 | DV_IV | Responsive | Service | 0.21266 | 0.6447 | 0.0341 | -0.0304 | |

| b3 | 1 | DV_IV | Helpful | Service | 4.60629 | 0.0319 | -0.1389 | 0.1555 |

| 2 | DV_IV | Helpful | Service | 4.60629 | 0.0319 | 0.1555 | -0.1389 | |

| b4 | 1 | DV_IV | Delivery | Service | 3.59763 | 0.0579 | -0.1508 | 0.1687 |

| 2 | DV_IV | Delivery | Service | 3.59763 | 0.0579 | 0.1687 | -0.1508 | |

| b5 | 1 | DV_IV | Pricing | Product | 0.50974 | 0.4753 | 0.0468 | -0.0524 |

| 2 | DV_IV | Pricing | Product | 0.50974 | 0.4753 | -0.0524 | 0.0468 | |

| b6 | 1 | DV_IV | Availability | Product | 0.57701 | 0.4475 | -0.0457 | 0.0512 |

| 2 | DV_IV | Availability | Product | 0.57701 | 0.4475 | 0.0512 | -0.0457 | |

| b7 | 1 | DV_IV | Quality | Product | 0.00566 | 0.9400 | -0.00511 | 0.00574 |

| 2 | DV_IV | Quality | Product | 0.00566 | 0.9400 | 0.00574 | -0.00511 | |

| theta01 | 1 | COVERR | Courtesy | Courtesy | 45.24725 | <.0001 | 0.7204 | -0.8064 |

| 2 | COVERR | Courtesy | Courtesy | 45.24725 | <.0001 | -0.8064 | 0.7204 | |

| theta02 | 1 | COVERR | Responsive | Responsive | 1.73499 | 0.1878 | -0.1555 | 0.1740 |

| 2 | COVERR | Responsive | Responsive | 1.73499 | 0.1878 | 0.1740 | -0.1555 | |

| theta03 | 1 | COVERR | Helpful | Helpful | 11.13266 | 0.0008 | -0.3448 | 0.3860 |

| 2 | COVERR | Helpful | Helpful | 11.13266 | 0.0008 | 0.3860 | -0.3448 | |

| theta04 | 1 | COVERR | Delivery | Delivery | 4.99097 | 0.0255 | -0.3364 | 0.3766 |

| 2 | COVERR | Delivery | Delivery | 4.99097 | 0.0255 | 0.3766 | -0.3364 | |

| theta05 | 1 | COVERR | Pricing | Pricing | 2.86428 | 0.0906 | 0.1729 | -0.1936 |

| 2 | COVERR | Pricing | Pricing | 2.86428 | 0.0906 | -0.1936 | 0.1729 | |

| theta06 | 1 | COVERR | Availability | Availability | 2.53147 | 0.1116 | -0.1494 | 0.1672 |

| 2 | COVERR | Availability | Availability | 2.53147 | 0.1116 | 0.1672 | -0.1494 | |

| theta07 | 1 | COVERR | Quality | Quality | 0.07328 | 0.7866 | -0.0315 | 0.0352 |

| 2 | COVERR | Quality | Quality | 0.07328 | 0.7866 | 0.0352 | -0.0315 | |

| theta08 | 1 | COVERR | Spend02 | Spend02 | 0.00214 | 0.9631 | 0.0304 | -0.0340 |

| 2 | COVERR | Spend02 | Spend02 | 0.00214 | 0.9631 | -0.0340 | 0.0304 | |

| theta09 | 1 | COVERR | Spend03 | Spend03 | 0.0001773 | 0.9894 | -0.00842 | 0.00946 |

| 2 | COVERR | Spend03 | Spend03 | 0.0001773 | 0.9894 | 0.00946 | -0.00842 | |

| phi | 1 | COVEXOG | Service | Product | 0.87147 | 0.3505 | 0.0605 | -0.0678 |

| 2 | COVEXOG | Service | Product | 0.87147 | 0.3505 | -0.0678 | 0.0605 | |

Recall that the measurement and the prediction models for the two regions are constrained to be the same by model referencing (that is, the REFMODEL statement). Output 88.10.13 shows you which parameter can be unconstrained so that your overall model fit might improve. For example, if you unconstrain the first parameter a1 for the two models, the expected chi-square drop (LM Stat) is about  , which is not significant (

, which is not significant ( ). The associated parameter changes are small too. However, if you consider unconstraining parameter b1, the expected drop of chi-square is

). The associated parameter changes are small too. However, if you consider unconstraining parameter b1, the expected drop of chi-square is  (

( ). There are two rows for this parameter. Each row represents a parameter location to be released from the equality constraint. Consider the first row first. If you rename the coefficient for the Courtesy <– Service path in model 1 to a new parameter, say "new" (while keeping b1 as the parameter for the Courtesy <– Service path in model 2), and fit the model again, the new estimate of b1 will be

). There are two rows for this parameter. Each row represents a parameter location to be released from the equality constraint. Consider the first row first. If you rename the coefficient for the Courtesy <– Service path in model 1 to a new parameter, say "new" (while keeping b1 as the parameter for the Courtesy <– Service path in model 2), and fit the model again, the new estimate of b1 will be  larger than the previous b1 estimate. The estimate of "new" would be

larger than the previous b1 estimate. The estimate of "new" would be  less than the previous b1 estimate. The second row for the b1 parameter shows similar but reflected results. It is for renaming the parameter location in model 2. For this example each equality constraint has exactly two locations, one for model 1 and one for model 2. That is the reason why you always observe reflected results for freeing the locations successively. Reflected results are not the case if you have equality constraints with more than two parameter locations.

less than the previous b1 estimate. The second row for the b1 parameter shows similar but reflected results. It is for renaming the parameter location in model 2. For this example each equality constraint has exactly two locations, one for model 1 and one for model 2. That is the reason why you always observe reflected results for freeing the locations successively. Reflected results are not the case if you have equality constraints with more than two parameter locations.

Another example of big expected improvement of model fit is by freeing the constrained variances of Courtesy among the two models. The corresponding row to look at is the row with parameter theta01, where the parameter type is labeled "COVERR" and the values for the Var1 and Var2 are both "Courtesy." The LM statistic is  , which is a significant chi-square drop if you free either parameter locations. If you choose to rename the error variance for Courtesy in model 1, the new theta01 estimate will be

, which is a significant chi-square drop if you free either parameter locations. If you choose to rename the error variance for Courtesy in model 1, the new theta01 estimate will be  smaller than the original theta01 estimate. The new estimate of the error variance for Courtesy in model 2 will be

smaller than the original theta01 estimate. The new estimate of the error variance for Courtesy in model 2 will be  larger than the previous theta01 estimate. Finally, the constrained parameter theta03, which is the error variance parameter for Helpful in both models, is also a potential constraint that can be released with a significant model fit improvement.

larger than the previous theta01 estimate. Finally, the constrained parameter theta03, which is the error variance parameter for Helpful in both models, is also a potential constraint that can be released with a significant model fit improvement.

In addition to the LM statistics for suggesting ways to improve model fit, PROC TCALIS also computes the Wald tests to show which parameters can be constrained to zero without jeopardizing the model fit significantly. The Wald test results are shown in Output 88.10.14.

In Output 88.10.14, you see that a1 is suggested to be a fixed zero parameter (or eliminated from the model) by the Wald test. Fixing this parameter to zero (or dropping the Spend02 <– Service path from the model) is expected to increase the model fit chi-square by  (=.079), which is only marginally significant at

(=.079), which is only marginally significant at  .

.

As is the case for the LM test statistics, you should not automatically adhere to the suggestions by the Wald statistics. Substantive and theoretical considerations should always be considered when determining whether a parameter should be added or dropped.

Note: This procedure is experimental.

Copyright © 2009 by SAS Institute Inc., Cary, NC, USA. All rights reserved.