The X12 Procedure

- Overview

-

Getting Started

-

SyntaxFunctional SummaryPROC X12 StatementADJUST StatementARIMA StatementAUTOMDL StatementBY StatementCHECK StatementESTIMATE StatementEVENT StatementFORECAST StatementID StatementIDENTIFY StatementINPUT StatementOUTLIER StatementOUTPUT StatementPICKMDL StatementREGRESSION StatementSEATSDECOMP StatementTABLES StatementTRANSFORM StatementUSERDEFINED StatementVAR StatementX11 Statement

-

DetailsData RequirementsMissing ValuesSAS Predefined EventsUser-Defined Regression VariablesCombined Test for the Presence of Identifiable SeasonalityComputationsPICKMDL Model SelectionSEATS DecompositionDisplayed Output, ODS Table Names, and OUTPUT Tablename KeywordsUsing Auxiliary Variables to Subset Output Data SetsODS GraphicsOUT= Data SetSEATSDECOMP OUT= Data SetSpecial Data Sets

-

ExamplesARIMA Model IdentificationModel EstimationSeasonal AdjustmentRegARIMA Automatic Model SelectionAutomatic Outlier DetectionUser-Defined RegressorsMDLINFOIN= and MDLINFOOUT= Data SetsSetting Regression ParametersCreating an MDLINFO= Data Set for Use with the PICKMDL StatementIllustration of ODS GraphicsAUXDATA= Data Set

- References

Example 38.1 ARIMA Model Identification

This example shows typical PROC X12 statements that are used for ARIMA model identification. This example invokes the X12 procedure and uses the TRANSFORM and IDENTIFY statements. It specifies the time series data, takes the logarithm of the series (TRANSFORM statement), and generates ACFs and PACFs for the specified levels of differencing (IDENTIFY statement). The ACFs and PACFs for DIFF=1 and SDIFF=1 are shown in Output 38.1.1, Output 38.1.2, Output 38.1.3, and Output 38.1.4. The data set is the same as in the section Basic Seasonal Adjustment.

The graphical displays are available when ODS Graphics is enabled. For more information about the graphics available in the X12 procedure, see the section ODS Graphics.

proc x12 data=sales date=date; var sales; transform power=0; identify diff=(0,1) sdiff=(0,1); run;

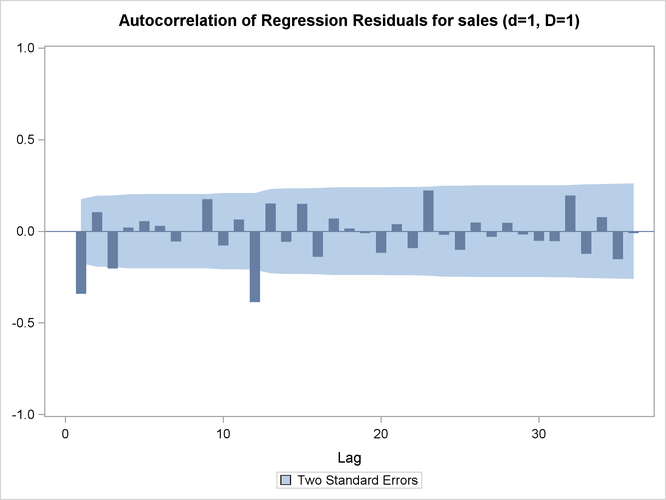

Output 38.1.1: ACFs (Nonseasonal Order=1 Seasonal Order=1)

| Autocorrelation of Regression Residuals for ARIMA Model Identification | |||||

|---|---|---|---|---|---|

| For Variable sales | |||||

| Differencing: Nonseasonal Order=1 Seasonal Order=1 | |||||

| Lag | Correlation | Standard Error | Chi-Square | DF | Pr > ChiSq |

| 1 | -0.34112 | 0.08737 | 15.5957 | 1 | <.0001 |

| 2 | 0.10505 | 0.09701 | 17.0860 | 2 | 0.0002 |

| 3 | -0.20214 | 0.09787 | 22.6478 | 3 | <.0001 |

| 4 | 0.02136 | 0.10101 | 22.7104 | 4 | 0.0001 |

| 5 | 0.05565 | 0.10104 | 23.1387 | 5 | 0.0003 |

| 6 | 0.03080 | 0.10128 | 23.2709 | 6 | 0.0007 |

| 7 | -0.05558 | 0.10135 | 23.7050 | 7 | 0.0013 |

| 8 | -0.00076 | 0.10158 | 23.7050 | 8 | 0.0026 |

| 9 | 0.17637 | 0.10158 | 28.1473 | 9 | 0.0009 |

| 10 | -0.07636 | 0.10389 | 28.9869 | 10 | 0.0013 |

| 11 | 0.06438 | 0.10432 | 29.5887 | 11 | 0.0018 |

| 12 | -0.38661 | 0.10462 | 51.4728 | 12 | <.0001 |

| 13 | 0.15160 | 0.11501 | 54.8664 | 13 | <.0001 |

| 14 | -0.05761 | 0.11653 | 55.3605 | 14 | <.0001 |

| 15 | 0.14957 | 0.11674 | 58.7204 | 15 | <.0001 |

| 16 | -0.13894 | 0.11820 | 61.6452 | 16 | <.0001 |

| 17 | 0.07048 | 0.11944 | 62.4045 | 17 | <.0001 |

| 18 | 0.01563 | 0.11975 | 62.4421 | 18 | <.0001 |

| 19 | -0.01061 | 0.11977 | 62.4596 | 19 | <.0001 |

| 20 | -0.11673 | 0.11978 | 64.5984 | 20 | <.0001 |

| 21 | 0.03855 | 0.12064 | 64.8338 | 21 | <.0001 |

| 22 | -0.09136 | 0.12074 | 66.1681 | 22 | <.0001 |

| 23 | 0.22327 | 0.12126 | 74.2099 | 23 | <.0001 |

| 24 | -0.01842 | 0.12436 | 74.2652 | 24 | <.0001 |

| 25 | -0.10029 | 0.12438 | 75.9183 | 25 | <.0001 |

| 26 | 0.04857 | 0.12500 | 76.3097 | 26 | <.0001 |

| 27 | -0.03024 | 0.12514 | 76.4629 | 27 | <.0001 |

| 28 | 0.04713 | 0.12520 | 76.8387 | 28 | <.0001 |

| 29 | -0.01803 | 0.12533 | 76.8943 | 29 | <.0001 |

| 30 | -0.05107 | 0.12535 | 77.3442 | 30 | <.0001 |

| 31 | -0.05377 | 0.12551 | 77.8478 | 31 | <.0001 |

| 32 | 0.19573 | 0.12569 | 84.5900 | 32 | <.0001 |

| 33 | -0.12242 | 0.12799 | 87.2543 | 33 | <.0001 |

| 34 | 0.07775 | 0.12888 | 88.3401 | 34 | <.0001 |

| 35 | -0.15245 | 0.12924 | 92.5584 | 35 | <.0001 |

| 36 | -0.01000 | 0.13061 | 92.5767 | 36 | <.0001 |

| Note: | The P-values approximate the probability of observing a Chi-Square at least this large when the model fitted is correct. When DF is positive, small values of P, customarily those below 0.05, indicate model inadequacy. |

Output 38.1.2: Plot for ACFs (Nonseasonal Order=1 Seasonal Order=1)

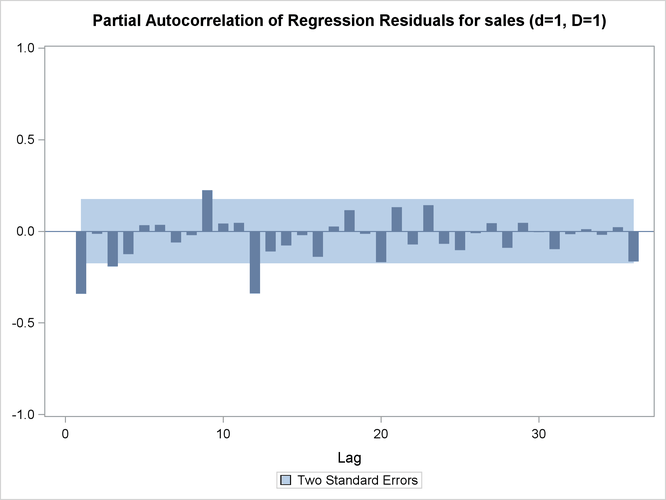

Output 38.1.3: PACFs (Nonseasonal Order=1 Seasonal Order=1)

| Partial Autocorrelations of Regression Residuals for ARIMA Model Identification |

||

|---|---|---|

| For Variable sales | ||

| Differencing: Nonseasonal Order=1 Seasonal Order=1 |

||

| Lag | Correlation | Standard Error |

| 1 | -0.34112 | 0.08737 |

| 2 | -0.01281 | 0.08737 |

| 3 | -0.19266 | 0.08737 |

| 4 | -0.12503 | 0.08737 |

| 5 | 0.03309 | 0.08737 |

| 6 | 0.03468 | 0.08737 |

| 7 | -0.06019 | 0.08737 |

| 8 | -0.02022 | 0.08737 |

| 9 | 0.22558 | 0.08737 |

| 10 | 0.04307 | 0.08737 |

| 11 | 0.04659 | 0.08737 |

| 12 | -0.33869 | 0.08737 |

| 13 | -0.10918 | 0.08737 |

| 14 | -0.07684 | 0.08737 |

| 15 | -0.02175 | 0.08737 |

| 16 | -0.13955 | 0.08737 |

| 17 | 0.02589 | 0.08737 |

| 18 | 0.11482 | 0.08737 |

| 19 | -0.01316 | 0.08737 |

| 20 | -0.16743 | 0.08737 |

| 21 | 0.13240 | 0.08737 |

| 22 | -0.07204 | 0.08737 |

| 23 | 0.14285 | 0.08737 |

| 24 | -0.06733 | 0.08737 |

| 25 | -0.10267 | 0.08737 |

| 26 | -0.01007 | 0.08737 |

| 27 | 0.04378 | 0.08737 |

| 28 | -0.08995 | 0.08737 |

| 29 | 0.04690 | 0.08737 |

| 30 | -0.00490 | 0.08737 |

| 31 | -0.09638 | 0.08737 |

| 32 | -0.01528 | 0.08737 |

| 33 | 0.01150 | 0.08737 |

| 34 | -0.01916 | 0.08737 |

| 35 | 0.02303 | 0.08737 |

| 36 | -0.16488 | 0.08737 |

Output 38.1.4: Plot for PACFs (Nonseasonal Order=1 Seasonal Order=1)