The ENTROPY Procedure (Experimental)

- Overview

-

Getting Started

-

Syntax

-

Details

Generalized Maximum Entropy Generalized Cross Entropy Moment Generalized Maximum Entropy Maximum Entropy-Based Seemingly Unrelated Regression Generalized Maximum Entropy for Multinomial Discrete Choice Models Censored or Truncated Dependent Variables Information Measures Parameter Covariance For GCE Parameter Covariance For GCE-M Statistical Tests Missing Values Input Data Sets Output Data Sets ODS Table Names ODS Graphics

-

Examples

- References

| Statistical Tests |

Since the GME estimates have been shown to be asymptotically normally distributed, the classical Wald, Lagrange mulitiplier, and likelihood ratio statistics can be used for testing linear restrictions on the parameters.

Wald Tests

Let  , where

, where  is a set of linearly independent combinations of the elements of

is a set of linearly independent combinations of the elements of  . Then under the null hypothesis, the Wald test statistic,

. Then under the null hypothesis, the Wald test statistic,

|

has a central  limiting distribution with degrees of freedom equal to the rank of .

limiting distribution with degrees of freedom equal to the rank of .

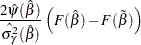

Pseudo-Likelihood Ratio Tests

Using the conditionally maximized entropy function as a pseudo-likelihood,  , Mittelhammer and Cardell (2000) state that:

, Mittelhammer and Cardell (2000) state that:

|

has the limiting distribution of the Wald statistic when testing the same hypothesis. Note that  and

and  are the maximum values of the entropy objective function over the full and restricted parameter spaces, respectively.

are the maximum values of the entropy objective function over the full and restricted parameter spaces, respectively.

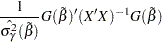

Lagrange Multiplier Tests

Again using the GME function as a pseudo-likelihood, Mittelhammer and Cardell (2000) define the Lagrange multiplier statistic as:

|

where  is the gradient of , which is being evaluated at the optimum point for the restricted parameters. This test statistic shares the same limiting distribution as the Wald and pseudo-likelihood ratio tests.

is the gradient of , which is being evaluated at the optimum point for the restricted parameters. This test statistic shares the same limiting distribution as the Wald and pseudo-likelihood ratio tests.

Note: This procedure is experimental.