Sample 60856: Testing for Returns to Scale in a Cobb-Douglas Production Function

|  |  |  |

Overview

A production function is a function that summarizes the conversion of inputs in to outputs. For example, the production of cars using steel, labor, machinery, and plant facilities could be described as  . Production functions can be applied to a single firm, an industry, or an entire nation. Note, however, that they are limited to producing a single output, so that joint production is disallowed, although multiple inputs are used. The simplest production function used frequently in economics is a Cobb-Douglas production function. This is a two-input production function that takes on the form

. Production functions can be applied to a single firm, an industry, or an entire nation. Note, however, that they are limited to producing a single output, so that joint production is disallowed, although multiple inputs are used. The simplest production function used frequently in economics is a Cobb-Douglas production function. This is a two-input production function that takes on the form

![\[ q = f(K,L) = AK^\alpha L^\beta \cdot e^\epsilon \]](http://support.sas.com/rnd/app/ets/examples/cobbdoug/images/ets_webex_cobbdoug0002.png) |

where output,  , is a function of two inputs, capital (

, is a function of two inputs, capital ( ) and labor (

) and labor ( ). The parameters

). The parameters  and

and  are all positive constants calculated from empirical data and

are all positive constants calculated from empirical data and  is a multiplicative exponential error. This type of production function is particularly useful since it is linear in logarithms and can be used to determine whether the inputs exhibit increasing, decreasing, or constant returns to scale. For example, suppose both the capital and the labor inputs are doubled. The Cobb-Douglas production function helps you determine what happens to the output. Will it also increase by double? Will output increase by more than double? Will it increase by some amount less than double?

is a multiplicative exponential error. This type of production function is particularly useful since it is linear in logarithms and can be used to determine whether the inputs exhibit increasing, decreasing, or constant returns to scale. For example, suppose both the capital and the labor inputs are doubled. The Cobb-Douglas production function helps you determine what happens to the output. Will it also increase by double? Will output increase by more than double? Will it increase by some amount less than double?

Formally, for constant returns to scale,  . That is, if both of the inputs, capital and labor, are increased by a factor of

. That is, if both of the inputs, capital and labor, are increased by a factor of  , then output also increases by a factor of . For increasing returns, if both capital and labor are increased by a factor of , then output increases by an amount greater than . In this case,

, then output also increases by a factor of . For increasing returns, if both capital and labor are increased by a factor of , then output increases by an amount greater than . In this case,  . The opposite is true for decreasing returns. If both capital and labor are increased by a factor of , then output increases by an amount less than such that

. The opposite is true for decreasing returns. If both capital and labor are increased by a factor of , then output increases by an amount less than such that  .

.

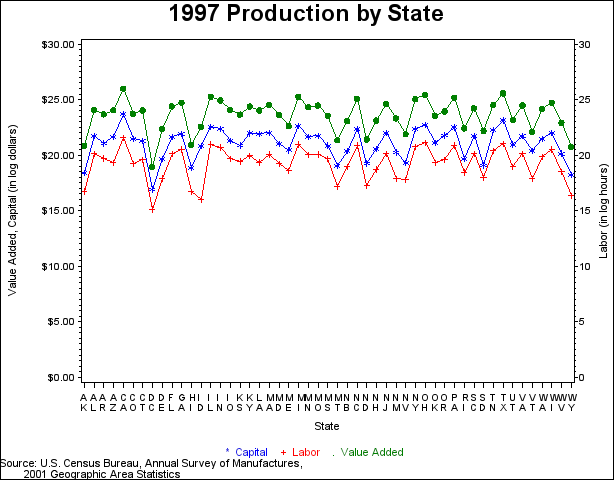

The U.S. Census Bureau conducts an Annual Survey of Manufactures in each of the four years between the economic census. This survey is broken down into each of the 50 states and the District of Colombia in the 2001 Geographic Area Statistics. The data consist of labor hours as the estimate for labor input, total capital expenditures as the estimate for capital input, and value added as the estimate for output. Labor, capital, and output data are from 1997, the most recent year for which complete data are available.

The following sections of code demonstrate how to manipulate input data into usable formats. You use PROC TRANSPOSE first to transpose the data into a form that is usable for your regression and then modify the data further to make it usable for your graph. The code for creating a graph with two vertical axes is also displayed, followed by a plot of the data in Figure 1.1.

data census_data;

input state $ type $ am;

datalines;

AL q 28762420000

AL K 2818886000

AL L 544806000

AK q 1153433000

AK K 97292000

AK L 18942000

AZ q 27900974000

AZ K 2593261000

AZ L 245413000

... more lines ...

WI L 829277000

WY q 1030583000

WY K 83569000

WY L 12209000

;

run;

** Manipulate the data for running regression and for plotting data **;

proc sort data=census_data;

by state;

run;

** reg_data is the data set you use for running the regression **;

proc transpose data=census_data out=reg_data

(rename = (Col1=q Col2=K Col3=L));

var am;

by state;

run;

data newdata;

set census_data;

lnam=log(am);

if type='q' then do;

format lnam dollar15.2;

end;

else if type='K' then do;

format lnam dollar15.2;

end;

else if type='L' then do;

delete;

end;

run;

** plot_data is the data set you use for plotting the data **;

data plot_data;

merge newdata (in=a) reg_data (in=b);

by state;

if a and b;

lnl=round(log(L),.01);

keep state type lnam lnl;

run;

** Create graph **;

proc gplot data=plot_data;

plot lnam*state=type / nolegend haxis=axis1 vaxis=axis2;

plot2 lnl*state / vaxis=axis3;

symbol1 c=blue i=join v=star;

symbol2 c=green i=join v=dot;

symbol3 c=red i=join v=plus ;

axis1 label=('State');

axis2 label=(angle=90 'Value Added, Capital (in log dollars)')

order=(0 to 30 by 5);

axis3 label=(angle=90 'Labor (in log hours)')

order=(0 to 30 by 5);

title "1997 Production by State";

footnote1 c=blue ' * Capital'

c=red ' + Labor'

c=green ' . Value Added';

footnote2 j=l 'Source: U.S. Census Bureau, Annual Survey of Manufactures,';

footnote3 j=l ' 2001 Geographic Area Statistics';

run;

quit;

title; footnote;

Figure 1.1 1997 Production by State

Analysis

Using the 1997 U.S. Census Bureau data, you can test for the three types of returns to scale based on the Cobb-Douglas production function with both F tests and t tests.

Conducting an F test for Constant Returns to Scale

In this example, you test the simplest case to determine whether the model has constant returns to scale. Beginning with the general form of the Cobb-Douglas equation, take the natural log of both sides of the equation and define the regression equation.

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

You are interested in determining whether the function exhibits constant returns to scale and test against the alternative that the returns are not constant. Hence,

|

|

|

|||

|

|

|

You can test this hypothesis using SAS by first creating the log variables, then using PROC REG to conduct an F test. Traditionally, you need to create both a full and a reduced model where the full model regresses  . The reduced model restates the hypothesis as

. The reduced model restates the hypothesis as  and substitutes the new value for

and substitutes the new value for  into the full model. Solving for the reduced model, you get the following:

into the full model. Solving for the reduced model, you get the following:

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

Thus, you perform the simple linear regression  as the reduced model using the MODEL statement.

as the reduced model using the MODEL statement.

However, PROC REG can calculate the reduced model for you by using a TEST statement. After the full model is defined, the conditions for the F test are specified in the TEST statement and SAS automatically calculates the reduced model necessary to conduct the test. In this case, the conditions you use echo the hypothesis that the sum of the betas equals zero. Note that the variable names in the TEST statement correspond to the regressors and that each variable name represents its estimated coefficient.

** Create log variables **;

data model (drop=_name_);

set reg_data;

y = log(q);

x1 = log(K);

x2 = log(L);

run;

** Run regression **;

proc reg data=model;

MODEL_1: model y = x1 x2;

F_TEST: test x1+x2=1;

run;

quit;

The results are given in two separate tables, as shown in Figure 1.2 and Figure 1.3.

Figure 1.2 Fit Statistics and Parameter Estimates

| Analysis of Variance | |||||

|---|---|---|---|---|---|

| Source | DF | Sum of Squares |

Mean Square |

F Value | Pr > F |

| Model | 2 | 102.86112 | 51.43056 | 1152.36 | <.0001 |

| Error | 48 | 2.14227 | 0.04463 | ||

| Corrected Total | 50 | 105.00339 | |||

| Root MSE | 0.21126 | R-Square | 0.9796 |

|---|---|---|---|

| Dependent Mean | 23.60251 | Adj R-Sq | 0.9787 |

| Coeff Var | 0.89507 |

| Parameter Estimates | |||||

|---|---|---|---|---|---|

| Variable | DF | Parameter Estimate |

Standard Error |

t Value | Pr > |t| |

| Intercept | 1 | 2.46466 | 0.46928 | 5.25 | <.0001 |

| x1 | 1 | 0.66876 | 0.05930 | 11.28 | <.0001 |

| x2 | 1 | 0.36535 | 0.05535 | 6.60 | <.0001 |

Figure 1.3 F test Results

| Test F_TEST Results for Dependent Variable y | ||||

|---|---|---|---|---|

| Source | DF | Mean Square |

F Value | Pr > F |

| Numerator | 1 | 0.11003 | 2.47 | 0.1230 |

| Denominator | 48 | 0.04463 | ||

In the F test results, you find a  -value of

-value of  . If the -value is less than the chosen significance level, then you reject the hypothesis in favor of the alternative. If the -value is greater than the chosen significance level, then there is insufficient evidence to reject the null hypothesis. If you assume a significance level of 0.05 for this example, then

. If the -value is less than the chosen significance level, then you reject the hypothesis in favor of the alternative. If the -value is greater than the chosen significance level, then there is insufficient evidence to reject the null hypothesis. If you assume a significance level of 0.05 for this example, then  , and you fail to reject the hypothesis. You find that the model demonstrates constant returns to scale.

, and you fail to reject the hypothesis. You find that the model demonstrates constant returns to scale.

Conducting a t test for Non-Constant Returns to Scale

If you want to perform a specific test for either increasing or decreasing returns to scale, then you need to use a one-sided t test. In the case of increasing returns, you test the following hypothesis and alternative:

|

|

|

|||

|

|

|

The case of decreasing returns works similarly. You test the following hypothesis and alternative:

|

|

|

|||

|

|

|

You use the same MODEL statement that you used in the preceding F test to conduct this t test for increasing returns to scale. However, you also ask PROC REG to return a covariance matrix by specifying the COVB option on the MODEL statement. This enables you to compute the standard error of a linear combination of parameter estimates. The necessary code and its results follow in Figure 1.4:

** t Test Regression **;

proc reg data=model;

T_TEST: model y = x1 x2 / covb;

run;

quit;

Figure 1.4 Model Results and Covariance Matrix

| Analysis of Variance | |||||

|---|---|---|---|---|---|

| Source | DF | Sum of Squares |

Mean Square |

F Value | Pr > F |

| Model | 2 | 102.86112 | 51.43056 | 1152.36 | <.0001 |

| Error | 48 | 2.14227 | 0.04463 | ||

| Corrected Total | 50 | 105.00339 | |||

| Root MSE | 0.21126 | R-Square | 0.9796 |

|---|---|---|---|

| Dependent Mean | 23.60251 | Adj R-Sq | 0.9787 |

| Coeff Var | 0.89507 |

| Parameter Estimates | |||||

|---|---|---|---|---|---|

| Variable | DF | Parameter Estimate |

Standard Error |

t Value | Pr > |t| |

| Intercept | 1 | 2.46466 | 0.46928 | 5.25 | <.0001 |

| x1 | 1 | 0.66876 | 0.05930 | 11.28 | <.0001 |

| x2 | 1 | 0.36535 | 0.05535 | 6.60 | <.0001 |

| Covariance of Estimates | |||

|---|---|---|---|

| Variable | Intercept | x1 | x2 |

| Intercept | 0.2202250596 | -0.015334657 | 0.0054015337 |

| x1 | -0.015334657 | 0.0035162514 | -0.003054157 |

| x2 | 0.0054015337 | -0.003054157 | 0.0030639604 |

You construct the t statistic using the results such that

|

|

|

You construct the t statistic using the results such that

|

|

|

where the standard error (se) of the parameter estimates,  , is computed as

, is computed as

|

|

|

by using the results in the covariance matrix.

You can either compute the t statistic by hand, using the results in the ANOVA table and the preceding equation, or you can use an OUTEST statement in PROC REG to achieve the same result. The following code demonstrates how to use the OUTEST statement and its results in Figure 1.5.

** t Test Regression with OUTEST statement **;

proc reg data=model outest=est covout edf;

T_TEST_OUT: model y = x1 x2 / covb;

run;

quit;

** Calculate t statistic**;

** Keep the parameter estimates, error degrees of freedom, **;

** variances, and covariance **;

data parms;

set est (where=(_type_='PARMS'));

keep x1 x2 _edf_;

run;

data varx1;

set est (where=(_name_='x1'));

varx1=x1;

covx1x2=x2;

keep varx1 covx1x2;

run;

data varx2;

set est (where=(_name_='x2'));

varx2=x2;

keep varx2;

run;

** Calculate the standard error for the denominator, **;

** the t statistic, and the p-values **;

data ttest;

merge parms varx1 varx2;

se_x1x2 = sqrt(varx1 + varx2 + (2*covx1x2));

t = (x1 + x2 - 1)/se_x1x2;

p_inc = 1 - probt(t,_edf_);

p_dec = probt(t,_edf_);

run;

** Print and view the results **;

proc print data=ttest;

var t _edf_ p_inc p_dec;

title "t statistic and p-values for model";

run;

Figure 1.5 Model Results

| t statistic and p-values for model |

| Obs | t | _EDF_ | p_inc | p_dec |

|---|---|---|---|---|

| 1 | 1.57014 | 48 | 0.061476 | 0.93852 |

As with the F test, you compare the -values with your chosen level of significance. Assuming a significance level of 0.05, you compare the -value for increasing returns to scale. If the -value is greater than the chosen significance level, then there is insufficient evidence to reject the null hypothesis. Since  , you fail to reject the hypothesis. Similarly, you compare the -value for decreasing returns to scale to your chosen level of significance. Since

, you fail to reject the hypothesis. Similarly, you compare the -value for decreasing returns to scale to your chosen level of significance. Since  , you fail to reject the hypothesis. The model is clearly demonstrating constant returns to scale.

, you fail to reject the hypothesis. The model is clearly demonstrating constant returns to scale.

References

-

Mendenhall, William and Terry Sincich (2003), A Second Course in Statistics: Regression Analysis, Sixth Edition, New Jersey: Pearson Education Inc.

-

Nicholson, W. (1992), Microeconomic Theory: Basic Principles and Extensions, Fifth Edition, Fort Worth: Dryden Press.

-

U.S. Census Bureau (2003), "Annual Survey of Manufactures, 2001 Geographic Area Statistics," http://www.census.gov/mcd/asm-as3.html.

-

Wooldridge, Jeffrey M. (2003), Introductory Econometrics: A Modern Approach, Second Edition, Ohio: South-Western.

-

Zellner, Arnold (1971), An Introduction to Bayesian Inference in Econometrics, New York: Wiley.

These sample files and code examples are provided by SAS Institute Inc. "as is" without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability and fitness for a particular purpose. Recipients acknowledge and agree that SAS Institute shall not be liable for any damages whatsoever arising out of their use of this material. In addition, SAS Institute will provide no support for the materials contained herein.

ata census_data;

input state $ type $ am;

datalines;

AL q 28762420000

AL K 2818886000

AL L 544806000

AK q 1153433000

AK K 97292000

AK L 18942000

AZ q 27900974000

AZ K 2593261000

AZ L 245413000

AR q 19392561000

AR K 1410061000

AR L 367624000

CA q 196182882000

CA K 19628560000

CA L 2296334000

CO q 20609367000

CO K 2083882000

CO L 224728000

CT q 27298479000

CT K 1783242000

CT L 315068000

DE q 5209618000

DE K 352875000

DE L 59829000

DC q 170633000

DC K 22435000

DC L 3714000

FL q 39767726000

FL K 2506475000

FL L 555402000

GA q 55426485000

GA K 3408828000

GA L 826574000

HI q 1261303000

HI K 157221000

HI L 18343000

ID q 6383900000

ID K 1157786000

ID L 9069000

IL q 95342475000

IL K 6357175000

IL L 1278831000

IN q 67173341000

IN K 5272833000

IN L 978646000

IO q 28615467000

IO K 1804159000

IO L 356074000

KS q 18987474000

KS K 1178162000

KS L 280314000

KY q 39062786000

KY K 3499977000

KY L 455748000

LA q 27463050000

LA K 3259885000

LA L 256824000

ME q 6698567000

ME K 755909000

ME L 120642000

MD q 18705455000

MD K 1333239000

MD L 218330000

MA q 45132888000

MA K 3615304000

MA L 520200000

MI q 93366860000

MI K 6981199000

MI L 1299481000

MN q 36567010000

MN K 2579422000

MN L 513688000

MS q 17184299000

MS K 1169221000

MS L 360610000

MO q 43071878000

MO K 2834926000

MO L 526652000

MT q 1876897000

MT K 191380000

MT L 27386000

NB q 10460265000

NB K 697928000

NB L 172999000

NV q 3260969000

NV K 249037000

NV L 51573000

NH q 11129674000

NH K 854626000

NH L 134236000

NJ q 49432983000

NJ K 3644389000

NJ L 555738000

NM q 13487517000

NM K 630512000

NM L 56972000

NY q 75858926000

NY K 5074888000

NY L 1049318000

NC q 79790807000

NC K 5207500000

NC L 1192012000

ND q 2008799000

ND K 233693000

ND L 31447000

OH q 112361392000

OH K 7364383000

OH L 1494596000

OK q 17226649000

OK K 1495963000

OK L 241863000

OR q 25100453000

OR K 2899991000

OR L 314114000

PA q 86116509000

PA K 6024692000

PA L 1187997000

RI q 5462493000

RI K 350655000

RI L 103787000

SC q 33343682000

SC K 2769701000

SC L 536612000

SD q 4352357000

SD K 194857000

SD L 64773000

TN q 44527758000

TN K 4620591000

TN L 741421000

TX q 127579894000

TX K 11247496000

TX L 1340712000

UT q 11689959000

UT K 1281331000

UT L 169255000

VT q 4028276000

VT K 714803000

VT L 57719000

VA q 43180687000

VA K 2702950000

VA L 549218000

WA q 31534413000

WA K 2173424000

WA L 424129000

WV q 8980535000

WV K 570564000

WV L 112022000

WI q 54974219000

WI K 3710392000

WI L 829277000

WY q 1030583000

WY K 83569000

WY L 12209000

;

run;

** Manipulate the data for running regression and for plotting data **;

proc sort data=census_data;

by state;

run;

** reg_data is the data set you use for running the regression **;

proc transpose data=census_data out=reg_data

(rename = (Col1=q Col2=K Col3=L));

var am;

by state;

run;

data newdata;

set census_data;

lnam=log(am);

if type='q' then do;

format lnam dollar15.2;

end;

else if type='K' then do;

format lnam dollar15.2;

end;

else if type='L' then do;

delete;

end;

run;

** plot_data is the data set you use for plotting the data **;

data plot_data;

merge newdata (in=a) reg_data (in=b);

by state;

if a and b;

lnl=round(log(L),.01);

keep state type lnam lnl;

run;

** Create graph **;

proc gplot data=plot_data;

plot lnam*state=type / nolegend haxis=axis1 vaxis=axis2;

plot2 lnl*state / vaxis=axis3;

symbol1 c=blue i=join v=star;

symbol2 c=green i=join v=dot;

symbol3 c=red i=join v=plus ;

axis1 label=('State');

axis2 label=(angle=90 'Value Added, Capital (in log dollars)')

order=(0 to 30 by 5);

axis3 label=(angle=90 'Labor (in log hours)')

order=(0 to 30 by 5);

title "1997 Production by State";

footnote1 c=blue ' * Capital'

c=red ' + Labor'

c=green ' . Value Added';

footnote2 j=l 'Source: U.S. Census Bureau, Annual Survey of Manufactures,';

footnote3 j=l ' 2001 Geographic Area Statistics';

run;

quit;

title; footnote;

** Create log variables **;

data model (drop=_name_);

set reg_data;

y = log(q);

x1 = log(K);

x2 = log(L);

run;

** Run regression **;

proc reg data=model;

MODEL_1: model y = x1 x2;

F_TEST: test x1+x2=1;

run;

quit;

** t Test Regression **;

proc reg data=model;

T_TEST: model y = x1 x2 / covb;

run;

quit;

** t Test Regression with OUTEST statement **;

proc reg data=model outest=est covout edf;

T_TEST_OUT: model y = x1 x2 / covb;

run;

quit;

** Calculate t statistic**;

** Keep the parameter estimates, error degrees of freedom, **;

** variances, and covariance **;

data parms;

set est (where=(_type_='PARMS'));

keep x1 x2 _edf_;

run;

data varx1;

set est (where=(_name_='x1'));

varx1=x1;

covx1x2=x2;

keep varx1 covx1x2;

run;

data varx2;

set est (where=(_name_='x2'));

varx2=x2;

keep varx2;

run;

** Calculate the standard error for the denominator, **;

** the t statistic, and the p-values **;

data ttest;

merge parms varx1 varx2;

se_x1x2 = sqrt(varx1 + varx2 + (2*covx1x2));

t = (x1 + x2 - 1)/se_x1x2;

p_inc = 1 - probt(t,_edf_);

p_dec = probt(t,_edf_);

run;

** Print and view the results **;

proc print data=ttest;

var t _edf_ p_inc p_dec;

title "t statistic and p-values for model";

run;

These sample files and code examples are provided by SAS Institute Inc. "as is" without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability and fitness for a particular purpose. Recipients acknowledge and agree that SAS Institute shall not be liable for any damages whatsoever arising out of their use of this material. In addition, SAS Institute will provide no support for the materials contained herein.

| Type: | Sample |

| Date Modified: | 2017-08-01 12:43:45 |

| Date Created: | 2017-08-01 10:03:56 |

Operating System and Release Information

| Product Family | Product | Host | SAS Release | |

| Starting | Ending | |||

| SAS System | SAS/ETS | z/OS | ||

| z/OS 64-bit | ||||

| OpenVMS VAX | ||||

| Microsoft® Windows® for 64-Bit Itanium-based Systems | ||||

| Microsoft Windows Server 2003 Datacenter 64-bit Edition | ||||

| Microsoft Windows Server 2003 Enterprise 64-bit Edition | ||||

| Microsoft Windows XP 64-bit Edition | ||||

| Microsoft® Windows® for x64 | ||||

| OS/2 | ||||

| Microsoft Windows 8 Enterprise 32-bit | ||||

| Microsoft Windows 8 Enterprise x64 | ||||

| Microsoft Windows 8 Pro 32-bit | ||||

| Microsoft Windows 8 Pro x64 | ||||

| Microsoft Windows 8.1 Enterprise 32-bit | ||||

| Microsoft Windows 8.1 Enterprise x64 | ||||

| Microsoft Windows 8.1 Pro 32-bit | ||||

| Microsoft Windows 8.1 Pro x64 | ||||

| Microsoft Windows 10 | ||||

| Microsoft Windows 95/98 | ||||

| Microsoft Windows 2000 Advanced Server | ||||

| Microsoft Windows 2000 Datacenter Server | ||||

| Microsoft Windows 2000 Server | ||||

| Microsoft Windows 2000 Professional | ||||

| Microsoft Windows NT Workstation | ||||

| Microsoft Windows Server 2003 Datacenter Edition | ||||

| Microsoft Windows Server 2003 Enterprise Edition | ||||

| Microsoft Windows Server 2003 Standard Edition | ||||

| Microsoft Windows Server 2003 for x64 | ||||

| Microsoft Windows Server 2008 | ||||

| Microsoft Windows Server 2008 R2 | ||||

| Microsoft Windows Server 2008 for x64 | ||||

| Microsoft Windows Server 2012 Datacenter | ||||

| Microsoft Windows Server 2012 R2 Datacenter | ||||

| Microsoft Windows Server 2012 R2 Std | ||||

| Microsoft Windows Server 2012 Std | ||||

| Microsoft Windows XP Professional | ||||

| Windows 7 Enterprise 32 bit | ||||

| Windows 7 Enterprise x64 | ||||

| Windows 7 Home Premium 32 bit | ||||

| Windows 7 Home Premium x64 | ||||

| Windows 7 Professional 32 bit | ||||

| Windows 7 Professional x64 | ||||

| Windows 7 Ultimate 32 bit | ||||

| Windows 7 Ultimate x64 | ||||

| Windows Millennium Edition (Me) | ||||

| Windows Vista | ||||

| Windows Vista for x64 | ||||

| 64-bit Enabled AIX | ||||

| 64-bit Enabled HP-UX | ||||

| 64-bit Enabled Solaris | ||||

| ABI+ for Intel Architecture | ||||

| AIX | ||||

| HP-UX | ||||

| HP-UX IPF | ||||

| IRIX | ||||

| Linux | ||||

| Linux for x64 | ||||

| Linux on Itanium | ||||

| OpenVMS Alpha | ||||

| OpenVMS on HP Integrity | ||||

| Solaris | ||||

| Solaris for x64 | ||||

| Tru64 UNIX | ||||