Sample 60852: A Specification Test for Non-Nested Regression Models

|  |  |  |

Overview

|

In econometrics, researchers are constantly faced with the fundamental problem of choosing between models. The seminal contributions of Cox (1961) to the testing of separate families of hypotheses and Pesaran (1974) to the testing of non-nested linear regressions have lead to a burgeoning literature on the testing for non-nested models. As McAleer (1995) points out, prior to 1982, there were only about 15 published papers testing non-nested regression models. Over the last decade, however, more than 100 papers have been published.

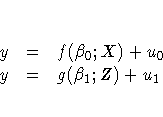

Consider the following two models (refer to Pesaran and Deaton 1978):

where y is an (nT)x1 vector of observations on all the n dependent variables, f(·) and g(·) are the corresponding vectors of predictions, u0 and u1, of errors, and X and Z are matrices of predetermined variables. As seen above, f(·) is not nested within g(·) and vice versa. A solution consists in nesting f(·) within more general models in which the variables Z appear explicitly as exogenous or endogenous variables.

One particular way of choosing between the two hypotheses is the J-test, suggested by Davidson and Mackinnon (1981). Estimate the comprehensive model

note that ![]() is refered to as the mixing parameter hereafter). When no a priori information is available, the mixing parameter is not identifiable in the comprehensive model. The J-test works around this by replacing g(·) with the fitted values from a regression of y on Z and testing the mixing parameter for statistical significance.

is refered to as the mixing parameter hereafter). When no a priori information is available, the mixing parameter is not identifiable in the comprehensive model. The J-test works around this by replacing g(·) with the fitted values from a regression of y on Z and testing the mixing parameter for statistical significance.

This example illustrates a way to test the specification of a consumption function. The extension of this example to other non-nested models and multiple hypotheses is straightforward.

Analysis

This example illustrates a specification problem in analyzing the relationship between consumption and income using U.S. quarterly data. One simple model postulates a linear relationship between consumption, income, and wealth; the influence of lagged income operates through the wealth term. Denoting consumption by c, income by y, and wealth by w, you postulate

where ut denotes a normally distributed disturbance vector.

An alternative is to estimate an equation containing lagged consumption as an explanatory variable. This can be thought of as a variant of Duesenberry's (1949) relative income hypothesis. The model can be postulated as

As seen above, the H1 and H2 models are non-nested.

The comprehensive models

and

where ![]() and

and ![]() are the coefficients of the fitted values under H1 and H2, respectively, are both estimated. The J-test is applied by testing the mixing parameter,

are the coefficients of the fitted values under H1 and H2, respectively, are both estimated. The J-test is applied by testing the mixing parameter, ![]() , for significance in each model.

, for significance in each model.

The data set consists of seasonally adjusted quarterly time series of real 1958 prices, consumers' expenditure on non-durable goods and personal disposable income. These were collected from the Survey of Current Business and are used by Pesaran and Deaton (1978).

data spec;

input yr qr c y w;

c_lag=lag(c);

date = yyq( yr, qr );

format date yyqc.;

datalines;

1954 2 253 270 0

1954 3 257 274 17

1954 4 262 279 34

1955 1 268 282 51

...

;

run;

Before the J-test can be performed, the fitted values from the two models must be calculated. The AUTOREG procedure can fit several different regressions with the inclusion of multiple model statements. In this example, two model statements are used, corresponding to the two hypotheses. For each MODEL statement an output data set is created with the OUT= option. These data sets contain the predicted values CHAT1 and CHAT2, as specified by the P= option. The DATA step merges the original data set with the two predicted data sets for use in the J-test.

proc autoreg data=spec ;

model c = y w; /* model for H1 */

output out=model1 p=chat1;

model c = y c_lag; /* model for H2 */

output out=model2 p=chat2;

run;

data spec2;

set spec ;

set model1;

set model2;

Because of the limits of the J-test, it is often wise to test twice for the significance of the mixing parameter by reversing the roles of the hypotheses. The AUTOREG procedure estimates the two comprehensive models. The coefficients of CHAT1 and CHAT2 correspond to a test of the significance of the mixing parameter, ![]() . To reject a model requires that the mixing parameter be insignificantly different from 0.

. To reject a model requires that the mixing parameter be insignificantly different from 0.

proc autoreg data=spec2;

model c = y c_lag chat1;

model c = y w chat2;

run;

The first comprehensive model yields the following parameter estimates:

|

|

The estimate for ![]() is 1.0185 with a p-value of 0.0001. As it is highly significant and statistically indistinguishable from 1, it provides further support to the previous conclusion that H1 should be rejected in favor of H2.

is 1.0185 with a p-value of 0.0001. As it is highly significant and statistically indistinguishable from 1, it provides further support to the previous conclusion that H1 should be rejected in favor of H2.

References

Cox, D.R. (1961), ``Tests of Separate Families of Hypotheses," Proceedings of the Fourth Berkeley Symposium on Mathematical Statistics and Probability, 1, Berkeley: University of California Press.

Davidson and Mackinnon (1981), ``Several Tests for Model Specification in the Presence of Alternative Hypotheses," Econometrica, 49, 781-793.

Duesenberry, J.S. (1949), Income, Saving, and the Theory of Consumer Behavior, Cambridge, MA: Harvard University Press.

Greene, W.H. (1993), Econometric Analysis, Second Edition, New York: Macmillan Publishing Company.

McAleer M. (1995), ``The Significance of Testing Empirical Non-nested Models," Journal of Econometrics, 67, 150-171.

Pesaran, M.H. (1974), ``On the General Problem of Model Selection," Review of Economic Studies, 41, 153-171.

Pesaran, M.H. and Deaton, A.S. (1978), ``Testing Non-nested Nonlinear Regression Models," Econometrica, 46, 677-694.

SAS Institute Inc. (1993), SAS/ETS Users's Guide, Version 6, Second Edition, Cary, NC: SAS Institute Inc.

Stone, J.R.E. (1973), ``Personal Spending and Saving in Post-War Britain," in Economic Structure and Development: Essays in Honour of Jan Tinbergen, eds. H.C. Bos, H. Linnemann, and P. De Wolff, Amsterdam: North Holland, 79-98.

These sample files and code examples are provided by SAS Institute Inc. "as is" without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability and fitness for a particular purpose. Recipients acknowledge and agree that SAS Institute shall not be liable for any damages whatsoever arising out of their use of this material. In addition, SAS Institute will provide no support for the materials contained herein.

/* A Specification Test for Non-Nested Models */

data spec;

input yr qr c y w;

c_lag=lag(c);

date = yyq( yr, qr );

format date yyqc.;

datalines;

1954 2 253 270 0

1954 3 257 274 17

1954 4 262 279 34

1955 1 268 282 51

1955 2 273 289 66

1955 3 276 294 82

1955 4 280 299 100

1956 1 280 300 118

1956 2 280 302 138

1956 3 281 303 160

1956 4 285 308 182

1957 1 287 308 205

1957 2 287 309 226

1957 3 289 311 249

1957 4 290 310 271

1958 1 286 307 291

1958 2 288 308 312

1958 3 292 315 333

1958 4 295 319 356

1959 1 302 323 380

1959 2 307 328 401

1959 3 310 326 422

1959 4 310 328 437

1960 1 314 332 455

1960 2 318 334 473

1960 3 316 334 489

1960 4 316 332 507

1961 1 316 334 522

1961 2 320 340 540

1961 3 324 345 559

1961 4 330 352 581

1962 1 333 355 603

1962 2 336 359 624

1962 3 340 360 647

1962 4 345 363 667

1963 1 349 367 685

1963 2 351 369 703

1963 3 356 374 721

1963 4 358 379 739

1964 1 366 387 760

1964 2 371 397 781

1964 3 379 402 807

1964 4 379 407 830

1965 1 388 411 858

1965 2 393 416 881

1965 3 400 430 904

1965 4 409 438 933

1966 1 415 442 962

1966 2 415 443 989

1966 3 421 450 1017

1966 4 421 454 1045

1967 1 424 459 1079

1967 2 430 463 1114

1967 3 432 468 1147

1967 4 434 472 1183

1968 1 445 480 1220

1968 2 448 486 1255

1968 3 458 488 1293

1968 4 460 491 1323

1969 1 466 492 1354

1969 2 469 496 1381

1969 3 470 504 1408

1969 4 472 508 1442

1970 1 474 511 1478

1970 2 478 522 1514

1970 3 481 528 1559

1970 4 478 524 1605

1971 1 490 535 1652

1971 2 494 541 1697

1971 3 498 542 1744

1971 4 504 547 1789

1972 1 513 552 1832

1972 2 523 559 1871

1972 3 531 567 1906

1972 4 542 584 1942

1973 1 553 599 1984

1973 2 554 602 2030

1973 3 555 605 2078

1973 4 546 606 2128

1974 1 540 594 2187

1974 2 543 587 2242

1974 3 547 587 2286

;

run;

proc autoreg data=spec ;

model c = y w;

output out=model1 p=chat1;

model c = y c_lag;

output out=model2 p=chat2;

run;

data spec2;

set spec ;

set model1;

set model2;

run;

proc autoreg data=spec2;

model c = y c_lag chat1;

model c = y w chat2;

run;

quit;

proc gplot data=spec;

plot y*date c*date / overlay cframe=ligr

haxis=axis1 vaxis=axis2;

title 'Time-Series Plots';

title2 'Income and Consumption';

footnote1 c=blue ' --- Income'

c=red ' --- Consumption';

symbol1 c=blue i=join v=star;

symbol2 c=red i=join v=circle;

axis1 label=none;

axis2 label=none;

run;

quit;

These sample files and code examples are provided by SAS Institute Inc. "as is" without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability and fitness for a particular purpose. Recipients acknowledge and agree that SAS Institute shall not be liable for any damages whatsoever arising out of their use of this material. In addition, SAS Institute will provide no support for the materials contained herein.

| Type: | Sample |

| Date Modified: | 2017-08-01 09:58:54 |

| Date Created: | 2017-07-31 15:26:48 |

Operating System and Release Information

| Product Family | Product | Host | SAS Release | |

| Starting | Ending | |||

| SAS System | SAS/ETS | z/OS | ||

| z/OS 64-bit | ||||

| OpenVMS VAX | ||||

| Microsoft® Windows® for 64-Bit Itanium-based Systems | ||||

| Microsoft Windows Server 2003 Datacenter 64-bit Edition | ||||

| Microsoft Windows Server 2003 Enterprise 64-bit Edition | ||||

| Microsoft Windows XP 64-bit Edition | ||||

| Microsoft® Windows® for x64 | ||||

| OS/2 | ||||

| Microsoft Windows 8 Enterprise 32-bit | ||||

| Microsoft Windows 8 Enterprise x64 | ||||

| Microsoft Windows 8 Pro 32-bit | ||||

| Microsoft Windows 8 Pro x64 | ||||

| Microsoft Windows 8.1 Enterprise 32-bit | ||||

| Microsoft Windows 8.1 Enterprise x64 | ||||

| Microsoft Windows 8.1 Pro 32-bit | ||||

| Microsoft Windows 8.1 Pro x64 | ||||

| Microsoft Windows 10 | ||||

| Microsoft Windows 95/98 | ||||

| Microsoft Windows 2000 Advanced Server | ||||

| Microsoft Windows 2000 Datacenter Server | ||||

| Microsoft Windows 2000 Server | ||||

| Microsoft Windows 2000 Professional | ||||

| Microsoft Windows NT Workstation | ||||

| Microsoft Windows Server 2003 Datacenter Edition | ||||

| Microsoft Windows Server 2003 Enterprise Edition | ||||

| Microsoft Windows Server 2003 Standard Edition | ||||

| Microsoft Windows Server 2003 for x64 | ||||

| Microsoft Windows Server 2008 | ||||

| Microsoft Windows Server 2008 R2 | ||||

| Microsoft Windows Server 2008 for x64 | ||||

| Microsoft Windows Server 2012 Datacenter | ||||

| Microsoft Windows Server 2012 R2 Datacenter | ||||

| Microsoft Windows Server 2012 R2 Std | ||||

| Microsoft Windows Server 2012 Std | ||||

| Microsoft Windows XP Professional | ||||

| Windows 7 Enterprise 32 bit | ||||

| Windows 7 Enterprise x64 | ||||

| Windows 7 Home Premium 32 bit | ||||

| Windows 7 Home Premium x64 | ||||

| Windows 7 Professional 32 bit | ||||

| Windows 7 Professional x64 | ||||

| Windows 7 Ultimate 32 bit | ||||

| Windows 7 Ultimate x64 | ||||

| Windows Millennium Edition (Me) | ||||

| Windows Vista | ||||

| Windows Vista for x64 | ||||

| 64-bit Enabled AIX | ||||

| 64-bit Enabled HP-UX | ||||

| 64-bit Enabled Solaris | ||||

| ABI+ for Intel Architecture | ||||

| AIX | ||||

| HP-UX | ||||

| HP-UX IPF | ||||

| IRIX | ||||

| Linux | ||||

| Linux for x64 | ||||

| Linux on Itanium | ||||

| OpenVMS Alpha | ||||

| OpenVMS on HP Integrity | ||||

| Solaris | ||||

| Solaris for x64 | ||||

| Tru64 UNIX | ||||