Sample 59779: Calculating Price Elasticity of Demand

|  |  |  |

Overview

|

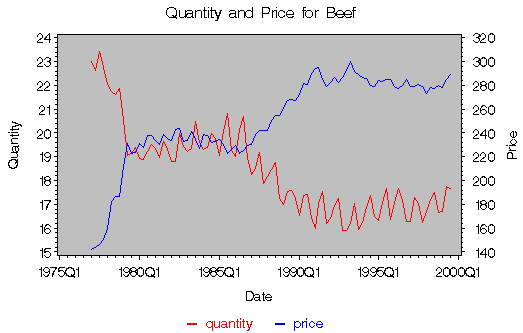

Figure 1: Quantity and Price for Beef

The price elasticity of demand is defined as the percentage change in quantity demanded for some good with respect to a one percent change in the price of the good. For example, if the price of some good goes up by 1%, and as a result sales fall by 1.5%, the price elasticity of demand for this good is -1.5%/1% = -1.5. Thus, price elasticity measures responsiveness of quantity demanded to changes in price. Price elasticity greater than one is called price elastic, and price elasticity less than one is called price inelastic. A given percentage increase in the price of an elastic good will reduce the quantity demanded for the good by a higher percentage than for an inelastic good. In general, a necessary good is less elastic than a luxury good. For an introductory text on price elasticities, see Nicholson (1992). Price elasticity can be expressed as:

where ![]() is the price elasticity,

P is the price of the good, and Q is the quantity

demanded for the good.

is the price elasticity,

P is the price of the good, and Q is the quantity

demanded for the good.

Analysis

In this example, you will calculate the price elasticity of demand for beef in a simple log-linear demand model. The data consist of quarterly retail prices and per capita consumption for beef. The data period covers the first quarter of 1977 through the third quarter of 1999. The data were obtained from the USDA Red Meats Yearbook (accessed 2001).

The log-linear demand model is of the following form:

- lnQ = a + b·lnP

where Q and P are defined as before, a and b are parameters to be estimated.

The log-linear demand model is a very simple one. In the real world, there may be many additional complexities that need to be considered in the model. For example, prices of some other closely related goods may have a significant effect on the quantity demanded for beef; hence, they may also enter the right-hand side of the demand equation. On a store level, there may also be occasions when sales remain zero regardless of how much the price is; for example, when the good is out of stock. For demonstration purposes these complexities will be ignored.

The log-linear demand function implies that the price elasticity of demand is constant:

Thus, to obtain an estimate of the price elasticity, you just need an estimate of b. You can use the AUTOREG procedure to obtain the estimates.

To use the AUTOREG procedure, you first read in the price and quantity data in the DATA step, and transform the price and quantity data into log forms:

data a ;

input yr qtr q p ;

date = yyq(yr,qtr) ;

format date yyq6. ;

lq = log(q) ;

lp = log(p) ;

datalines;

1977 1 22.9976 142.1667

1977 2 22.6131 143.9333

1977 3 23.4054 146.5

1977 4 22.7401 150.8

1978 1 22.0441 160

... more datalines ...

1997 4 16.2354 279.3

1998 1 16.6884 273.4667

1998 2 17.1985 278.1

1998 3 17.5085 277.3667

1998 4 16.6475 279.5333

1999 1 16.6785 278

1999 2 17.7635 284.7667

1999 3 17.6689 289.2333

;

run ;

Then you specify the input data set in the PROC AUTOREG statement and specify the regression model in a MODEL statement. If you are not concerned with autocorrelated errors and just want to do an ordinary least-squares regression, you can specify the model as follows:

proc autoreg data=a outest=estb ;

model lq = lp ;

output out=out1 r=resid1 ;

title "OLS Estimates";

run ;

This will yield ordinary least squares estimates of a and b. The output is shown in Figure 2.

Figure 2: OLS EsimatesThe parameter estimate for b is equal to -0.5314, which suggests that increasing the price for beef by 1% will reduce the demand for beef by 0.53%.

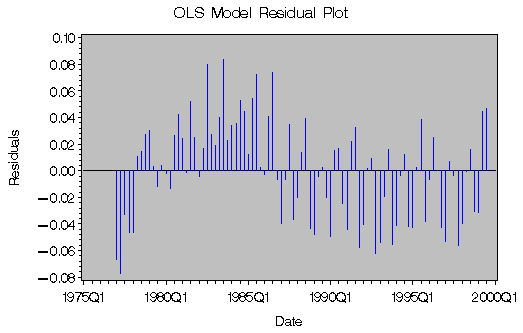

The following SAS code uses the GPLOT procedure to plot the residuals obtained from the OLS estimation, as shown in Figure 3.

proc gplot data=plot2 ;

title 'OLS Model Residual Plot' ;

axis1 label=(angle=90 'Residuals') ;

axis2 label=('Date') ;

symbol1 c=blue i=needle v=none ;

plot resid1*date / cframe=ligr haxis=axis2 vaxis=axis1 ;

run ;

|

Figure 3: OLS Model Residual Plot

Note that the residual errors from the OLS regression do not appear to be random. The residual plot shows evidence of autocorrelation in the error process. This violates the independent error assumption of the classical regression model, and the OLS estimates will be inefficient. Thus, the parameter estimates are not as accurate as they could be.

To improve the efficiency of the estimated parameters, you can correct for autocorrelation using the AUTOREG procedure. Specify the order of autocorrelation using the NLAG= option. Since the data are quarterly, this example chooses order 1 as well as order 4 for seasonality considerations. You can use the METHOD= option to specify the maximum likelihood estimation.

proc autoreg data=a outest=estb ;

model lq = lp / nlag=(1 4) method=ml ;

output out=out2 r=resid2 ;

title "OLS, Autocorrelations, & Maximum Likelihood Estimates";

run ;

The output in Figure 4 first shows the initial OLS results. Then the estimates of autocorrelations and the maximum likelihood estimates are displayed.

The AUTOREG Procedure

The AUTOREG Procedure

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

By including an autoregressive error structure in the model, the total R2 statistic increases from 0.8521 to 0.9422 in the maximum likelihood estimation. The information criteria AIC and SBC become more negative. These imply significant improvement over the OLS estimation.

Notice also that the estimate for b changes from -0.5314 to -0.4131, which means that the estimated elasticity for beef demand is smaller in absolute value than the OLS estimate. Since the estimated elasticity is smaller than 1 in absolute value, you may conclude that demand for beef is relatively inelastic.

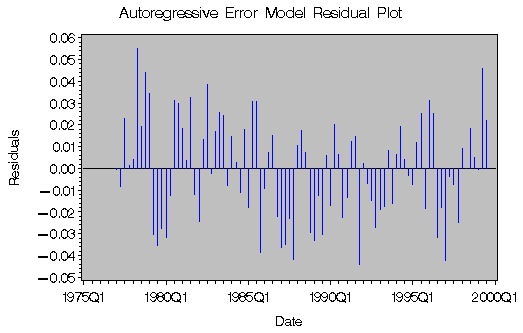

Figure 5 illustrates the residuals obtained from the autoregressive error model estimation.

proc gplot data=plot2 ;

title 'Autoregressive Error Model Residual Plot' ;

axis1 label=(angle=90 'Residuals') ;

axis2 label=('Date') ;

symbol1 c=blue i=needle v=none ;

plot resid2*date / cframe=ligr haxis=axis2 vaxis=axis1 ;

run ;

|

Figure 5: Autoregressive Error Model Residual Plot

References

Nicholson, W. (1992), Microeconomic Theory: Basic Principles and Extensions, Fifth Edition, Fort Worth: Dryden Press.

SAS Institute Inc. (1999), SAS/ETS User's Guide, Version 8, Cary, NC: SAS Institute Inc.

USDA-ERS Electronic Data Archive, Red Meats Yearbook, housed at Cornell University's Mann Library, [http://usda.mannlib.cornell.edu/], accessed 25 September 2001.

These sample files and code examples are provided by SAS Institute Inc. "as is" without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability and fitness for a particular purpose. Recipients acknowledge and agree that SAS Institute shall not be liable for any damages whatsoever arising out of their use of this material. In addition, SAS Institute will provide no support for the materials contained herein.

/*-----------------------------------------------------------------

Example: Calculating Price Elasticity of Demand

Requires: SAS/ETS, SAS/IML

Version: 9.0

------------------------------------------------------------------*/

data a ;

input yr qtr q p ;

date = yyq(yr,qtr) ;

format date yyq6. ;

lq = log(q) ;

lp = log(p) ;

datalines;

1977 1 22.9976 142.1667

1977 2 22.6131 143.9333

1977 3 23.4054 146.5

1977 4 22.7401 150.8

1978 1 22.0441 160

1978 2 21.7602 182.5333

1978 3 21.6064 186.2

1978 4 21.8814 186.4333

1979 1 20.5086 211.7

1979 2 19.0408 231.5

1979 3 19.1457 222.7

1979 4 19.3989 223.8333

1980 1 18.947 231.1667

1980 2 18.898 227.5

1980 3 19.2127 237.5333

1980 4 19.4988 238.1667

1981 1 19.3429 233.5

1981 2 18.9816 230.7

1981 3 19.6459 239.0333

1981 4 19.2868 235.4333

1982 1 18.8193 233.3

1982 2 18.7968 242.9667

1982 3 19.9882 244.0333

1982 4 19.4242 233.1333

1983 1 19.2252 233.8667

1983 2 19.3361 240.9333

1983 3 20.4952 234.3667

1983 4 19.5995 227.1667

1984 1 19.3191 238.4667

1984 2 19.3744 238

1984 3 19.9738 232.2

1984 4 19.7597 233.2333

1985 1 19.0586 234.9

1985 2 20.0757 230.4333

1985 3 20.8175 222.7333

1985 4 19.2488 226.4333

1986 1 19.0212 229.2667

1986 2 20.1607 222.9

1986 3 20.7108 225.6333

1986 4 18.9416 229.3

1987 1 18.2746 230.6

1987 2 18.5266 239.1

1987 3 19.175 242.1667

1987 4 17.8807 241.6667

1988 1 18.1678 241.7333

1988 2 18.4639 250.1

1988 3 18.7622 254.5333

1988 4 17.2552 255

1989 1 16.9765 260.7

1989 2 17.5192 266.9667

1989 3 17.5975 268.0333

1989 4 17.2416 266.9333

1990 1 16.5516 272.6333

1990 2 17.3763 281.2

1990 3 17.4207 280.3667

1990 4 16.4315 289.8667

1991 1 15.9842 294.2667

1991 2 17.0449 295.2

1991 3 17.5591 284.6333

1991 4 16.2093 279.2

1992 1 16.3952 282.2667

1992 2 16.9538 286.8333

1992 3 17.227 282.6667

1992 4 15.9093 286.6667

1993 1 15.8915 292.1333

1993 2 16.2058 300.4

1993 3 17.043 292

1993 4 15.9513 289.2333

1994 1 16.2494 286.6667

1994 2 16.8868 286.1667

1994 3 17.3775 279.5

1994 4 16.4723 279.1667

1995 1 16.3097 283.8667

1995 2 17.0895 283.1

1995 3 17.647 285.1

1995 4 16.3476 285.2667

1996 1 17.0783 278.7

1996 2 17.6763 277.4

1996 3 17.1606 279.8

1996 4 16.2764 285.0333

1997 1 16.2921 278.8

1997 2 17.2994 278.9667

1997 3 17.0513 281.0667

1997 4 16.2354 279.3

1998 1 16.6884 273.4667

1998 2 17.1985 278.1

1998 3 17.5085 277.3667

1998 4 16.6475 279.5333

1999 1 16.6785 278

1999 2 17.7635 284.7667

1999 3 17.6689 289.2333

;

run ;

proc autoreg data=a outest=estb ;

model lq = lp ;

output out=out1 r=resid1 ;

title "OLS Estimates";

run ;

proc autoreg data=a outest=estb ;

model lq = lp / nlag=(1 4) method=ml ;

output out=out2 r=resid2 ;

title "OLS, Autocorrelations, & ML";

run ;

data plot2 ;

merge out1 out2 a ;

run ;

proc gplot data=plot2 ;

title 'OLS Model Residual Plot' ;

axis1 label=(angle=90 'Residuals') ;

axis2 label=('Date') ;

symbol1 c=blue i=needle v=none ;

plot resid1*date / cframe=ligr haxis=axis2 vaxis=axis1 ;

run ;

proc autoreg data=a outest=estb ;

model lq = lp / nlag=(1 4) method=ml ;

output out=out2 r=resid2 ;

title "OLS, Autocorrelations, & Maximum Likelihood Estimates";

run ;

proc gplot data=plot2 ;

title 'Autoregressive Error Model Residual Plot' ;

axis1 label=(angle=90 'Residuals') ;

axis2 label=('Date') ;

symbol1 c=blue i=needle v=none ;

plot resid2*date / cframe=ligr haxis=axis2 vaxis=axis1 ;

run ;

proc iml ;

use estb ;

read all var {intercept lp} ;

close estb ;

x = (100:300)` ;

x = log(x) ;

y = intercept + lp*x ;

all = y || x ;

create outset from all ;

append from all ;

quit ;

data plot ;

set outset(rename=(col1=y col2=x)) ;

run ;

proc gplot data=plot ;

title 'Demand for Beef' ;

axis1 label=(angle=90 'log of quantity') ;

axis2 label=('log of price') ;

symbol color=blue interpol=join value=none ;

plot y*x / cframe=ligr vaxis=axis1 haxis=axis2 ;

run ;

These sample files and code examples are provided by SAS Institute Inc. "as is" without warranty of any kind, either express or implied, including but not limited to the implied warranties of merchantability and fitness for a particular purpose. Recipients acknowledge and agree that SAS Institute shall not be liable for any damages whatsoever arising out of their use of this material. In addition, SAS Institute will provide no support for the materials contained herein.

| Type: | Sample |

| Date Modified: | 2017-01-24 12:13:50 |

| Date Created: | 2017-01-24 12:09:48 |

Operating System and Release Information

| Product Family | Product | Host | SAS Release | |

| Starting | Ending | |||

| SAS System | SAS/ETS | z/OS | ||

| z/OS 64-bit | ||||

| OpenVMS VAX | ||||

| Microsoft® Windows® for 64-Bit Itanium-based Systems | ||||

| Microsoft Windows Server 2003 Datacenter 64-bit Edition | ||||

| Microsoft Windows Server 2003 Enterprise 64-bit Edition | ||||

| Microsoft Windows XP 64-bit Edition | ||||

| Microsoft® Windows® for x64 | ||||

| OS/2 | ||||

| Microsoft Windows 8 Enterprise 32-bit | ||||

| Microsoft Windows 8 Enterprise x64 | ||||

| Microsoft Windows 8 Pro 32-bit | ||||

| Microsoft Windows 8 Pro x64 | ||||

| Microsoft Windows 8.1 Enterprise 32-bit | ||||

| Microsoft Windows 8.1 Enterprise x64 | ||||

| Microsoft Windows 8.1 Pro 32-bit | ||||

| Microsoft Windows 8.1 Pro x64 | ||||

| Microsoft Windows 10 | ||||

| Microsoft Windows 95/98 | ||||

| Microsoft Windows 2000 Advanced Server | ||||

| Microsoft Windows 2000 Datacenter Server | ||||

| Microsoft Windows 2000 Server | ||||

| Microsoft Windows 2000 Professional | ||||

| Microsoft Windows NT Workstation | ||||

| Microsoft Windows Server 2003 Datacenter Edition | ||||

| Microsoft Windows Server 2003 Enterprise Edition | ||||

| Microsoft Windows Server 2003 Standard Edition | ||||

| Microsoft Windows Server 2003 for x64 | ||||

| Microsoft Windows Server 2008 | ||||

| Microsoft Windows Server 2008 R2 | ||||

| Microsoft Windows Server 2008 for x64 | ||||

| Microsoft Windows Server 2012 Datacenter | ||||

| Microsoft Windows Server 2012 R2 Datacenter | ||||

| Microsoft Windows Server 2012 R2 Std | ||||

| Microsoft Windows Server 2012 Std | ||||

| Microsoft Windows XP Professional | ||||

| Windows 7 Enterprise 32 bit | ||||

| Windows 7 Enterprise x64 | ||||

| Windows 7 Home Premium 32 bit | ||||

| Windows 7 Home Premium x64 | ||||

| Windows 7 Professional 32 bit | ||||

| Windows 7 Professional x64 | ||||

| Windows 7 Ultimate 32 bit | ||||

| Windows 7 Ultimate x64 | ||||

| Windows Millennium Edition (Me) | ||||

| Windows Vista | ||||

| Windows Vista for x64 | ||||

| 64-bit Enabled AIX | ||||

| 64-bit Enabled HP-UX | ||||

| 64-bit Enabled Solaris | ||||

| ABI+ for Intel Architecture | ||||

| AIX | ||||

| HP-UX | ||||

| HP-UX IPF | ||||

| IRIX | ||||

| Linux | ||||

| Linux for x64 | ||||

| Linux on Itanium | ||||

| OpenVMS Alpha | ||||

| OpenVMS on HP Integrity | ||||

| Solaris | ||||

| Solaris for x64 | ||||

| Tru64 UNIX | ||||