| Model Fitting: Linear Regression |

Interpreting Linear Regression Plots

You can use the Linear Regression analysis to create a variety of residual and diagnostic plots, as indicated by Figure 21.7. This section briefly presents the types of plots that are available. To provide common reference points, the same five observations are selected in each set of plots.

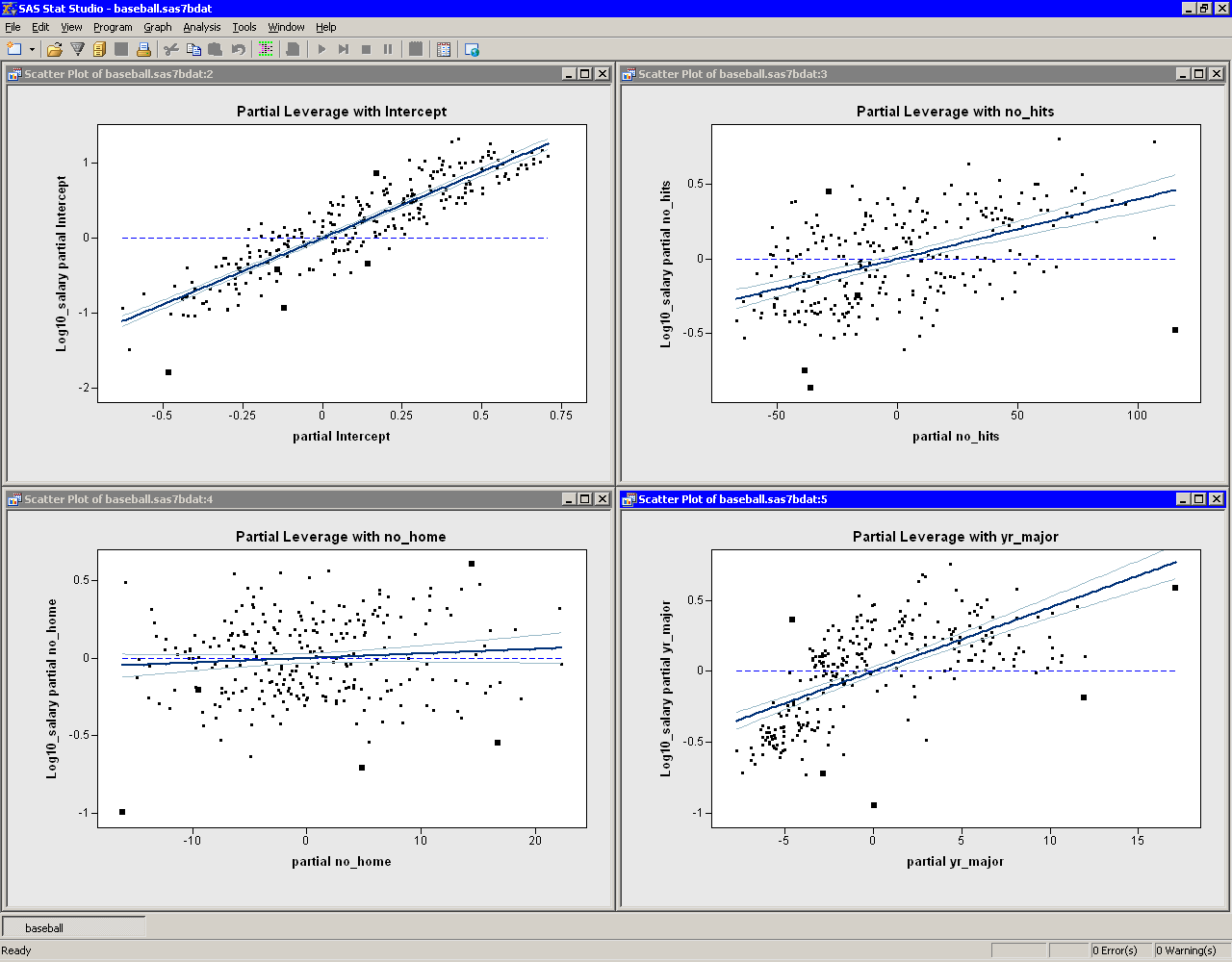

Partial Leverage Plots

Partial leverage plots are an attempt to isolate the effects of a single variable on the residuals (Rawlings, Pantula, and Dickey 1998, p. 359). A partial regression leverage plot is the plot of the residuals for the dependent variable against the residuals for a selected regressor, where the residuals for the dependent variable are calculated with the selected regressor omitted, and the residuals for the selected regressor are calculated from a model where the selected regressor is regressed on the remaining regressors. A line fit to the points has a slope equal to the parameter estimate in the full model. Confidence limits for each regressor are related to the confidence limits for parameter estimates (Sall 1990).

Partial leverage plots for the previous example are

shown in Figure 21.10. The lower-left plot shows

residuals of no_home. The confidence bands in this plot

contain the horizontal reference line, which

indicates that the coefficient of no_home is not

significantly different from zero.

|

Figure 21.10: Partial Leverage Plots

Plots of Residuals versus Explanatory Variables

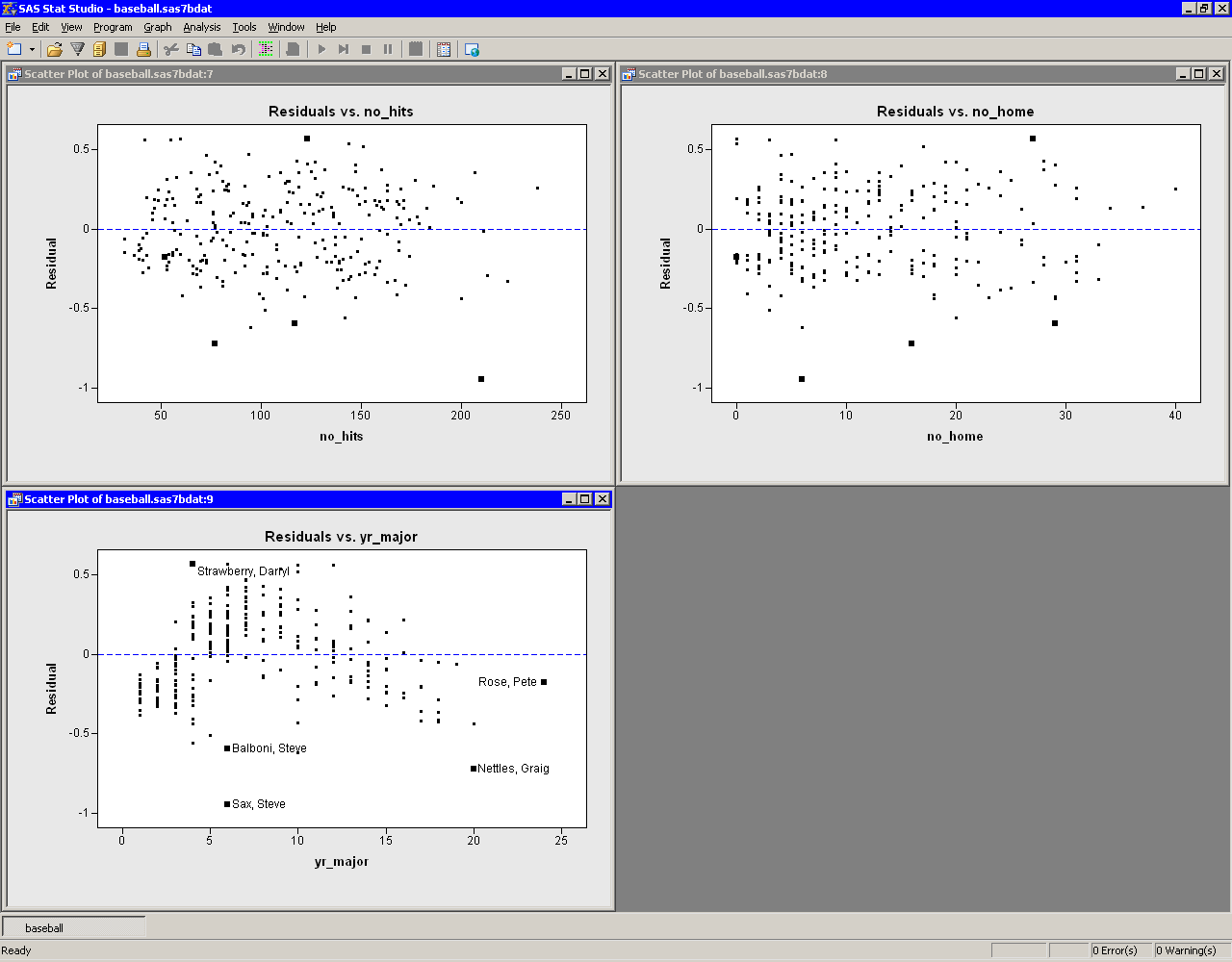

Figure 21.11 shows the residuals plotted against the three explanatory variables in the model. Note that the plot of residuals versus yr_major shows a distinct pattern. The plot indicates that players who have recently joined the major leagues earn less money, on average, than their veteran counterparts with 5 - 10 years of experience. The mean salary for players with 10 - 20 years of experience is comparable to the salary that new players make.

This pattern of residuals suggests that the example does not

correctly model the effect of the yr_major variable. Perhaps

it is more appropriate to model log10_salary as a nonlinear

function of yr_major. Also, the low salaries of

Steve Sax, Graig Nettles, and Steve Balboni might be unduly

influencing the fit.

|

Figure 21.11: Residual versus Explanatory Plots

More Residual Plots

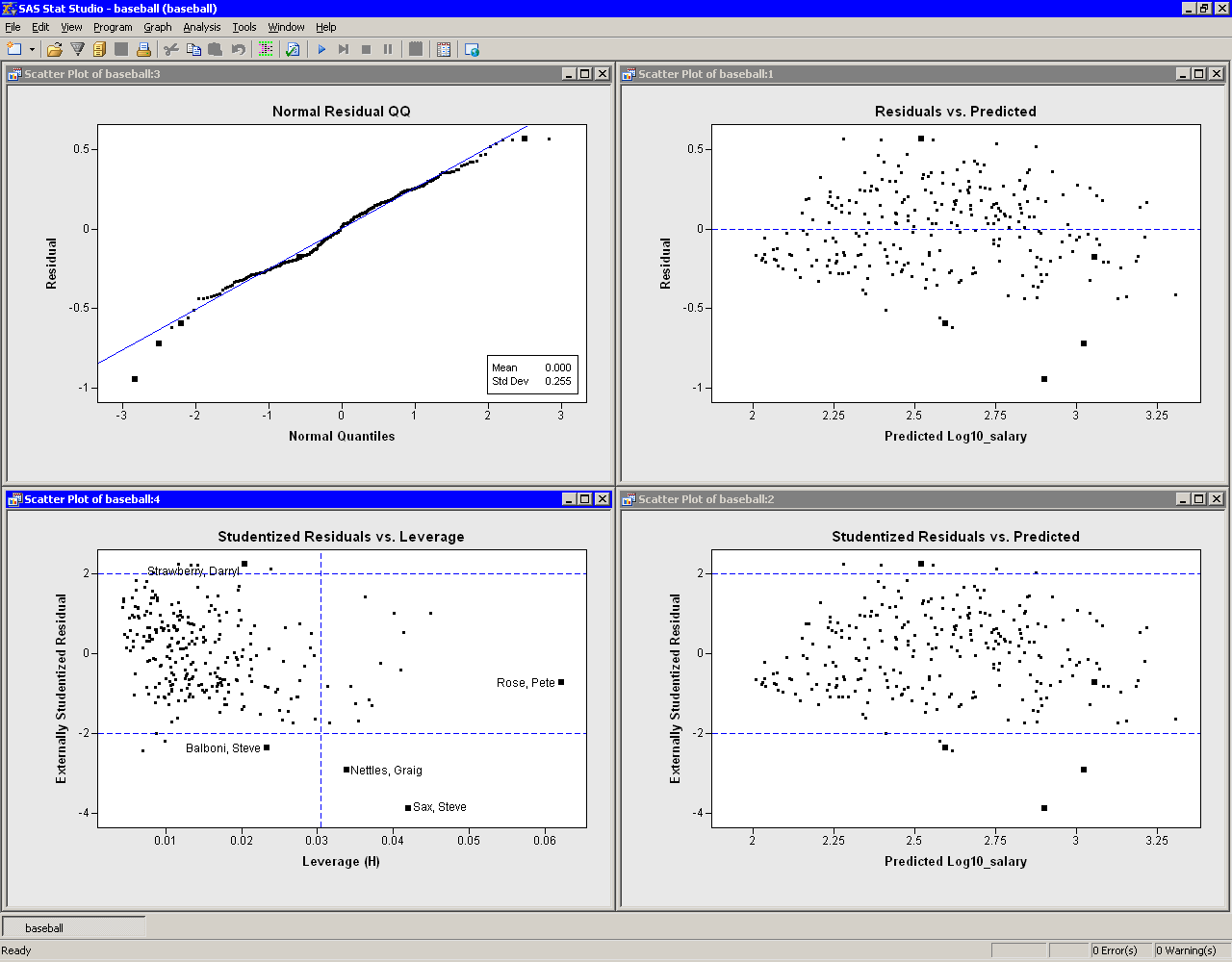

Figure 21.12 shows several residual plots.The Q-Q plot (upper left in Figure 21.12) shows that the residuals are approximately normally distributed. Three players with large negative residuals (Steve Sax, Graig Nettles, and Steve Balboni) are highlighted below the diagonal line in the plot. These players seem to be outliers for this model.

The residuals versus predicted plot is located in the upper-right

corner of

Figure 21.12. As noted in the example, the residuals show a

slight "bend" when plotted against the predicted value.

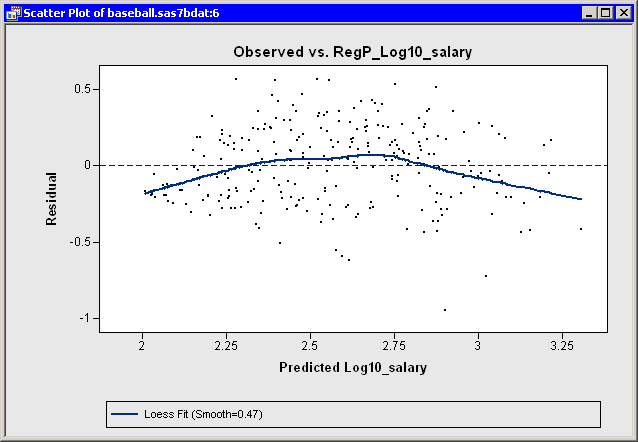

Figure 21.13 makes the trend easier to see by adding

a loess smoother to the residual plot. (See Chapter 18, "Data Smoothing: Loess," for

more information about adding loess curves.)

As discussed in the previous section, this trend might indicate the

need for a nonlinear term involving

yr_major. Alternatively, excluding

or downweighting outliers might lead

to a better fit.

|

|

Figure 21.13: A Loess Smoother of the Residuals

The lower-right plot in Figure 21.12 is a graph of

externally studentized residuals versus predicted values.

The externally studentized residual (known as RSTUDENT in the

documentation of the REG procedure) is a studentized residual in which

the error variance for the ![]() th observation

is estimated without including the

th observation

is estimated without including the ![]() th observation.

You should examine an observation when the absolute value of the

studentized residual exceeds 2.

th observation.

You should examine an observation when the absolute value of the

studentized residual exceeds 2.

The lower-left plot in Figure 21.12 is a graph of

(externally) studentized residuals versus the leverage

statistic. The leverage statistic

for the ![]() th observation is also

the

th observation is also

the ![]() th element on the diagonal of the hat

matrix.

The leverage statistic indicates

how far an observation is from the centroid of the data in the space

of the explanatory variables. Observations far from the centroid are

potentially influential in fitting the regression model.

th element on the diagonal of the hat

matrix.

The leverage statistic indicates

how far an observation is from the centroid of the data in the space

of the explanatory variables. Observations far from the centroid are

potentially influential in fitting the regression model.

Observations whose leverage values exceed ![]() are called

high leverage points (Belsley, Kuh, and Welsch 1980).

Here

are called

high leverage points (Belsley, Kuh, and Welsch 1980).

Here ![]() is the number

of parameters in the model (including the intercept) and

is the number

of parameters in the model (including the intercept) and ![]() is the

number of observations used in computing the least squares estimates.

For the example,

is the

number of observations used in computing the least squares estimates.

For the example, ![]() observations are used. There are three

regressors in addition to the intercept, so

observations are used. There are three

regressors in addition to the intercept, so ![]() . The cutoff value

is therefore 0.0304.

. The cutoff value

is therefore 0.0304.

The plot of studentized residuals versus leverage has a vertical line that indicates high leverage points and two horizontal lines that indicate potential outliers. In Figure 21.12, Pete Rose is an observation with high leverage (due to his 24 years in the major leagues), but not an outlier. Graig Nettles and Steve Sax are outliers and leverage points. Steve Balboni is an outlier because of a low salary relative to the model, whereas Darryl Strawberry's salary is high relative to the prediction of the model.

You should be careful in interpreting results when there are high leverage points. It is possible that Pete Rose fits the model precisely because he is a high leverage point. Chapter 22, "Model Fitting: Robust Regression," describes a robust technique for identifying high leverage points and outliers.

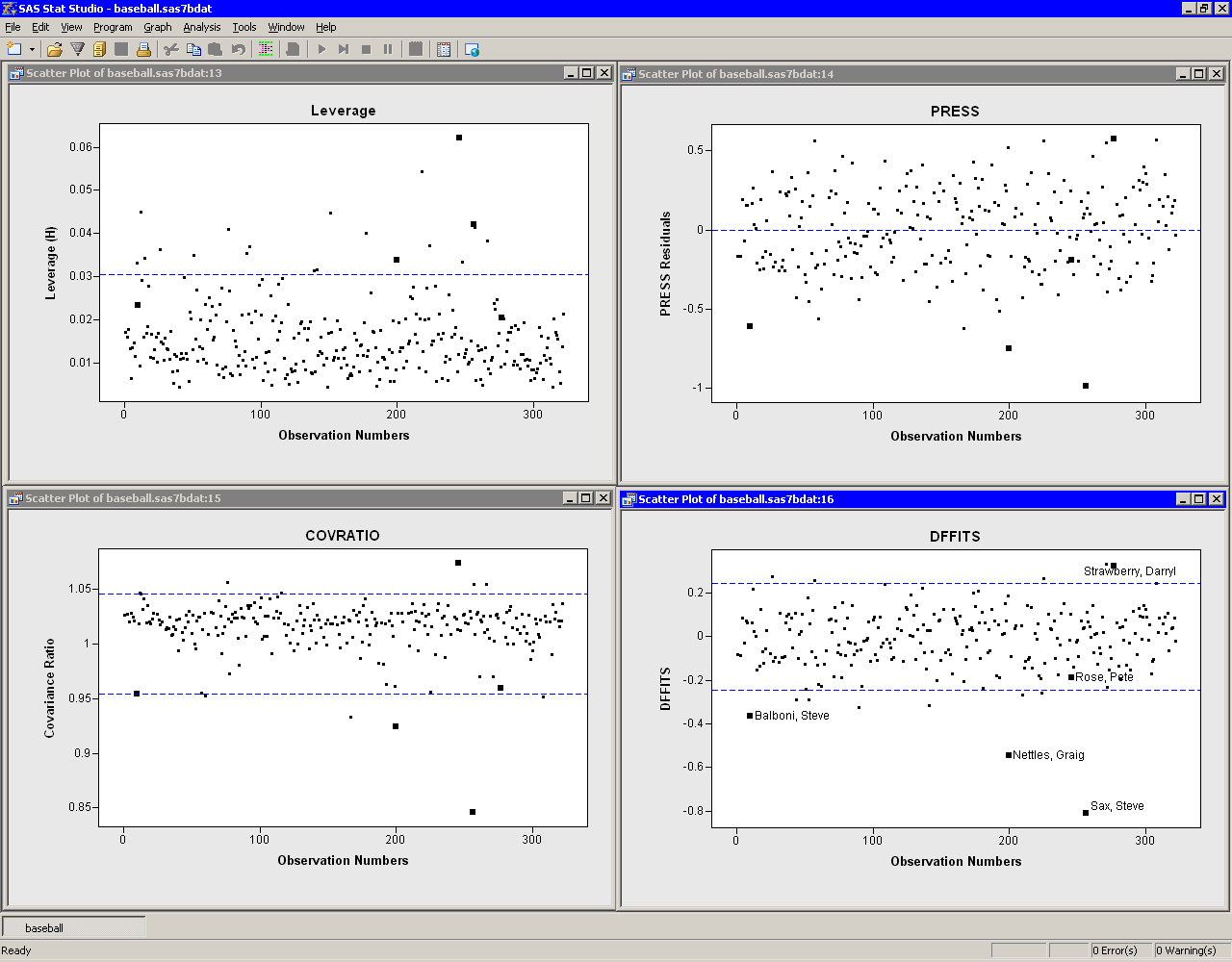

Influence Diagnostic Plots

Previous sections discussed plots that included Cook'sThe upper-left plot displays the leverage statistic along with the

cutoff ![]() .

.

The upper-right plot displays the PRESS residuals.

The PRESS residual

for observation ![]() is the

residual that would result if you fit the model without using the

is the

residual that would result if you fit the model without using the ![]() th

observation. A large press residual indicates an influential

observation. Pete Rose does not have a large PRESS residual.

th

observation. A large press residual indicates an influential

observation. Pete Rose does not have a large PRESS residual.

The lower-left plot displays the covariance ratio.

The

covariance ratio measures the change in the determinant of the

covariance matrix of the estimates by deleting the ![]() th

observation. Influential observations have

th

observation. Influential observations have

![]() , where

, where ![]() is the covariance ratio (Belsley, Kuh, and Welsch 1980).

Horizontal lines on the plot mark the critical values. Pete Rose has

the largest value of the covariance ratio.

is the covariance ratio (Belsley, Kuh, and Welsch 1980).

Horizontal lines on the plot mark the critical values. Pete Rose has

the largest value of the covariance ratio.

The lower-right plot displays the DFFIT statistic, which is similar

to Cook's ![]() . The observations outside of

. The observations outside of ![]() are

influential (Belsley, Kuh, and Welsch 1980). Pete Rose is not influential by this measure.

are

influential (Belsley, Kuh, and Welsch 1980). Pete Rose is not influential by this measure.

|

Figure 21.14: Influence Diagnostics Plots

Copyright © 2008 by SAS Institute Inc., Cary, NC, USA. All rights reserved.