| The Interior Point Nonlinear Programming Solver -- Experimental |

Overview of Constrained Optimization

A function that plays a pivotal role in establishing conditions that characterize a local minimum of an

NLP problem is the Lagrangian function  , defined as

, defined as

Note that the Lagrangian function can be seen as a linear combination of the objective and constraint

functions. The coefficients of the constraints,

, and

, are called the Lagrange

multipliers or dual variables. At a feasible point

, an inequality constraint is called active if it

is satisfied as an equality, i.e.,

. The set of active constraints at a feasible point

is then defined as the union of the index set of the equality constraints,

, and the indices of those inequality constraints

that are active at

, i.e.,

An important condition that is assumed to hold in the majority of optimization algorithms is the so-called

linear independence constraint qualification (LICQ). The LICQ states that at any feasible point

, the

gradients of all the active constraints are linearly independent. The main purpose of the LICQ is to ensure that

the set of constraints is well-defined, in a way that there are no redundant constraints, or in a way that there are

no constraints defined such that their gradients are always equal to zero.

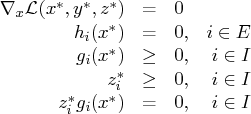

The First-Order Necessary Optimality Conditions

If

is a local minimum of the NLP problem and the LICQ holds at

, then there are vectors of Lagrange

multipliers

and

, with components

, and

, respectively,

such that the following conditions are satisfied:

where

is the gradient of the Lagrangian function with respect to

, defined as

The preceding conditions are often called the

Karush-Kuhn-Tucker (KKT) conditions , named after their inventors.

The last group of equations (

) is called the complementarity condition. Its main

aim is to try to force the Lagrange multipliers,

, of the inactive inequalities

(i.e., those inequalities with

) to zero.

The KKT conditions describe the way the first derivatives of the objective and constraints are related at a local

minimum . However, they are not enough to fully characterize a local minimum. The second-order optimality

conditions attempt to fulfill this aim, by examining the curvature of the Hessian matrix of the Lagrangian function

at a point that satisfies the KKT conditions.

The Second-Order Necessary Optimality Condition

Let

be a local minimum of the NLP problem, and let

be the corresponding Lagrange multipliers that

satisfy the first-order optimality conditions. Then

for all

nonzero vectors

that satisfy the following conditions:

-

,

,

-

,

,  , such that

, such that

-

, , such that

, , such that

The second-order necessary optimality condition states that, at a local minimum, the curvature of

the Lagrangian function along the directions that satisfy the preceding conditions must be nonnegative.