| Language Reference |

DURATION Function

calculates and returns a scalar containing the modified duration of a noncontingent cash flow.

- DURATION( times,flows,ytm)

The DURATION function returns the modified duration of a noncontingent cash flow as a scalar.

- times

- is an

-dimensional column vector of times.

Elements should be nonnegative.

-dimensional column vector of times.

Elements should be nonnegative.

- flows

- is an -dimensional column vector of cash flows.

- ytm

- is the per-period yield-to-maturity of the cash-flow stream. This is a scalar and should be positive.

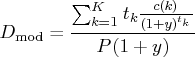

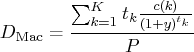

Duration of a security is generally defined as

For example, consider the following statements:

times={1};

ytm={0.1};

flow={10};

duration=duration(times,flow,ytm);

print duration;

These statements produce the following output:

DURATION

0.9090909

Copyright © 2009 by SAS Institute Inc., Cary, NC, USA. All rights reserved.