BLKSHPTPRC Function

Calculates put prices for European options on stocks, based on the Black-Scholes model.

| Category: | Financial |

| Returned data type: | DOUBLE |

Syntax

Arguments

E

is a nonmissing, positive value that specifies the exercise price.

| Requirement | Specify E and S in the same units. |

| Data type | DOUBLE |

t

is a nonmissing value that specifies the time to maturity, in years.

| Data type | INTEGER |

S

is a nonmissing, positive value that specifies the share price.

| Requirement | Specify S and E in the same units. |

| Data type | DOUBLE |

r

is a nonmissing, positive value that specifies the annualized risk-free interest rate, continuously compounded.

| Data type | DOUBLE |

sigma

is a nonmissing, positive fraction that specifies the volatility of the underlying asset.

| Data type | DOUBLE |

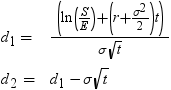

Details

Comparisons

Example

|

Statements

|

Results

|

|---|---|

|

|

----+----1----+-—-2-- |

select blkshptprc(230,.5,290,.04,.25); |

1.56597442946068 |

select blkshptprc(350,.3,400,.05,.2); |

1.64091943067592 |