The COPULA Procedure (Experimental)

- Overview

- Getting Started

-

Syntax

-

Details

Sklar’s Theorem Dependence Measures Normal Copula Student’s t copula Archimedean Copulas Canonical Maximum Likelihood Estimation (CMLE) Exact Maximum Likelihood Estimation (MLE) Calibration Estimation Nonlinear Optimization Options Displayed Output OUTCOPULA= Data Set OUTPSEUDO=, OUT=, and OUTUNIFORM= Data Sets ODS Table Names ODS Graph Names

-

Examples

- References

| Canonical Maximum Likelihood Estimation (CMLE) |

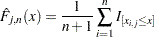

In the CMLE estimation method, it is assumed that the sample data  ,

,  have been transformed into uniform variates

have been transformed into uniform variates  , . One commonly used transformation is the nonparametric estimation of the CDF of the marginal distributions, which is closely related to empirical CDF,

, . One commonly used transformation is the nonparametric estimation of the CDF of the marginal distributions, which is closely related to empirical CDF,

|

where

|

The transformed data  are used as if they had uniform marginal distributions; hence, they are called pseudo-samples. The function

are used as if they had uniform marginal distributions; hence, they are called pseudo-samples. The function  is different from the standard empirical CDF in the scalar

is different from the standard empirical CDF in the scalar  , which is to ensure that the transformed data cannot be on the boundary of the unit interval

, which is to ensure that the transformed data cannot be on the boundary of the unit interval  . It is clear that

. It is clear that

|

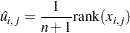

where  is the rank among in increasing order.

is the rank among in increasing order.

Let  be the density function of a copula

be the density function of a copula  , and let

, and let  be the parameter vector to be estimated. The parameter is estimated by maximum likelihood:

be the parameter vector to be estimated. The parameter is estimated by maximum likelihood:

|