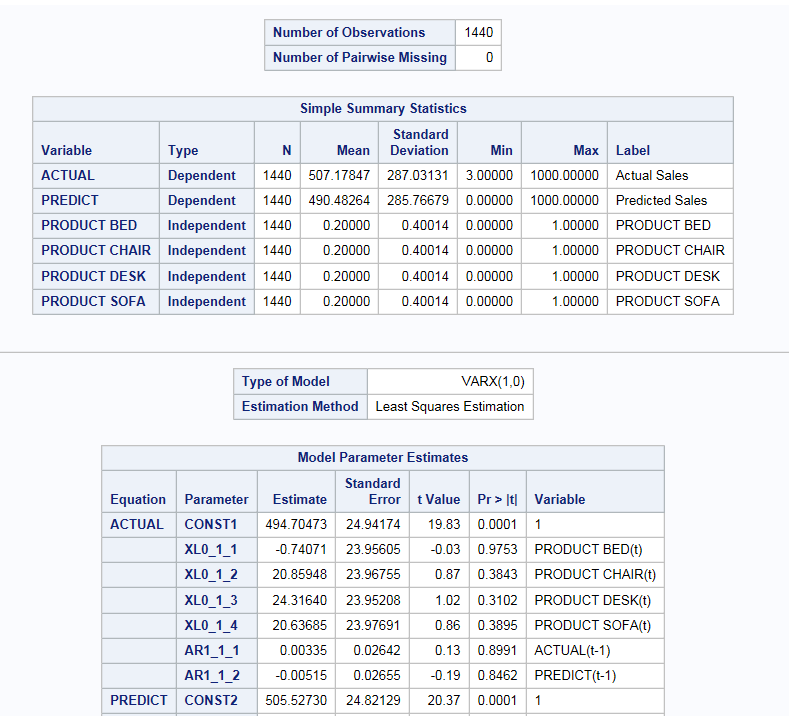

Time Series Analysis for Multiple Dependent Variables

Assigning Data to Roles

To perform a time series

analysis, you must assign an input data set. To filter the input data source, click

.

.

.

To perform a time series

analysis with multiple dependent variables, you also must assign at

least two variables to the Dependent variables role.

|

Role

|

Description

|

|---|---|

|

Roles

|

|

|

Dependent

variables

|

specifies the dependent

variables for the analysis.

|

|

Independent Variables

|

|

|

Continuous

variables

|

specifies the independent

variables for the model.

|

|

Categorical

variables

|

specifies the classification

variables to use in the analysis.

|

|

Time series

ID

|

specifies the datetime

values for the series.

If you assign a SAS

date or datetime variable to this role, the task automatically determines

the time interval for these values. You can change this interval and

also specify the multiplier, shift, and seasonal length. For more information about these options, see Understanding SAS Time Intervals.

Note: This role is available only

if you have multiple dependent variables.

|

|

Additional Roles

|

|

|

Group analysis

by

|

enables you to obtain separate

analyses of observations for each unique group.

|

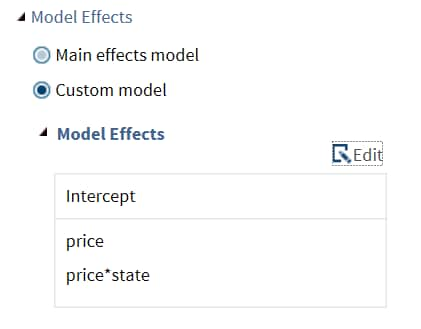

Setting the Model Options

You can display the main effects

model or create a custom model. To create a custom model, select the Custom

Model option, and then click Edit.

The Model Effects Builder opens. All continuous

variables and categorical variables are listed in the Variables pane.

-

To create a main effect, select the variable in the Variables pane, and then click Add.

-

To create a crossed effect, select the variables in the Variables pane. (You can use Ctrl to select multiple variables.) Then click Cross.

When you finish, click OK.

The effects that you specified now appear on the Model tab.

Here are the remaining

options on the Model tab.

|

Option Name

|

Description

|

|---|---|

|

Model Settings

|

|

|

Process Model

|

|

|

Automatically

select process orders

|

removes insignificant

autoregressive and moving average orders based on the value of the

information criteria.

|

|

Autoregressive

order (p), Maximum autoregressive order (p)

|

specifies the order

of the autoregressive process.

|

|

Moving average

order (q), Maximum average order (q)

|

specifies the order

of the moving average process.

|

|

Exogenous

variables lag (xlag)

|

specifies the lags for

the exogenous variables.

|

|

GARCH Conditional Heteroscedasticity

|

|

|

ARCH process

order (q)

|

specifies the order

of the ARCH process to be fitted.

|

|

GARCH process

order (p)

|

specifies the order

of the GARCH process to be fitted.

Note: This option is available

only if you specify an ARCH process order greater than 0.

|

|

GARCH model

representation

|

specifies the type of

multivariate GARCH model representation.

Here are the valid

options:

Note: This option is available

only if you specify an ARCH process order greater than 0.

|

|

GARCH model

type

|

specifies the subform

type of GARCH model.

Here are the valid

options:

Note: This option is available

only if you select constant conditional correlation representation

or the dynamic conditional correlation representation.

|

|

Vector Error Correction

|

|

|

Cointegration

rank

|

specifies the cointegration

rank of the cointegrated system. The rank of cointegration must be

less than the number of dependent variables.

|

|

Select a

normalization variable

|

specifies a dependent

variable whose cointegrating vectors are normalized.

|

Setting the Options

|

Option Name

|

Description

|

|---|---|

|

Methods

|

|

|

Optimization

method

|

specifies the optimization

method to use. By default, no optimization method is used.

|

|

Maximum

number of iterations

|

specifies the maximum

number of iterations. You can use the default value or specify a custom

value.

|

|

Statistics

|

|

|

You can include these

statistics in the results:

|

|

|

Plots

|

|

|

You can choose to include

the default plots in the results, only selected plots, all of the

plots, or none of the plots.

You can also include

these plots in the results:

|

|

Copyright © SAS Institute Inc. All rights reserved.