The SURVEYLOGISTIC Procedure

- Overview

- Getting Started

-

Syntax

PROC SURVEYLOGISTIC StatementBY StatementCLASS StatementCLUSTER StatementCONTRAST StatementDOMAIN StatementEFFECT StatementESTIMATE StatementFREQ StatementLSMEANS StatementLSMESTIMATE StatementMODEL StatementOUTPUT StatementREPWEIGHTS StatementSLICE StatementSTORE StatementSTRATA StatementTEST StatementUNITS StatementWEIGHT Statement

PROC SURVEYLOGISTIC StatementBY StatementCLASS StatementCLUSTER StatementCONTRAST StatementDOMAIN StatementEFFECT StatementESTIMATE StatementFREQ StatementLSMEANS StatementLSMESTIMATE StatementMODEL StatementOUTPUT StatementREPWEIGHTS StatementSLICE StatementSTORE StatementSTRATA StatementTEST StatementUNITS StatementWEIGHT Statement -

DetailsMissing ValuesModel SpecificationModel FittingSurvey Design InformationLogistic Regression Models and ParametersVariance EstimationDomain AnalysisHypothesis Testing and EstimationLinear Predictor, Predicted Probability, and Confidence LimitsOutput Data SetsDisplayed OutputODS Table NamesODS Graphics

-

Examples

- References

The factor ![]() in the computation of the matrix

in the computation of the matrix ![]() reduces the small sample bias associated with using the estimated function to calculate deviations (Morel, 1989; Hidiroglou, Fuller, and Hickman, 1980). For simple random sampling, this factor contributes to the degrees-of-freedom correction applied to the residual mean square

for ordinary least squares in which p parameters are estimated. By default, the procedure uses this adjustment in Taylor series variance estimation. It is equivalent

to specifying the VADJUST=DF option in the MODEL statement. If you do not want to use this multiplier in the variance estimation, you can specify the

VADJUST=NONE option in the MODEL statement to suppress this factor.

reduces the small sample bias associated with using the estimated function to calculate deviations (Morel, 1989; Hidiroglou, Fuller, and Hickman, 1980). For simple random sampling, this factor contributes to the degrees-of-freedom correction applied to the residual mean square

for ordinary least squares in which p parameters are estimated. By default, the procedure uses this adjustment in Taylor series variance estimation. It is equivalent

to specifying the VADJUST=DF option in the MODEL statement. If you do not want to use this multiplier in the variance estimation, you can specify the

VADJUST=NONE option in the MODEL statement to suppress this factor.

In addition, you can specify the VADJUST=MOREL option to request an adjustment to the variance estimator for the model parameters ![]() , introduced by Morel (1989):

, introduced by Morel (1989):

where for given nonnegative constants ![]() and

and ![]() ,

,

The adjustment ![]() does the following:

does the following:

-

reduces the small sample bias reflected in inflated Type I error rates

-

guarantees a positive-definite estimated covariance matrix provided that

exists

exists

-

is close to zero when the sample size becomes large

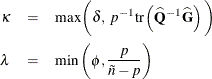

In this adjustment, ![]() is an estimate of the design effect, which has been bounded below by the positive constant

is an estimate of the design effect, which has been bounded below by the positive constant ![]() . You can use DEFFBOUND=

. You can use DEFFBOUND=![]() in the VADJUST=MOREL option in the MODEL statement to specify this lower bound; by default, the procedure uses

in the VADJUST=MOREL option in the MODEL statement to specify this lower bound; by default, the procedure uses ![]() . The factor

. The factor ![]() converges to zero when the sample size becomes large, and

converges to zero when the sample size becomes large, and ![]() has an upper bound

has an upper bound ![]() . You can use ADJBOUND=

. You can use ADJBOUND=![]() in the VADJUST=MOREL option in the MODEL statement to specify this upper bound; by default, the procedure uses

in the VADJUST=MOREL option in the MODEL statement to specify this upper bound; by default, the procedure uses ![]() .

.