| The PHREG Procedure |

Testing Linear Hypotheses about Regression Coefficients

Linear hypotheses for  are expressed in matrix form as

are expressed in matrix form as

|

where L is a matrix of coefficients for the linear hypotheses, and c is a vector of constants. The Wald chi-square statistic for testing  is computed as

is computed as

|

where  is the estimated covariance matrix. Under ,

is the estimated covariance matrix. Under ,  has an asymptotic chi-square distribution with r degrees of freedom, where r is the rank of

has an asymptotic chi-square distribution with r degrees of freedom, where r is the rank of  .

.

Optimal Weights for the AVERAGE option in the TEST Statement

Let  , where

, where  is a subset of

is a subset of  regression coefficients. For any vector

regression coefficients. For any vector  of length ,

of length ,

|

To find  such that

such that  has the minimum variance, it is necessary to minimize

has the minimum variance, it is necessary to minimize  subject to

subject to  . Let

. Let  be a vector of 1’s of length . The expression to be minimized is

be a vector of 1’s of length . The expression to be minimized is

|

where  is the Lagrange multipler. Differentiating with respect to and , respectively, yields

is the Lagrange multipler. Differentiating with respect to and , respectively, yields

|

|

|

|||

|

|

|

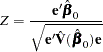

Solving these equations gives

|

This provides a one degree-of-freedom test for testing the null hypothesis  with normal test statistic

with normal test statistic

|

This test is more sensitive than the multivariate test specified by the TEST statement

Multivariate: test X1, ..., Xs;

where X , ..., X are the variables with regression coefficients

, ..., X are the variables with regression coefficients  , respectively.

, respectively.

Copyright © 2009 by SAS Institute Inc., Cary, NC, USA. All rights reserved.