| The VARMAX Procedure |

| VARMAX Model |

The vector autoregressive moving-average model with exogenous variables is called the VARMAX( ,

, ,

, ) model. The form of the model can be written as

) model. The form of the model can be written as

|

where the output variables of interest,  , can be influenced by other input variables,

, can be influenced by other input variables,  , which are determined outside of the system of interest. The variables

, which are determined outside of the system of interest. The variables  are referred to as dependent, response, or endogenous variables, and the variables

are referred to as dependent, response, or endogenous variables, and the variables  are referred to as independent, input, predictor, regressor, or exogenous variables. The unobserved noise variables,

are referred to as independent, input, predictor, regressor, or exogenous variables. The unobserved noise variables,  , are a vector white noise process.

, are a vector white noise process.

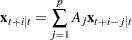

The VARMAX(,,) model can be written

|

|

|

where

|

|

|

|||

|

|

|

|||

|

|

|

are matrix polynomials in  in the backshift operator, such that

in the backshift operator, such that  , the

, the  and

and  are

are  matrices, and the

matrices, and the  are

are  matrices.

matrices.

The following assumptions are made:

,

,  , which is positive-definite, and

, which is positive-definite, and  for

for  .

. For stationarity and invertibility of the VARMAX process, the roots of

and

and  are outside the unit circle.

are outside the unit circle. The exogenous (independent) variables

are not correlated with residuals

are not correlated with residuals  ,

,  . The exogenous variables can be stochastic or nonstochastic. When the exogenous variables are stochastic and their future values are unknown, forecasts of these future values are needed to forecast the future values of the endogenous (dependent) variables. On occasion, future values of the exogenous variables can be assumed to be known because they are deterministic variables. The VARMAX procedure assumes that the exogenous variables are nonstochastic if future values are available in the input data set. Otherwise, the exogenous variables are assumed to be stochastic and their future values are forecasted by assuming that they follow the VARMA(,) model, prior to forecasting the endogenous variables, where and are the same as in the VARMAX(,,) model.

. The exogenous variables can be stochastic or nonstochastic. When the exogenous variables are stochastic and their future values are unknown, forecasts of these future values are needed to forecast the future values of the endogenous (dependent) variables. On occasion, future values of the exogenous variables can be assumed to be known because they are deterministic variables. The VARMAX procedure assumes that the exogenous variables are nonstochastic if future values are available in the input data set. Otherwise, the exogenous variables are assumed to be stochastic and their future values are forecasted by assuming that they follow the VARMA(,) model, prior to forecasting the endogenous variables, where and are the same as in the VARMAX(,,) model.

State-Space Representation

Another representation of the VARMAX(,,) model is in the form of a state-variable or a state-space model, which consists of a state equation

|

and an observation equation

|

where

and

|

On the other hand, it is assumed that follows a VARMA(,) model

|

The model can also be expressed as

|

where  and

and  are matrix polynomials in , and the

are matrix polynomials in , and the  and

and  are

are  matrices. Without loss of generality, the AR and MA orders can be taken to be the same as the VARMAX(,,) model, and

matrices. Without loss of generality, the AR and MA orders can be taken to be the same as the VARMAX(,,) model, and  and

and  are independent white noise processes.

are independent white noise processes.

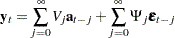

Under suitable conditions such as stationarity, is represented by an infinite order moving-average process

|

where  .

.

The optimal minimum mean squared error (minimum MSE)  -step-ahead forecast of

-step-ahead forecast of  is

is

|

|

|

|||

|

|

|

For  ,

,

|

The VARMAX(,,) model has an absolutely convergent representation as

|

|

|

|||

|

|

|

|||

|

|

|

or

|

where  ,

,  , and

, and  .

.

The optimal (minimum MSE) -step-ahead forecast of  is

is

|

|

|

|||

|

|

|

for  with

with  . For ,

. For ,

|

|

|

|||

|

|

|

|||

|

|

|

|||

|

|

|

where  .

.

Define  . For

. For  with , you obtain

with , you obtain

|

|

|

|||

|

|

|

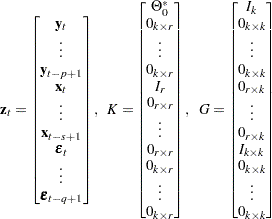

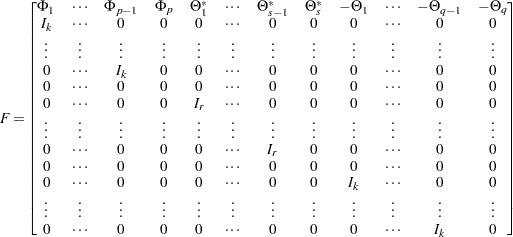

From the preceding relations, a state equation is

|

and an observation equation is

|

where

|

|

|

and

|

Note that the matrix  and the input vector

and the input vector  are defined only when

are defined only when  .

.

Copyright © SAS Institute, Inc. All Rights Reserved.