Introduction to Statistical Modeling with SAS/STAT Software

To estimate the parameters in a linear model with mean function ![]() by maximum likelihood, you need to specify the distribution of the response vector

by maximum likelihood, you need to specify the distribution of the response vector ![]() . In the linear model with a continuous response variable, it is commonly assumed that the response is normally distributed.

In that case, the estimation problem is completely defined by specifying the mean and variance of

. In the linear model with a continuous response variable, it is commonly assumed that the response is normally distributed.

In that case, the estimation problem is completely defined by specifying the mean and variance of ![]() in addition to the normality assumption. The model can be written as

in addition to the normality assumption. The model can be written as ![]() , where the notation

, where the notation ![]() indicates a multivariate normal distribution with mean vector

indicates a multivariate normal distribution with mean vector ![]() and variance matrix

and variance matrix ![]() . The log likelihood for

. The log likelihood for ![]() then can be written as

then can be written as

This function is maximized in ![]() when the sum of squares

when the sum of squares ![]() is minimized. The maximum likelihood estimator of

is minimized. The maximum likelihood estimator of ![]() is thus identical to the ordinary least squares estimator. To maximize

is thus identical to the ordinary least squares estimator. To maximize ![]() with respect to

with respect to ![]() , note that

, note that

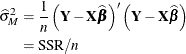

Hence the MLE of ![]() is the estimator

is the estimator

This is a biased estimator of ![]() , with a bias that decreases with n.

, with a bias that decreases with n.