| Language Reference |

| COVLAG Function |

The COVLAG function computes a sequence of lagged crossproduct matrices. This function is useful for computing sample autocovariance sequences for scalar or vector time series.

The arguments to the COVLAG function are as follows:

- x

is an

matrix of time series values;

matrix of time series values;  is the number of observations, and

is the number of observations, and  is the dimension of the random vector.

is the dimension of the random vector. - k

is a scalar, the absolute value of which specifies the number of lags desired. If

is positive, a mean correction is made. If is negative, no mean correction is made.

is positive, a mean correction is made. If is negative, no mean correction is made.

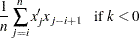

The value returned by the COVLAG function is an  matrix. The

matrix. The  th

th  block of the matrix is the sum

block of the matrix is the sum

|

where  is the

is the  th row of

th row of  . If > 0, then the th block of the matrix is

. If > 0, then the th block of the matrix is

|

where  is a row vector of the column means of .

is a row vector of the column means of .

For example, the following statements produce a lagged crossproduct matrix:

x = T(do(-9, 9, 2)); cov = covlag(x, 4); print cov;

Copyright © SAS Institute, Inc. All Rights Reserved.